Hydrogen prices across key European countries rose over the course of 2021, primarily driven by gas and power price spikes amid tight supply, while record carbon prices lifted grey hydrogen close to parity with low-carbon hydrogen, analysis from market data and intelligence group ICIS shows.

Near-Curve

The hydrogen near curve posted the largest gains, as record-breaking gas and power prices lifted the variable and levelized cost of hydrogen (LCOH) to the highest levels recorded by ICIS.

Between Jan. 4 and Dec. 17, 2021, December, prices for Dutch baseload power electrolytic, steam methane reformation (SMR) without carbon capture and storage (CCS) (unabated SMR), SMR with CCS (low-carbon SMR), and authothermal reforming (ATR) of natural gas with CCS (low-carbon ATR) purchased on a front-month basis rose to five times in value.

The highest climb was for baseload electrolytic hydrogen, which rose from €4.16/kg H2 on LCOH basis, to a high of €24.3/kg H2 on Dec. 16.

Meanwhile, all natural gas–derived hydrogen production streams saw similar proportional gains, the highest of which was low-carbon SMR, which rose to €8.93/kg H2 on LCOH basis on Dec. 17.

Comparatively, the lowest gas-derived front-month price recorded by ICIS in 2020 was €0.75/kg H2 on LCOH basis for Dutch unabated SMR. Baseload electrolytic prices were also substantially lower during the first half of 2020 amid coronavirus-induced demand destruction and high renewable output. The lowest Dutch baseload electrolytic price on a front-month LCOH basis was €2.03/kg H2, recorded in March 2020.

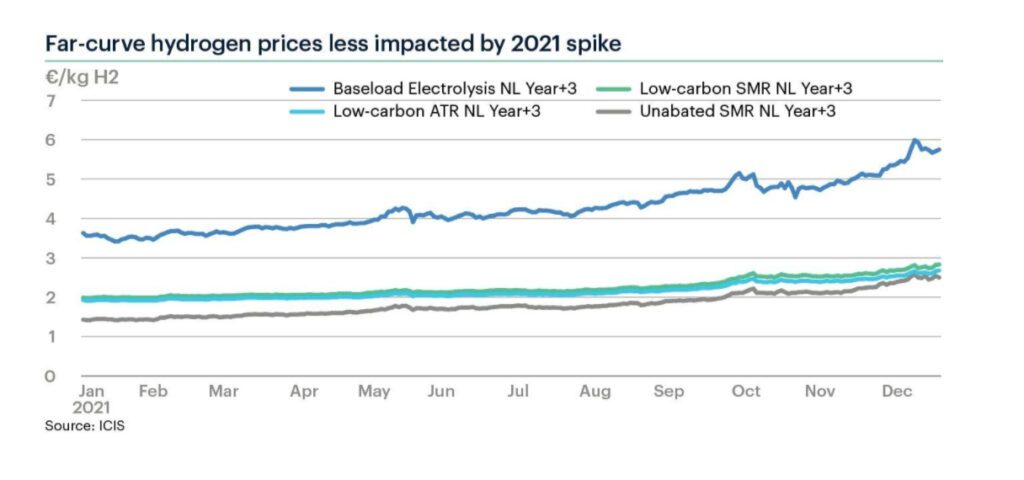

Far Curve

Hydrogen contracts for 2024 also rose over 2021, but not to the same degree as that of the near curve, in line with the trend on the gas and power curves.

2024 is a key year for hydrogen as it is the date by which the European Commission aims to complete Phase 1 of its hydrogen strategy and have 6 GW of installed electrolysis capacity for the production of green hydrogen online.

The largest jump in spot-purchased hydrogen was once again seen across baseload electrolytic hydrogen, which climbed just over €2/kg H2 between Jan. 4 to Dec. 17, 2021. Natural-gas derived hydrogen gained around €1/kg H2 depending on technology streams: unabated SMR rose to €2.5/kg H2, the highest of the three gas-based technologies, following higher carbon prices.

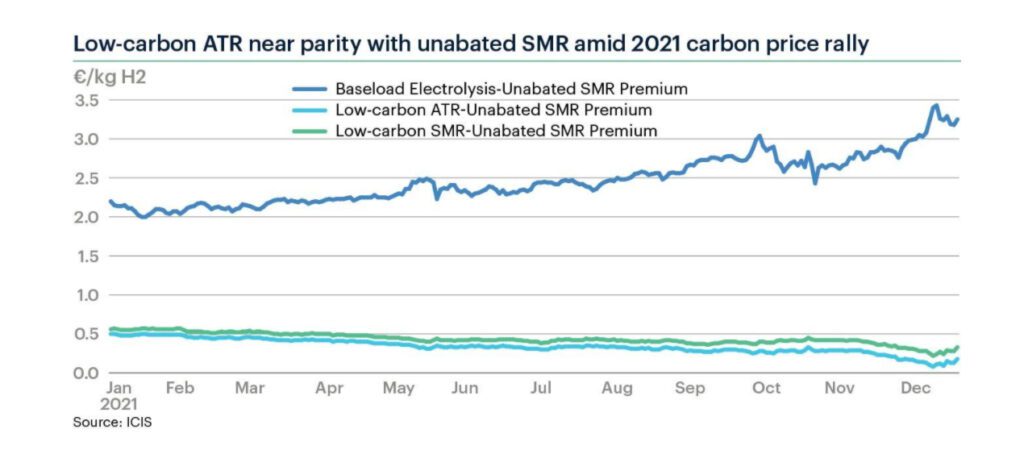

Premiums

Hydrogen price premiums over unabated SMR, or grey hydrogen, varied substantially across different technology processes and delivery periods over the course of 2021.

On Jan. 4, 2021, baseload electrolytic hydrogen for delivery in 2024 was around €2/kg H2 more expensive than unabated SMR.

However, despite rising carbon contracts over the course of the year, the climb in power price—which accounts for roughly 75% of the final price of electrolytic hydrogen—lifted the premium to a peak of €3.43/kg H2 on Dec. 9.

Meanwhile, low-carbon SMR and low-carbon ATR premiums over unabated SMR narrowed substantially for 2024 delivery.

At the start of the year, the two technology streams resulted in an LCOH of around €0.50/kg H2 higher than unabated SMR. On Dec. 8, the premium dropped to its lowest over ICIS’s three-year price records at just €0.08/kg H2 hydrogen for low-carbon ATR.

The key driver behind the lower premium for low-carbon hydrogen delivering in 2024 has been the carbon price. The December 2024 EUA contract settled at €34.71/tCO2e on Jan. 4 but rose progressively over the year to record levels, peaking on Dec. 8, breaching €91/tCO2e.

Given ICIS gas and power assessments published on Dec. 17, a carbon price of €98/tCO2e would make unabated SMR more expensive than low-carbon ATR.

The rise in carbon prices had a bigger impact on the premium between technology streams for far-curve contracts. This was because far-curve power and gas prices remained well below the near curve.

For example, the premium for low-carbon SMR for year+3 dropped from €0.50/kg H2 to €0.28/kg H2 between Jan. 4 to Dec. 17, 2021, while front-month based premiums for the same technology widened to €1.21/kg H2 over the same period, up from €0.60/kg.

This is because higher power prices also impact low-carbon hydrogen technologies due to power demand for the CCS process, balancing the rise in the carbon price. Power prices weigh on low-carbon ATR more than low-carbon SMR, as power is required for the air separation unit used to produce pure oxygen for the ATR hydrogen production process.

Despite slightly higher power demand over low-carbon SMR and unabated SMR, low-carbon ATR is a more efficient production process, meaning less natural gas is required per kg of hydrogen, a contributing factor behind the record-low premium recorded on Dec. 8.

Renewable Hydrogen

One means of avoiding price volatility such as that seen over the spot market in 2021 would be via securing a long-term power purchase agreement (PPA).

A PPA is an agreement signed with an energy supplier that locks in a commodity’s price for the duration of the contract. For renewable projects, developers can sign PPAs to provide the project with financial support.

An ICIS analysis conducted in November 2021 showed that a long-term PPA of around €53/MWh would result in a hydrogen price of around €4/MWh for the duration of the contract. This means that such PPA-supplied hydrogen would have been cheaper than front-month unabated SMR towards the third quarter.

However, market information on PPAs indicates that such long-term contracts are also rising in price amid the commodity price spike.

Given current Dutch power market spot prices, PPAs could still result in a cheaper hydrogen price compared to purchasing power supply from the wholesale market. However, far-curve gas contracts have remained low enough to keep low-carbon hydrogen via ATR or SMR cheaper than PPA-derived hydrogen were you to sign a contract in the current market.

—Jake Stones, Hydrogen Editor, ICIS. ICIS—Independent Commodity Intelligence Services—connects data, markets and customers to create a comprehensive trusted view of global commodities markets, enabling smarter business decisions that help optimize the world’s resources.