The fog of uncertainty that hangs over the global power industry is getting larger and denser as generating companies and utilities navigate ever more complex challenges.

High-level scenarios often paint the energy transition as a smooth trajectory—a gradual evolution toward a more modern, cleaner, more intelligent system that addresses climate change, as well as furnishes the world with secure, affordable energy. In reality, change often has sharp edges, and in the vast and diverse power space, it can be volatile and disjointed, characterized by friction and imbalances among its many participating entities.

As a critical infrastructure industry whose primary mission is to provide safe, reliable electricity, the power sector has always faced some degree of uncertainty and change, and many companies have mature risk measures and controls in place for their networks and assets. But as overall system complexity ramps up, POWER’s analysis suggests they are now facing a lengthy list of looming exposures. Several industry experts from insurance, financial consultancy, and market rating firms pointed out to POWER that many existing risks are rooted in the industry’s changing business profile, specifically related to potential impacts from decarbonization and past reliance on natural resources. Newer risks, however, can be pegged to pandemic tumult that has had a broader reach, they suggested.

“The world as we know it is being completely reshaped. No country or company will simply bounce back or rebound to the way they were before. Consumer behaviors are changing, supply chains are being rewritten, institutions are shuttering, business models are being fundamentally reshaped, and expectations of governments are shifting. Energy as a sector will be no different,” noted Aon plc., a global professional services firm that provides a broad range of risk, retirement, and health solutions.

While the level of risk can’t be easily quantified given the array or markets, applications, and size of operation, the following are some risks to which experts called specific attention. While not detailed here, stakeholders notably also highlighted risks related to fuel uncertainty, business model overhauls—including through mergers and acquisitions—asset divestment and decommissioning, safety, and geopolitical concerns, such as trade disputes and political volatility.

Natural Disasters. Climate change is adding new stressors to power operations, and that is raising a paramount interest in resiliency against severe weather events for power companies and utilities. According to the Edison Electric Institute (EEI), a trade group representing all U.S. investor-owned utilities, “risks are differing in different parts of the country and evolving,” which is why they require specific planning for mitigation. Examples include risks of hurricanes, floods, wildfires (Figure 1), and extreme heat or cold events, as well as decreasing water availability. Since Superstorm Sandy in 2012, EEI said its members have invested more than $340 billion to harden their investments.

In This Issue

Full issue |

|

1. Pacific Gas & Electric (PG&E) in July announced it would bury about 10% of its transmission and distribution lines to prevent wildfires in projects that could cost up to $30 billion. Courtesy: PG&E |

Reliability and Environmental Compliance Requirements. The extreme cold weather event that forced three grid operators, most prominently in Texas, to implement rolling blackouts last February, and the summer 2020 heat wave–related brownouts in California, resulted in billions of dollars in losses for market participants and highlighted supply-demand mismatches. Ensuing reliability measures may require costly generator upgrades. Environmental compliance has meanwhile prompted a wider spate of coal and gas plant closures in the U.S. Government-announced phaseouts have meanwhile prompted closures of coal and nuclear plants across Europe, China, and South Korea.

Regulatory Uncertainty. In the U.S., efforts to address climate change and resiliency, customer preferences, and technologies that promise to integrate renewables, electric vehicles, and digitalization are “crashing up against sluggish century old regulatory paradigms,” said Brien J. Sheahan, former chairman and CEO of the Illinois Commerce Commission and former chairman of the National Association of Regulatory Utility Commissioners’ Presidential Task Force on Innovation. Mandates related to data privacy, cybersecurity, supply chains, and other evolving areas are also an emerging concern. Meanwhile, environmental, social, and governance (ESG) concerns “pressed upon utilities by both their boards and regulators are an immediate risk to utilities,” Michael Pignataro, regional head of Energy and Construction North America for global corporate insurance carrier Allianz Global Corporate and Specialty, told POWER. These concerns will require long-term planning and execution in the form of investment and divestment. “Conversely, they are subject to the quarterly and election-cycle mindset of shareholders and politicians,” he said.

The ESG Boon and Burden. Heightened pressure from investors that is informed by ESG, a metric that gauges corporate sustainability, is prompting financial institutions—including banks, insurers, and brokers to halt financial support or coverage for the traditional coal-fired power sector. But ESG considerations may also have negative credit implications for all utilities that own generation owing to their high exposure to extreme weather risk, Moody’s Investors Service said in a June 2021 report that looked at 71 global holding companies. “We are already seeing trends emerge, aligned to the increasing influence of ESG, however a rapid escalation in pressure would result in a significant increase in on-balance sheet exposures, forcing many more firms to dramatically change their energy mix,” noted Aon.

A Changing Customer Base. Utilities committed to ESG criteria are generally pushing to be more customer-centric, but according to consulting firm EY’s Energy Transition Consumer Survey, they are increasingly catering to the “omnisumer”—a person or business entity who participates in a dynamic energy ecosystem across a multitude of places, solutions, and providers. “Energy providers are grappling with multiple challenges but meeting rapidly changing customer expectations may be the toughest yet. We believe that an enterprise-wide focus on transforming the customer experience—driven by the workforce, powered by consumer insights, and supported by digital technology—is the winning strategy. This means harnessing agile ways of working and creating a culture to constantly improve, innovate, and put people first,” said Greg Guthridge, EY Global Power & Utilities Customer Experience Transformation Leader.

Technology Risks. Power companies have typically carried substantial risk associated with their generating technologies, but they face elevated risks associated both with obsolete models as well as new ones. For example, “Certain older steam turbines have design issues that make them virtually uninsurable; furthermore, carriers also continue to encounter problems with the ‘quick start’ aeroderivative/frame machines. Obtaining spare parts and rotors for certain machines is challenging, which is driving up loss costs,” noted global insurance-related service provider Willis Towers Watson. “An average turbine loss costs significantly more than in past years, due to the limited availability of replacement parts, increased costs for component parts and larger machines; this is partly why carriers are requiring higher deductibles.” Newer gas turbine models, including the larger H- and J-class machines, are “both expensive and prototypical,” the firm said. “Although carriers didn’t pay any significant losses in 2020 involving these machines, it is possible that some events did occur with OEMs [original equipment manufacturers] picking up the tab under warranty. Given the large size and cost of these units, when losses involving these large machines do occur, repair costs will dwarf the costs of older combustion turbines.”

Over the last 10 years, meanwhile, renewable energy insurance has also been characterized by “some significant losses that have resulted in the market altering terms in order to compensate,” said GCube, a leading underwriter for renewable energy projects around the world. “Moreover, as the wind and solar industries have expanded in scale, proliferated into more extreme environments, and brought a raft of new products into the market, claims severity has increased. With insurance premiums resetting to a new base, renewable energy project operators face increasing insurance costs.”

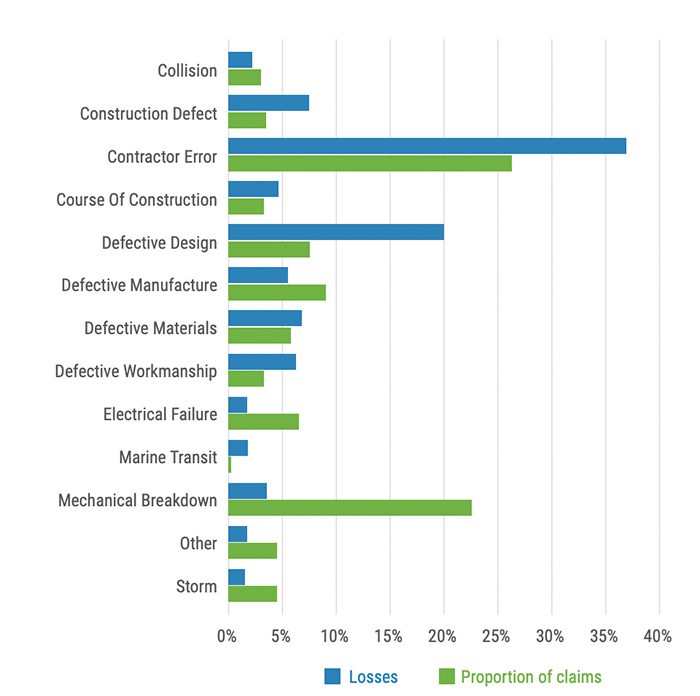

GCube specifically highlighted challenges with the offshore wind industry, where it warns an increased focus on cost-competitiveness has led to “prolific cost-cutting in the design, manufacture, construction, and operation of offshore wind” over the past decade. However, that quest for competitiveness “has increasingly come at the expense of quality control, increasing the frequency and severity of insurance claims in the sector, and putting pressure on a strained insurance market,” it said. Recent combined market losses in offshore wind have quadrupled in the last five years, the company claims (Figure 2). “Put simply, the insurance sector must take a more unified approach to writing offshore wind insurance, and the supply chain must accept its share of accountability on offshore wind claims,” said GCube CEO Fraser McLachlan.

|

|

2. GCube, a renewables project underwriter, suggests the most common sources of offshore wind insurance claims by far are contractor error and defects across design, manufacture, workmanship, and construction. The company in November said that the average size of an offshore wind insurance claim has shot up over the past five years. Between 2010 and 2015, the average loss was $2.2 million; whereas, between 2016 and 2020, the average loss was $4.1 million, showing a notable rise in claims severity. Courtesy: GCube |

Attracting Talent. Attracting and retaining talent is also an immediate challenge for many power companies. “The majority of utility employees are approaching retirement age, and the availability of a replacement workforce is questionable,” explained Allianz’s Pignataro. “The ability for an aging workforce to maintain our aging power infrastructure under increased consumer demand is a primary concern. The lead-time in attracting, training, and retaining the workforce of the future presents an immediate threat to the stability of the system.”

Supply Chain Risks. While exacerbated by the pandemic, supply chain bottlenecks have long been a concern for power companies, which are essentially end-users of electrical equipment. In the U.S., utilities face specific vulnerabilities because, in many instances, the industry lacks viable or cost-competitive domestic sources for critical equipment. Equipment procurements, notably, involve months, sometimes years, of costly budgeting, engineering, and planning before equipment can be put into production safely and reliably. “The number of manufacturers and suppliers of power generation equipment, particularly turbines and transformers, is both limited and highly consolidated,” noted Pignataro. “A disruption in the operations of one or many of these companies will have extreme impacts on equipment supply. Similarly, an interconnected catastrophic event could result in unsupportable enhanced short-term demand. The barriers to entry of these industries prevents upstarts. It is my opinion that governments should purchase and store power generation equipment as a part of its national security strategy.”

Supply chain security, however, is also a growing concern. In May 2020, President Trump issued an executive order prohibiting the acquisition, importation, transfer, or installation of certain bulk electric equipment sourced from foreign adversaries. Responding to the U.S. Department of Energy’s (DOE’s) recent actions to coordinate with the power sector to ensure procurement practices and requirements evolve to match changes in the threat landscape, the EEI recently said the sector already uses many existing tools, methods, and programs to address potential security vulnerabilities. The organization noted, however, that if the DOE takes initiatives to improve electric company security posture, they should be flexible and “recognize the unique threats individual electric companies face due to their system design and topology, customer base, and existing security controls.” According to EEI, large power companies typically address supply chain risk management “in a risk-based, defense-in-depth manner using tools that are integrated into electric companies’ security culture, most notably by prioritizing protections for supply chain equipment in the most critical pathways.”

Cybersecurity. More digitalization in the power sector has raised its vulnerabilities to cyberattacks. Despite compliance with the North American Electric Reliability Corp.’s (NERC’s) critical-infrastructure protection standards and other industry requirements, “many security functions face continual stress from addressing gaps identified in ongoing site-specific or regional-level security assessments,” said McKinsey and Company. According to Moody’s, however, larger, more highly regulated, privately owned firms appear best able to manage this growing risk. A survey the ratings agency conducted in 2020 of global electric utilities showed that “large, privately owned regulated utilities have more robust cyber risk governance and management practices in place than state-owned or unregulated and not-for-profit peers,” said Moody’s analyst Lesley Ritter. “Smaller utilities, not-for-profits in particular, favor a risk transfer approach to cyber risk mitigation.”

Construction. Construction of new power projects, too, is ridden with risk. Allianz in December told POWER that it expects a boom in global construction driven by the transition to a low-carbon or net-zero economy, with a specific focus on a build out of wind, solar, hydrogen, storage, and transmission. “This boom in global construction will, however, present challenges for the construction and engineering sector, and their insurers,” the company said. “In the medium term, sudden surges in growth could put supply chains under additional pressure and exacerbate the existing shortage of skilled labor. Longer term, huge investments in green energy will mean larger values at risk, while the rapid adoption of unproven technology, building methods, and materials will require close cooperation between underwriting, claims, and risk engineering, as well as between insurers and their clients.”

—Sonal Patel is a POWER senior associate editor (@sonalcpatel, @POWERmagazine).