Electric utilities have a significant opportunity to create long‑term value by building new clean energy infrastructure—an approach Warren Buffett’s Berkshire Hathaway utilities have followed quietly but effectively for decades. Xcel Energy calls its version of this strategy “Steel for Fuel.”

Our recent analysis of multiple Integrated Resource Plans (IRPs) asks a simple question: have other companies identified this opportunity and are they actively planning to take advantage of it?

COMMENTARY

For most integrated electric utility companies, resource plans are key to identifying the electricity system’s needs and determining the optimal combination of generation and demand-side options to meet those needs reliably and affordably. IRPs determine what gets built by informing subsequent bidding and approval processes.

This matters to shareholders because when regulated utilities build new infrastructure, they are allowed to earn a return on that investment. State regulators typically approve a return on equity (ROE) of 9 to 11%. However, utilities are relatively low-risk companies, so financial models suggest their true cost of equity capital is closer to 7–8%. That means every time a utility builds a long‑lived asset, they actually end up earning more than it costs to finance—creating steady, predictable cash flow for investors for decades and bolstering shareholder value.

Renewables, energy storage, and fossil plants play different roles in the system through the year. Companies can build renewables mainly for low-cost energy, with a combination of duration-limited storage and long-duration gas plants to meet seasonal peak capacity needs. The sum of gigawatts and resulting capex adds up to more than just building gas plants alone and running them year-round. Rather than adding operating costs (which are recovered at cost only), building renewables and energy storage converts future fuel costs into capital costs which create shareholder value.

This shows how clean energy infrastructure can be a win-win situation for customers as well as investors. Investing in these assets can be very beneficial for customers, especially when costs are measured over the full life of the assets. Making the right decisions for customers is good business practice.

Building new clean energy resources like renewables, battery storage, and nuclear directly determines how often fossil fuel plants need to be dispatched and the resulting carbon dioxide emissions. That’s relevant for globally diversified investors’ portfolios that are already exposed to the physical effects of climate change.

In analyzing or engaging with companies, shareholders should take a closer look at the details of IRPs. These plans contain important signals about if and how a company plans to capitalize on the clean energy opportunity. Admittedly, IRPs rely on complex power system models, but fortunately, a very simple concept applies: robust inputs lead to robust outcomes. Alternatively, garbage in leads to garbage out.

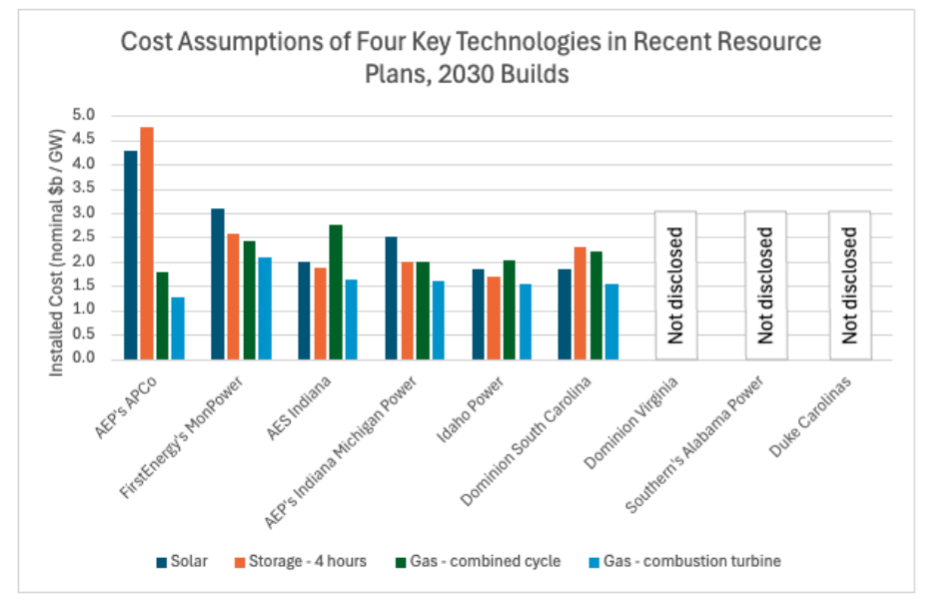

One of the most important pieces of information to take into account is the cost assumptions used to determine what resources to build. Surprisingly, companies are using a lot of discretion with respect to how much it costs to build different resources. The chart below summarizes the cost assumptions used in several notable plans filed in 2025 for a 2030 build.

(Note: Companies disclose in a variety of formats, and we have converted into nominal dollars and total installed costs where necessary for comparability.)

The fact that Duke Carolinas and Dominion Virginia did not disclose their cost assumptions in 2025 is surprising, since they did in their prior plans, and Duke’s and Dominion’s other subsidiaries are disclosing those costs. Alabama Power’s lack of transparency is unsurprising since Southern takes the same approach with its other subsidiaries, Georgia Power and Mississippi Power. Fortunately, most companies are still transparent, but the list of companies not disclosing this information to the public and investors is growing.

AEP’s Appalachian Power Co’s assumptions stand out as being wildly inflated for clean energy, and low for new gas builds. The company states these costs are “informed from the 2024 Renewable RFP,” but we wonder if AEP’s clean energy cost assumptions are distorted by unusually high, nonserious bids from developers.

With all the federal policy changes, including tariff uncertainty, and other inflationary pressures in the construction sector, determining appropriate build cost assumptions is getting harder. Public sources like NREL’s Annual Technology Baseline are lagged, and up-to-date estimates are paywalled. As a result, comparisons across peers are still worthwhile, if one pays close attention to when a plan is filed.

Importantly, inflation has not just been limited to solar, wind, or energy storage. Cost increases have actually impacted gas plant builds more, with estimated costs of $2.8 billion per GW to build a combined-cycle plant.

Given these discrepancies and their potential impact on shareholders and consumers, the first step is for utilities to disclose these cost assumptions in their IRPs. Ideally, these disclosures should show the assumptions for the full planning horizon and not just a single year. Utilities should also model into their assessment moderate cost declines for solar and energy storage, since installation becomes more efficient and supply chains mature. IRPs are forward looking, often with a horizon of two decades, so it does not make sense just to use today’s costs.

This transparency is essential for investors. Cost assumptions signal whether companies are fully pursuing this value creation opportunity while reflecting state and federal policies. Better assumptions also give the power system models the flexibility to identify the lowest cost, most reliable resource mix–benefitting companies, investors, and customers.

—Colette Lamontage is the senior director of electric power, and Luke Angus is the director of utilities, at Ceres, a nonprofit advocacy organization working to accelerate the transition to a cleaner, more just, and resilient economy.