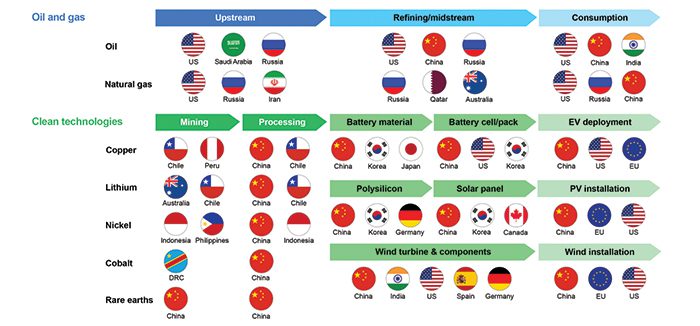

Washington, D.C., has spent the past five years fixating on rare earths—where they’re mined, how they’re processed, and who controls the magnet supply chain. That attention is overdue.

But the national conversation still stops one link too soon. The real compounding bottleneck isn’t just the magnets, it’s the motors and drives that use those magnets—traction motors in electric vehicles (EVs), generators in wind turbines, high-efficiency industrial drives on factory floors, and electric motors used in naval propulsion and aerospace subsystems. Magnet output alone does not translate into the domestic capability to produce high-value end-use systems. Until North America builds more of those motors, drives, and generators at scale, materials security will remain a mirage.

COMMENTARY

Every mainstream high-frequency electric motor—especially permanent-magnet designs and modern inverter-driven induction motors—relies on non-oriented electrical steel (NOES) for its stator/rotor laminations.

While induction motors can tolerate a wider range of materials at lower speeds, high-efficiency, high-frequency operation still depends on thin Fe-Si laminations with high magnetic permeability and low core loss. These properties enable EV traction motors to operate at 15,000+ rpm without overheating or excessive energy loss. The U.S. currently produces only a fraction of the high-grade NOES required for modern EV and industrial drives; the most advanced grades (0.25 mm or thinner, with more than 3% silicon and specialized coatings) are produced primarily in Japan, Korea, and Europe. Without domestic NOES capacity, even “U.S.-made” motors depend on imported laminations—leaving a major blind spot in America’s materials and manufacturing strategy.

The Role of Industry

The demand side is unambiguous. The International Energy Agency’s latest “Global Critical Minerals Outlook” shows sustained growth in clean energy demand for critical minerals—including rare earths—driven by the rapid deployment of permanent-magnet motors and generators across EVs, wind, and industrial systems. The National Renewable Energy Laboratory’s (NREL’s—also known as National Lab of the Rockies) comparative generator studies explain why: permanent magnets reduce mass, improve efficiency, and lower total system cost. Today’s permanent-magnet direct-drive generators can require hundreds of kilograms of rare-earth-containing magnet material per megawatt, creating enormous pull on a still-concentrated upstream supply chain.

Meanwhile, the U.S. debate still treats “motors” as a rounding error. Yet motors and drives are where magnet supply becomes industrial strategy. They are heavy, customized systems, tightly integrated with power electronics and typically built near end markets by firms with deep application expertise. And that is exactly where America’s manufacturing footprint is thinnest—particularly in the fastest-growing, highest-value segments relative to demand growth.

More telling is what major firms are already doing. In traction motors and e-axles, companies such as BorgWarner, Dana, AISIN, and Valeo are scaling production programs close to vehicle assembly hubs. Nidec (Japan)—the world’s largest motor manufacturer—has rolled out global e-axle platforms and is adding North American capacity, including a major EV drive-unit plant in Mexico, to serve the regional market. In China, it has experimented with localized supply chains for its latest e-axles. The strategy is clear: build motors where the vehicles are built.

Bosch (Germany) is producing permanent-magnet electric motors in Charleston, South Carolina, as part of a broader North American electrification build-out. ZF (Germany) has scaled EV motor production across Europe and Asia and is simultaneously commercializing magnet-free variants—a useful reminder that engineering choices can shift materials exposure, but are unlikely to eliminate permanent-magnet demand this decade.

On the industrial side, Innomotics (Siemens’ former motors business) manufactures permanent-magnet motors in Germany, the Czech Republic, Romania, China and the U.S. (Norwood, Mass.). These products underpin high-efficiency industrial drives used across manufacturing, infrastructure, and energy systems. ABB (Switzerland), a leading supplier of industrial drives and permanent-magnet generators, is expanding U.S. manufacturing to better serve local customers. That matters because variable-speed industrial drive systems—often paired with permanent- magnet motors—are among the lowest cost ways to reduce electricity consumption in American industry.

WEG (Brazil) supplies motors and drives globally from manufacturing hubs in Brazil, the U.S., Mexico, China, and Europe, and is expanding capacity both at home and in the U.S.—evidence that scale producers are positioning production close to growth markets in the Americas. In wind, Siemens Gamesa’s permanent-magnet direct-drive platform has become a de facto standard in offshore turbines, and the company has begun working with suppliers to explore localized magnet production in Europe—an instructive model for de-risking entire product chains rather than focusing narrowly on raw materials.

Taken together, these examples point to a clear pattern: globally competitive firms are anchoring motor, drive, and generator manufacturing close to final assembly and end markets—and pulling upstream materials, components, and know-how along with them. The U.S., by contrast, has focused disproportionately on upstream inputs while allowing much of the value-dense electromechanical manufacturing layer for next generation electrified systems to remain thin or offshore. The result is a structural mismatch: growing domestic demand for electrified systems paired with limited domestic capacity to produce the motors and drives that define their performance, cost, and efficiency. Until that gap is addressed, efforts to secure magnet and rare-earth supply chains will remain incomplete.

What Can Help?

Three policies could help secure the full supply chain.

First, recast the rare-earth permanent-magnet conversation as a motors-and-drives strategy. The Department of Energy’s clean energy supply-chain assessments correctly highlight that sintered NdFeB magnets are foundational to multiple clean-energy technologies. But unless those magnets are converted into U.S.-made traction motors, wind generators, and IE5-class industrial motors, America will continue to import the highest-value components—along with the jobs, know-how, and learning curves that accompany them. A materials-first strategy without a manufacturing-first strategy is incomplete. Framing matters: policymakers, stakeholders, and the American public must be clear about what the nation is ultimately trying to build if this conversation—and the necessary pivot in policy—are to succeed.

Second, adapt the incentives that worked for batteries. The tools that accelerated U.S. cell and pack production can be recalibrated for motors and drives. Production tax credits and local-content requirements tied to complete drive units (motor, inverter, and gearbox) would reward manufacturers for building integrated systems domestically—not merely sourcing individual magnets or laminations. Federal procurement—from postal vehicles to military support platforms, port equipment, and federal facilities—can reinforce this shift by specifying high-efficiency domestically manufactured permanent-magnet motor-drive systems. Done correctly, these measures would help establish durable domestic capability while simultaneously improving energy performance across the federal fleet.

Third, push de-risking where the value accumulates. Europe’s wind champion is exploring magnet onshoring precisely because turbine manufacturing is anchored there. The U.S. should adopt the same end-product logic. For offshore wind, this means situating generator assembly and drivetrain manufacturing at U.S. ports and pulling magnet, lamination, casting, and machining capacity alongside them. For electrified transportation more broadly, federal incentives and procurement should reward domestic production of complete e-axles and motor-stator assemblies—not just upstream materials or isolated components. Supply chains follow final assembly, not the other way around.

America has learned to think in gigafactories for batteries. It’s time to think in motor factories and drive lines as well. Stockpiling—and even mining and processing—rare-earths will not solve the materials challenge if the high-value components that use them are still stamped, wound, and assembled elsewhere. Build the motors and drives here—and the rest of the supply chain will begin to align around U.S. industry.

—Morgan D. Bazilian, Ph.D., is director and professor at The Payne Institute for Public Policy at the Colorado School of Mines. Joseph Sopcisak is industry advisory board member for The Payne Institute.