In 2010 investment in wind power continued to accelerate, particularly in California and Texas. California also entered several solar projects in the race for financing. The finish line that renewable power developers and their partners are racing to meet is a December 31 deadline to qualify for federal cash grants.

December 31 is the deadline that renewable power developers are racing to meet. That is when renewable energy project developers that are seeking cash grants from the U.S. government must have their projects approved and a small percentage of each project under way. So throughout 2010, particularly in the third and fourth quarters, there has been a “mad dash for cash,” as developers, regulators, investors, and channel partners (those covering the entire lifecycle of a technology) work long and hard to make sure their projects meet qualifications for the Section 1603 Cash Grants, established as part of the American Recovery and Reinvestment Act of 2009 (ARRA).

California Sets the Pace

As is often the case, California set the pace for the rush to renewables. Data tracked by Industrial Info Resources show that 13 renewable energy projects with an aggregate generating capacity of 2,186 MW were scheduled to kick off in the state this year. Concentrated solar power (CSP) was by far the leading type of renewable energy project scheduled to break ground in California during 2010, accounting for 1,256 MW of the state’s new renewable generation.

By technology type, the other renewable energy projects scheduled to start in California this year include:

- Wind power, 6 projects, 650 MW

- Photovoltaics, 1 project, 230 MW

- Geothermal, 1 project, 50 MW

The Golden State, which was requiring utilities to obtain 20% of their electricity from renewable sources in 2010, further increased its renewable energy standard (RES). In September, the state’s Air Resources Board (ARB) ruled that 33% of California’s electricity must come from renewable energy sources by 2020. The ARB action was another step toward fulfilling A.B. 32, a state law passed in 2006 that mandated lowering California’s greenhouse gas emissions to 1990 levels by 2020.

California’s 33% RES “is going to further diversify and secure our energy supply while also growing California’s leading green technology market, which will lead to cost savings for consumers,” ARB Chairman Mary D. Nichols said in a statement.

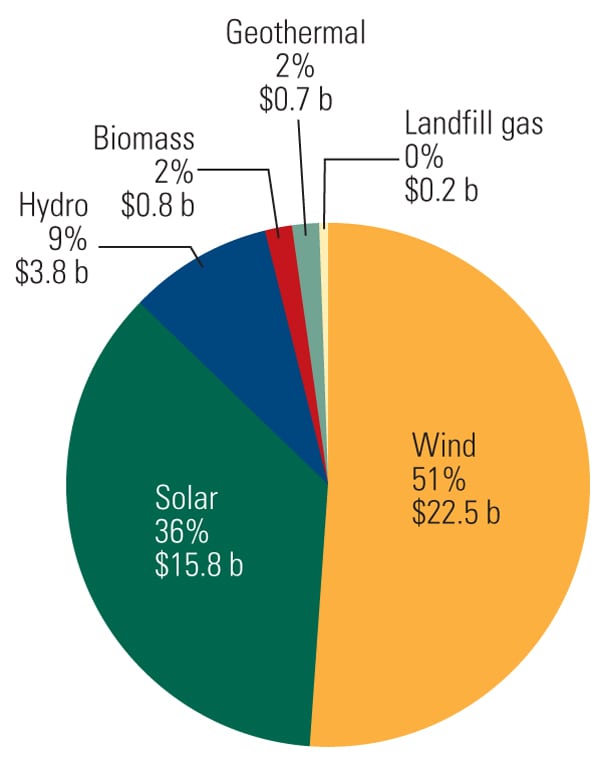

Though it is perhaps most obvious in California, the rush to renewables is also evident across the U.S. and Canada. Across North America, Industrial Info Resources is tracking $43.8 billion in renewable energy generation projects that are scheduled to kick off in 2010. Wind power is scheduled to garner the lion’s share of this investment at 51% ($22.5 billion), followed by solar at 36% ($15.8 billion), hydro at slightly less than 9% ($3.8 billion), biomass (about 2%, or $800 million), geothermal (about 1.6%, or $700 million), and landfill gas (about 0.5%, or $200 million), as illustrated in the figure.

Projects Slow to Start

In our experience, many, if not most, power projects do not proceed according to their original schedules. This is especially true for renewable energy projects. It is also our experience that renewable projects tend to have higher rates of deferral and abandonment than gas- or coal-fired projects, usually because of power purchase agreement negotiations or the availability of financing. Industrial Info Resources tracks power projects according to the kick-off date specified by the project developer.

As a case in point, Industrial Info Resources’ data show that 181 renewable energy projects totaling 13,888 MW of generating capacity are scheduled to kick off in the U.S. during 2010. But at the end of the third quarter, 77 projects representing 7,750 MW of capacity had not yet begun construction.

So although our data reflect a total of 145,000 MW of renewable generation that is scheduled to kick off during the 2011–2015 period, we expect only about 20% of this capacity will move forward. Using history as our guide, we expect that most projects will be delayed, deferred, or abandoned.

|

| North American renewable power projects spending breakdown. This chart illustrates how spending is distributed for projects scheduled to kick off in 2010. Source: Industrial Info Resources |

Renewables Gaining Ground Despite the Odds

Each year, Industrial Info Resources prepares a five-year rolling total of scheduled generating projects according to fuel type. For the 2011–2015 period, renewables (principally wind power) are scheduled to account for about 60% of all new generating capacity additions in the U.S. Last year, our five-year spending projection said renewables would account for 46% of all new generation to be built between 2010 and 2014. In an earlier projection, renewables were scheduled to account for 33% of the generation capacity built in the U.S. over the period of 2008–2012.

Across the U.S., a continuing trend was that investments in renewables came at the expense of other fuels—chiefly coal and nuclear. Coal’s share of new generating projects slipped from 28% over the 2008–2012 period to 17% during 2010–2014 to 7% during the 2011–2015 period. Nuclear’s share of new generation construction fell from 20% over the 2008–2012 period to 11% during 2010–2015, before rising to 13% for the 2011–2015 period.

The rush to renewables is evident across all regions in the U.S. On a megawatt basis, between 2011 and 2015, project developers have announced plans to have renewables account for:

- 73% of the new generating capacity proposed for the West Coast, up from 54% of new capacity between 2008 and 2012.

- 71% of the new generating capacity proposed for the Rocky Mountain area, up from 25% of new capacity during the 2008–2012 period.

- 85% of the new generating capacity proposed for the Midwest, up from 39% of new capacity to be built between 2008 and 2012.

Power developers also have announced plans to increase the share of renewables in the new power generation mix between 2011 and 2015 in the Southeast, Southwest, and New England areas.

The embrace of renewables in the U.S. comes despite markedly higher construction costs for renewable capacity (see table), relatively high unemployment, weak economic growth, and the uncertainty that comes with mid-term elections.

|

| Capital costs. The cost to build new electric generation capacity in the U.S. varies widely, according to project-spending data tracked by Industrial Info Resources. The data are rank-ordered on the basis of cost per megawatt of installed capacity. Source: Industrial Info Resources |

Beat the Clock

The calendar will determine exactly how many of these planned renewable energy projects actually break ground. The Section 1603 program provided renewable power developers with a cash grant of up to 30% of a project’s value, instead of investment or production tax credits, as long as their projects actually began construction by year-end 2010. Throughout 2010, especially during the third quarter and the early part of the fourth quarter, we have seen the dash for cash among project developers translate into long hours and increased business for equipment providers and engineering and construction companies.

Without the renewal of the Section 1603 cash grant program, many otherwise worthy renewable energy projects may not begin construction, although some could continue to move forward using the promise of federal investment or production tax credits. During the summer, efforts to extend the Section 1603 cash grant program were shot down by a suddenly budget-conscious Congress. But as autumn began, an intense lobbying effort by renewable energy developers and organizations may have increased the chances for an extension beyond year-end 2010. Observers say a Section 1603 extension may be attached to a piece of “must-pass” legislation such as the renewal of the Bush administration’s tax cuts or a continuing resolution funding the operation of the U.S. government.

Intense lobbying by renewable energy organizations did succeed in the introduction of a narrow bill that would establish a national RES of 15% by 2021. The bill, introduced in late September by Sens. Jeff Bingaman (D-N.M.) and Sam Brownback (R-Kan.), attracted more than 25 co-sponsors within one week, including several Republicans, which could bolster the bill’s chance of surviving a cloture vote on the Senate floor. With the Senate in recess for October, any RES bill would have to be considered by a lame-duck session of Congress, convening after the elections in November but before a new Congress is seated in January. In the Senate, the inability to muster the 60 votes necessary to defeat a cloture vote is what stalled comprehensive energy legislation during most of 2010.

It will be some time into 2011 before we know exactly how many renewable energy projects started construction in the U.S. in late 2010. But one thing is clear: The aftermarket for wind power equipment maintenance and replacement is an emerging multi-billion-dollar business opportunity. Over the next three years, at least 8,000 MW of wind power per year are coming off warranty. Companies that manufacture or service wind turbine gearboxes, rotors, turbines, and other machinery are expected to be busy chasing maintenance and overhaul projects for the next several years. â–

— Britt Burt (bburt@industrialinfo.com) is vice president of research and Shane Mullins (smullins@industrialinfo.com) is vice president of product development for the power industry at Industrial Info Resources (http://www.industrialinfo.com) in Sugar Land, Texas.