A once-predictable industry is moving at hyperscale speed. Here are five trends defining the biggest gas power buildout in a generation.

Natural gas power is in the middle of its biggest buildout in a generation, driven by an electricity demand surge that few saw coming at this speed or this scale. The rules that governed how gas plants get developed, financed, and built are being rewritten in real time. Following are five ways gas power is rewriting its own rules.

1. Speed to Scale

A phrase that started in PJM’s market monitor reports is fast becoming the operating principle of the entire gas power buildout: “bring your own generation” or BYOG. On its face, the idea is simple: Because data centers can’t wait for utilities to plan, permit, and build adequate capacity, they are moving to finance their own generation and demanding it be delivered quickly. In some instances, the speed imperative has replaced cost as the deal-winning variable, and every decision downstream—contracts, procurement, financing, engineering sequence—is now seemingly being restructured around it.

Across the industry, the adjustment is visible in procurement architecture. Owners who once left heat recovery steam generators, transformers, and switchgear to their engineering, procurement, and construction (EPC) contractors are now buying long-lead equipment directly—sometimes before permits are secured. Lump-sum turnkey contracts are giving way to target-price frameworks with fixed fees and shared savings. And major regulated utilities, including Xcel Energy, are locking in turbine supply agreements years in advance in moves their executives describe as building the “clock speed” the market now demands.

2. The Market Has Already Answered

From Texas to the mid-Atlantic, demand growth is fueling new prospects for gas power.

Electric Reliability Council of Texas (ERCOT). Texas is carrying more than 230 GW of new load requests in its interconnection queue—70% data center driven—which could roughly double the state’s current peak if it fully materializes. Keith Collins, ERCOT’s vice president of Commercial Operations, noted that peak system stress has shifted from the traditional 4 p.m. to 5 p.m. window to 8 p.m. to 9 p.m., just as solar resources fall, forcing gas to carry the load. Batteries, which average 1.5-hour duration, cannot bridge a winter double-peak, he noted.

Southwest Power Pool (SPP). Thermal interconnection requests—predominantly natural gas—have increased tenfold in a single year in SPP. “Three or four years ago, data centers weren’t even in our forecast,” said Casey Cathey, SPP’s vice president of Engineering. Today the region is seeing 4%–5% annual load growth—“unheard of in 20-plus years”—with 110 GW of generation requests queued against a 56 GW peak. Gas generation remains essential to balance SPP’s 35 GW of wind resources and support system reliability, he said.

Midcontinent Independent System Operator (MISO). The operator serving 45 million customers formally lists “fewer synchronous resources and more inverters” as an active system stability risk in its February-updated 2026 Reliability Imperative Report. For now, gas power is “beginning to re-emerge where firm capacity is needed”—even as 52 GW of approved generation awaits construction and 32 GW of that reports commercial operation date delays.

PJM Interconnection. Gas power cleared 45% of the 2026/27 Base Residual Auction—nuclear, coal, hydro, wind, and solar combined cleared 51%—at the price cap of $329.17/MW-day. That represents roughly an 800% increase over two auction cycles.

3. New Business Models, New Buyers Emerging Amid Cutthroat Race

Beyond reshaping what gets built, the gas turbine boom also appears to be shifting who builds it, who owns it, and who pays for it. Three distinct business models are competing in the race to render molecules to megawatts.

The first is the traditional regulated utility, which has been pouring ever-growing investment into new capacity. NextEra Energy anticipates investing between $90 billion and $100 billion over the next six years through its Florida Power & Light unit and has told investors it expects to develop 15–30 GW of new generation capacity for U.S. data centers by 2035. More than 20 GW will come from gas-fired generation. Xcel Energy is planning a $60 billion base capital investment for 2026–2030—up from $45 billion in the prior cycle—driven almost entirely by artificial intelligence (AI) and data center load growth in its service territories.

The second model involves merchant generators, which are also moving aggressively to build speculative capacity and sell it under long-term power purchase agreements. Vistra acquired 2.6 GW of modern natural gas generation assets from Lotus Infrastructure Partners in 2025 and is completing the Cogentrix acquisition in mid-2026, which adds a further 5.5 GW. Upon closing, Vistra will operate approximately 26 GW of gas generation capability. Constellation Energy, following its acquisition of Calpine, is marketing what it calls “clean firm power”—nuclear baseload paired with gas peaking capacity—directly to hyperscalers seeking round-the-clock reliability. NRG Energy is pursuing a similar scale strategy: its acquisition of LS Power’s generation portfolio nearly doubled its fleet to about 25 GW—including roughly 13 GW of modern natural gas assets—while adding CPower’s commercial and industrial virtual power plant platform. The company has already secured 445 MW of long-term agreements extending to 2032 in ERCOT and PJM, and is developing more than 5 GW of new combined cycle capacity through a joint venture with GE Vernova and Kiewit aimed at serving rapidly growing data center demand.

The third model seeks to cut out the utility entirely, and the White House recently endorsed it in its Ratepayer Protection Pledge, under which seven hyperscalers committed to “build, bring, or buy” their own generation and cover the full cost of infrastructure upgrades required to deliver them. But even without it, gas power buildout under the model was already gaining traction. Recently, for example, Babcock & Wilcox received full notice to proceed on a $2.4 billion design-build contract with Base Electron to supply 1.2 GW of natural gas–fired boilers and steam turbine generator systems powering Applied Digital’s AI campuses, with an option for another 1.2 GW. Elon Musk’s xAI secured a Mississippi permit for a 41-turbine gas-fired plant to power its data centers directly, while Atlas Energy Solutions signed an $840 million framework agreement with Caterpillar to secure approximately 1.4 GW of behind-the-meter generation assets through 2029.

4. A Tight Market for Gas Turbines

Every major original equipment manufacturer (OEM) kicked off 2026 with record backlogs, rising prices, and delivery slots filling into the early 2030s.

GE Vernova. The company entered 2026 with 83 GW of gas power equipment under firm order or slot reservation—up from 62 GW one quarter earlier—after signing 24 GW of new contracts in the fourth quarter (Q4) 2025 alone, including 6 GW in the final three weeks of December. CEO Scott Strazik told investors that current slot reservations are priced “another 10 to 20 points” higher than existing backlog orders. The company is targeting 100 GW under contract by year-end 2026, added nearly 1,000 production workers in 2025, and plans an incremental 200 machines and 500 additional workers in 2026, ramping annual capacity to approximately 20 GW by mid-year.

Siemens Energy. In just the first quarter of fiscal year (FY) 2026, Gas Services “booked 102 gas turbines”—matching more than 50% of last year’s unit volume in a single quarter, CEO Christian Bruch told analysts on Feb. 11. Total gas commitments stand at 80 GW, including 22 GW tied to data centers, though data centers “still represent only one quarter of our total global commitments.” Pricing and lead times are both moving in one direction. Siemens Energy is backing its growth with a $1 billion U.S. manufacturing expansion across six states, adding 1,500 jobs and resuming gas turbine production in North Carolina.

Baker Hughes. The Houston-based company logged $2.5 billion in power systems orders in 2025, including $1 billion directly tied to data centers. Its NovaLT industrial turbine booked approximately 2 GW last year, with a 1 GW slot reservation secured in Q4 alone. The company targets $3 billion in total data center orders between 2025 and 2027.

Mitsubishi Power. The company’s 10-year U.S. market forecast for large turbines nearly doubled in a single year. Its JAC-series—more than 90% of its U.S. large turbine sales—is in full production ramp-up, backed by a new 120,000-square-foot parts distribution hub opened in Orlando in early 2025. Parent MHI booked 31 large-frame gas turbine contracts in the first nine months of FY2025, up 15 units year-on-year. “Demand for gas turbines remains high, particularly in the U.S.,” CFO Hiroshi Nishio said in February 2026.

5. A Global Buildout That Is Vulnerable to Geopolitical Risk

The gas power boom extends globally, and according to some analysts, could only grow given the urgency for scale and speed. Data center electricity consumption is projected to double to 800–1,000 TWh by 2030, driven in large part by the U.S. and China. In Dublin, data centers consumed 22% of Ireland’s national electricity in 2024, a figure projected to exceed 30% by 2027. And in the Middle East, sovereign-backed mega-campuses are pairing gas turbines with utility-scale solar in integrated campus-plus-power developments, leveraging abundant gas to guarantee the round-the-clock reliability that data center customers need.

|

|

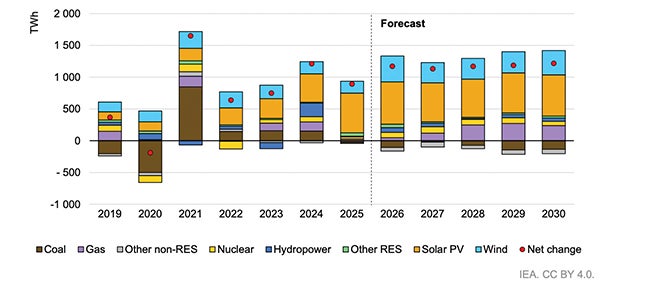

1. Global gas-fired power generation is projected to grow 2.6% annually from 2026 to 2030, driven by strong expansion in the U.S. and rising electricity demand in the Middle East, where countries such as Saudi Arabia are accelerating oil-to-gas switching. Courtesy: International Energy Agency, Electricity 2026 (February 2026) |

According to the International Gas Union (IGU), gas-fired generation for data centers could expand by approximately 30 billion cubic meters by 2030 and nearly double again by 2035. The International Energy Agency (IEA), meanwhile, projects that gas-fired generation could grow at 2.6% annually through 2030—the only fossil fuel that is expected to soar in its outlook—as one of the only viable firm, flexible resources that is already balancing grids that are increasingly dependent on variable renewables (Figure 1).

Yet, gas power’s trajectory is still clouded by disruption. Approximately 20% of globally traded liquefied natural gas (LNG) moves through the Strait of Hormuz, primarily from Qatar. A two-week interruption from the Iran conflict (ongoing as of this writing in early March), is poised to spike gas prices 10%–20% across most Asian and European markets, says a March 2026 analysis by global advisory firm Teneo. That could have steep repercussions for LNG-dependent markets like the UK and Japan. If the disruption spans more than two months, it could push European prices up between 60% and 120%, U.S. prices 15%–50%, and UK wholesale electricity prices 25%–100%. “If the AI revolution has served as a reminder of the centrality of energy to geoeconomics,” wrote Teneo’s Head of Energy Dan Gabaldon, “this conflict is reminding us how globalized and geopolitically relevant the once very local gas and power markets have become.”

—Sonal Patel is senior editor at POWER magazine (@sonalcpatel, @POWERmagazine).