American Electric Power, one of the premier generating utilities in the U.S., is caught between a deregulated rock—wholesale competitive capacity markets that don’t, in the company’s opinion, value solid equipment over ephemeral demand response—and a regulatory hard place of increasing federal government rules that devalue on-the-ground coal-fired generation. Add the competitive challenge of cheap natural gas as a generating fuel, and you get a coal-dominated generating system in transition.

Ohio-based American Electric Power (AEP), one of the most successful electric utilities in U.S. history, is “a company in transition,” says Mark McCullough, the company’s executive vice president for generation. In a November POWER interview, McCullough described how the company with 38 GW of generating capacity is moving from a system dominated by cheap, plentiful coal located in the regions it serves to something else: natural gas.

Coal Concentration Challenged on Multiple Fronts

“From an overall perspective,” McCullough said, “AEP today is in the mid-60s” for its systemwide percentage of coal generation. “We are in the low 20s for gas, and less than 5% nuclear. The rest is hydro and renewables.” That’s going to change.

Today and in the short term, AEP’s heavy reliance on coal is getting challenged by the burgeoning supply of cheap natural gas, much of it coming from fracked Marcellus and Utica shale formations in AEP’s service territory in the rust belt (Ohio, West Virginia, Indiana, Virginia) and Texas. Added to that market competition is a regulatory thrust driven by the Obama administration’s Environmental Protection Agency (EPA), principally the Mercury and Air Toxics Standards (MATS, now under review by the U.S. Supreme Court on the grounds of costs versus benefits) and the looming EPA global warming rules, the “Clean Power Plan,” grounded in Section 111(d) of the 1990 Clean Air Act. The timing of the climate rules, says McCullough, “doesn’t work for 2020. You can’t get there from here. The targets and the basis for the targets have a number of flaws. Our transmission folks and the Southwest Power Pool say the reliability issues are too difficult to solve.”

AEP’s immediate strategy involves investing heavily in its muscular transmission system, featuring more 765-kV transmission lines than all other U.S. transmission systems combined, along with moving some of its coal-fired plants away from competitive wholesale markets and into conventional state-based regulation. AEP’s transmission system is strategically positioned to take advantage of the growing cost-of-service market for transmission across large areas of the country. According to AEP, “Our transmission system supplies about 10 percent of the demand in the Eastern Interconnection, the transmission system that serves 38 U.S. states and eastern Canada, and 11 percent of the demand in ERCOT, covering much of Texas.”

Talking to Wall Street analysts last fall, AEP CEO Nick Akins said, “Keep in mind, we are in the middle of a multiyear plan to reposition our company, focused on infrastructure investments, particularly in the transmission and regulated utility lines of our business, improving our customer service through process and technology improvements, transforming our generation resources, and defining an employee culture that enables the adaptability, flexibility and entrepreneurship that the future will demand.” In early January, TheStreet.com reported that AEP had hired Goldman Schs to examine selling off the company’s 7,923-MW merchant generating business, with an expected sale price of $2.8 billion to $3.6 billion.

Part of AEP’s generation transition, as ElectricityPolicy.com detailed, is asking the Public Utilities Commission of Ohio (PUCO) to “guarantee income from four of its coal-fired power plants, which have had difficulty showing a profit in the PJM Interconnection’s forward capacity market. The plants were part of a restructuring that separated Ohio investor-owned utilities’ generation from their wires and retail service businesses.” The Ohio regulators in early December said they would hear AEP’s request for the Kyger Creek plant in southeastern Ohio, the first of the four stations the company wants to shift into state cost-of-service regulation. The 1955-vintage, 1,000-MW plant is jointly owned by AEP (43%) and FirstEnergy (21%), with the balance owned by other utilities.

The Columbus Dispatch reported, “Environmentalists, consumer advocates and competing electricity suppliers have come out against the plan, which they see as an unneeded subsidy that will prolong the life of a coal-fired power plant.” The PUCO staff has also opposed the utility’s plan, while the commission rejected its staff’s recommendation when it granted the hearing.

AEP has made a similar proposal for shielding its 50% share of the Mitchell plant in West Virginia from the wholesale market. It would spin off its 800-MW Mitchell share into tiny Wheeling Power, a West Virginia distribution utility run by AEP subsidiary Allegheny Power Co. and regulated by the Public Service Commission of West Virginia. ElectricityPolicy.com characterized the deal as “the mouse that was asked to swallow the elephant.”

FirstEnergy, based in Akron, Ohio, facing many of the same issues as AEP with regard to the wholesale markets, has also asked the Ohio commission to provide an umbrella of regulated prices for some of its coal-fired plants in order to protect against losses in the PJM capacity market. FirstEnergy owns the other half of the Mitchell plant.

A Newer Challenge: Demand Response

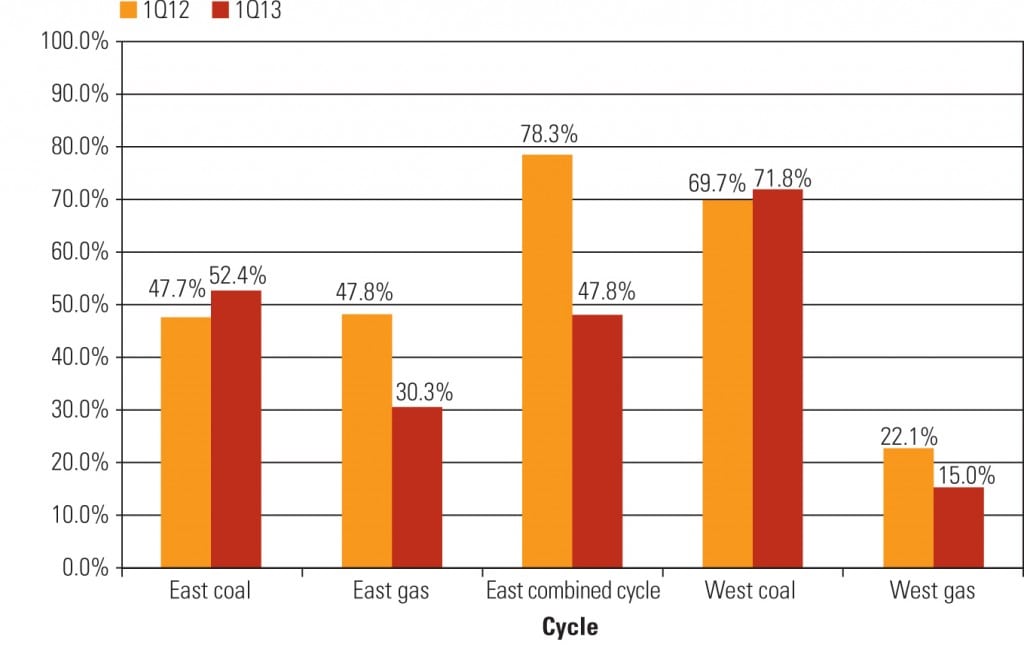

McCullough elaborated on the problems with the PJM forward (2016) market, which is hurting both AEP and FirstEnergy. “We haven’t lacked success in bidding” into the PJM capacity market, he said. But there are insufficient profits he claimed, pointing to PJM’s generous payments for customer demand response, driven by Federal Energy Regulatory Commission (FERC) rules giving demand response the same value as generating capacity.

“The problem is getting to appropriate values,” McCullough said. “When you treat demand response the same as steel in the ground, you’re going to have difficulty maintaining reliability.” He added, “It is really, really important to recognize the difference between capacity and energy. Look at Germany. Before the feed-in tariff, Germany had 100 GW supplying a load of 80 GW. Since then, the country has added 70 GW of renewables but only retired 10 GW of dispatchable generation.”

Wholesale regional markets such as PJM, said McCullough, “Need to realize that their capacity markets do not appropriately value existing generation. And with low capacity market signals, you are not going to attract new capacity. Companies will not choose to invest and take the risk that they won’t recover costs.”

Boosting AEP’s position, the U.S. Court of Appeals for the D.C. Circuit last year rejected FERC’s demand response regime. The court not only took issue with the commission’s Order 745, which deemed customer demand response worthy of the same price as physical generating capacity, but it also rejected the FERC rule in its entirety. The court told FERC to start over from scratch. The Obama administration has approved a FERC request to challenge the appeals court in the U.S. Supreme Court.

In the wake of the court order, PJM has come up with an outline of a plan for restructuring its demand response and capacity market rules. McCullough told POWER that the PJM plan, “if done right, could work. It looks like it is headed in the right direction.”

A Coal Technology Leader

AEP has a reputation not only for fielding an enormous fleet of coal-fired plants; it also has long won kudos for its engineering prowess in constructing and managing the coal-fired units. An illustration: In the late 1980s, AEP led a project to convert a failed nuclear construction project in Ohio, the Zimmer plant, into a successful coal-fired unit, an astonishing and one-of-a-kind engineering feat.

AEP’s 1,300-MW Mountaineer plant in West Virginia was an engineering marvel when it was built in 1980. In 2009, AEP and Bechtel developed a pilot project to capture and bury carbon dioxide from Mountaineer’s stack gases (Figure 1). While the project was a technical success, in 2011, The New York Times reported, the company abandoned the project because “Congressional inaction on climate change diminished the incentives that had spurred AEP to take the leap.”

|

| 1. AEP’s Mountaineer Plant. Though a carbon capture and sequestration pilot project at this West Virginia plant was a success, political action on climate change policies necessary to make continuing the work justifiable did not materialize quickly enough. Courtesy: AEP |

Still Solid, For Now

McCullough’s 34-year career at AEP tracks the company’s modern history closely, particularly its success with coal generation. Armed with a newly minted mechanical engineering degree, McCullough joined AEP in 1981 in junior management positions at the Tanners Creek coal-fired plant in Indiana, rising to operation superintendent in 1994. (Tanners Creek is scheduled to close as part of a deal with air regulators.) He then was assistant plant manager at the 2,900-MW John E. Amos plant in West Virginia, the AEP system’s largest, until 1995, when he was awarded a series of high-level, companywide management jobs, mostly related to coal-fired capacity. McCullough was named executive vice president for generation in 2010.

McCullough has lived the successful coal-fired past at AEP and has a grip on the present challenges. How does he see the generating future for the Columbus, Ohio, electricity giant?

“In the long term—20 years—there’s not a valid option for anything but gas,” McCullough told POWER. “Regulations on nuclear and coal make it difficult to put the company at that much risk.”

What about demand-side resources, distributed generation, and renewables? “Those resources make it more difficult to forecast load and make it hard to build something big, so you will see smaller incremental moves. Renewables are getting cheaper and better, especially solar. And then we will see how storage shapes up, although it’s a long way from being competitive now.”

Addressing financial analysts last fall, AEP CEO Akins said the company’s strategy, first laid out in 2013, “serves to mitigate the impacts of the, for lack of a better description, growing pains dealing with the negative circumstances of the 2016 PJM capacity auction and Ohio deregulation-induced financial impacts.”

AEP says it plans to invest “at least $4.8 billion” in transmission over the next three years “through AEP Transmission Holding Co. and AEP’s regulated utility operating companies.” As a result of those moves, Akins said, AEP remains well-positioned financially for the period up to 2016, as the company plans to maintain its dividend payout, among the highest in the industry at 3.7%. The company has paid a dividend for 418 consecutive quarters.

In a press release, AEP said the company “has a strong balance sheet and a stable credit outlook. The company’s capital plan is supported by cash flows and financial discipline without an anticipated need for equity financing beyond the company’s existing dividend reinvestment plan and employees’ purchases of stock through the 401k plans.”

It appears that AEP’s strategy is to build on its strength in transmission in order to hedge against the challenges to its generating system, which was once the backbone of the company. At the same time, the company wants to keep its already low rates under control, and try to adjust to the problems presented by wholesale capacity markets, particularly in PJM, which are also in transition.

At the end, says McCullough, in the classic claim of business people everywhere, “At AEP, our interests are aligned with our customers. What makes them happy, makes up happy.” No doubt, low electric rates make AEP’s customers happy. Whether the company’s generation transition can produce that result and keep customers happy remains a key, unanswered question. ■

—Kennedy Maize is a POWER contributing editor.