Risk is inherent in all businesses, but power plants face unique perils that require the right protection. Property and casualty insurance may not be enough; equipment breakdown, business interruption, weather risk transfer, and cyber coverage are just a few examples of insurance that may also be worth considering. The right coverage could mean the difference between success and failure.

Insuring a power plant is quite a bit different from insuring a car or truck. Sure, your Allstate or State Farm representative may check your car for pre-existing damage before initiating coverage, but in my experience, no agent has ever performed routine inspections of my vehicles or offered engineered solutions to make them safer or more reliable. In fact, I suspect my auto insurance agent knows much less about automobiles than I do. For the most part, if a vehicle is legally registered, the insurer will write you a policy and gladly take your money.

Insurance companies that specialize in power plant policies are much more proactive. They often have a unique understanding of the systems and components installed in facilities, and they recognize the perils faced by the technology being used. Most of the power plant insurance representatives who visit sites are not just salespeople, but often full-fledged engineers with the knowledge and experience to make valuable recommendations. They visit many different facilities and have a database full of claim information, allowing them to share best practices and catch little things that could lead to big problems.

A History of Risk Reduction

The theory behind the process lies in the belief that most losses can be prevented. If appropriate actions are taken to mitigate hazards and reduce risk, the likelihood of a claim decreases, and that’s good for everyone.

It’s not a new idea. A textile mill owner named Zachariah Allen, for example, formed FM Global (originally known as the Factory Mutual System [Ed. correction made 3/14/17]), back in 1835. In an effort to reduce the risk of fire and increase his mill’s resiliency, Allen made various property improvements. However, when he asked his property insurance company to decrease his premiums to match the reduced risk, it refused. So Allen recruited other mill owners who shared his philosophy, and they created their own mutual insurance company. Today, more than a third of Fortune 1000 companies partner with FM Global for at least a portion of their insurance needs.

“We’re a property insurance company. We don’t do the casualty, the liability, or many of the other lines of insurance that are out there,” Mark F. McAdams, high-hazard occupancy specialist for FM Global, told POWER during an interview. “We do one thing and we do it right. We address property exposures, and we help our clients reduce their exposure to loss—reduce their overall cost of risk—by sending engineers out to the facilities and focusing on practical solutions to reduce the chance of loss as well as the potential severity of the loss.”

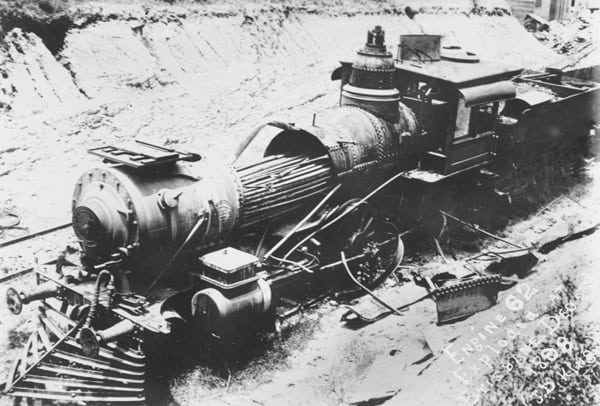

There are other insurance companies with similar philosophies. Hartford Steam Boiler (HSB)—a 150-year-old business—has a history that is just as interesting as FM Global’s. When HSB was founded, the light bulb had not yet been invented, but boilers were everywhere nonetheless. Steam was used to power boats, locomotives, and industrial machines. But the boilers back then weren’t as safe and reliable as they are today; explosions were commonplace. In the 1850s, a boiler explosion occurred about once every four days, according to HSB.

Although many boiler owners simply considered explosions—and the damage and loss of life that resulted—as a cost of doing business, a group of Connecticut businessmen didn’t think explosions were unavoidable. The men formed a polytechnic club to find a solution and what transpired was a boiler inspection company that offered insurance as an incentive. Today, HSB employs more than 1,200 engineers, inspectors, and technical personnel around the globe.

The benefits provided by companies like FM Global and HSB are quantifiable. McAdams said FM Global has documented a reduction in the number of losses—and the severity of the losses—the longer a facility is insured by the company and receives its engineering services.

“As a mutual insurance company, our owners are our policyholders [Ed. correction made 3/14/17], so we’ve got a built-in bias to do what we can to take care of our clients,” said McAdams. “With a philosophical foundation that most large losses can be avoided—a majority of loss can be avoided—we utilize our engineering service to help them prevent the potential and reduce the severity of the potential losses that are out there.”

Insurance Changes with the Times

Exploding boilers are much less likely today than they were in the 19th century (Figure 1) due at least in part to the work of companies like FM Global and HSB, but now there are new risks that were never even dreamed of back in those days. There are also new companies serving the insurance needs of power plants. The increase in providers with still solid track records has helped to keep policy costs in check.

Allianz Global Corporate and Specialty (AGCS)—a German-based company—offers one example. With more than 100 years of technical expertise in the business, Allianz began investing heavily in the U.S. power segment in 2003. Similar to FM Global and HSB, AGCS offers property coverage (including business interruption) and builder’s risk policies (including delay in startup coverage). It, too, has a loss control program, which incorporates visits to facilities by qualified engineers and the creation of loss control reports with recommendations to reduce risks.

“We as insurers have an overview of the whole industry because we are insuring multiple clients across the whole country and all classes of power assets, so our engineers have access to the best practices in the markets,” said Honorio Campos, engineering team leader for AGCS Americas. “They contribute by sharing those best practices as recommendations.”

Some common items addressed by AGCS engineers in their reports include fire protection improvements (Figure 2), plant monitoring upgrades, and recommendations to protect against natural hazards. For example, if a plant is located in a flood exposure area, AGCS engineers can use their expertise to propose solutions to reduce the flood risk.

Campos suggested that whenever a natural disaster strikes, clients rest easier knowing they have sound insurance protection. “Hurricane Sandy was an event that affected some of our clients. We have had clients impacted by tornados or most recently by wildfires on the West coast. Those are all events where clients appreciated having AGCS protection,” he said.

Weighing the benefits provided by the various property insurers is certainly important, but there are also other policy options that must be considered. According to David Barclay, senior vice president with the property and casualty insurer Chubb, property and liability policies form the heart of an insurance program, but coverage must still be customized depending on the insured’s particular exposures.

“Chubb can provide many insurance products for a power producer including property, business income, general liability, automobile, workers compensation, environmental, umbrella, and many others. Mid-sized independent power producers may find having one insurance carrier is most efficient,” Barclay told POWER. “It is important to look for an insurance carrier that can grow with them as they build more projects,” he said.

Barclay suggested power producers should consider broad business income coverage that includes “extra expense.” One argument for such a feature is that it allows the insured to use extra expense dollars to expedite replacement equipment when an event interrupts power production. It can also be used to purchase replacement power from third parties following an incident, thus reducing losses and helping companies more easily meet their customers’ needs.

Plant owners must consider all sources of business income too. Barclay noted that many power generation operations derive revenue from capacity payments and tax incentives. Losses of those revenue sources should be contemplated when insurance policies are designed. Many large power companies can accept higher deductibles and purchase higher limits because of their size, but mid-sized independent power producers probably shouldn’t assume as much risk, so smaller deductibles are often more appropriate for them.

Other exposure that can often be overlooked is the risk associated with international operations and activities. Barclay said it’s important for companies to have the same protection in other countries as they do at home. Environmental coverage is perhaps a less well-known option that may be worth considering for many power companies. Those policies alleviate some of the risk associated with potential damage to land, water, and other natural resources.

Lloyd’s, a London-based company that has been providing specialty insurance since the 17th century, offers some of the most unique policy options. The company says it has more than 60 lines of insurance and reinsurance from which it can develop tailor-made policies for nearly any customer. It covers such things as accident and health; crime; contingency; cyber; directors and officers; employers liability; energy; engineering; extended warranty; legal expenses; medical expenses; general liability; nuclear; political risks, credit, and financial guarantees; power generation; property; and terrorism.

Renewable Power Project Insurance

Often, people think of renewable energy as a recent phenomenon, but many renewable projects have been around for more than three decades. One company that specializes in renewable energy insurance is GCube. The insurer focuses solely on renewable energy projects—mainly wind and solar. Sam Walsh, senior vice president with GCube, noted that 2017 is the company’s 25th year of offering its WindPro product.

“We’re backed primarily by Lloyd’s of London paper, as well as Swiss Re, and that allows us to write pretty much in any country that they have the legal capability to write within, so that is the vast majority of the world,” Walsh told POWER.

GCube gets between 40% and 45% of its business from U.S. projects, but it also has a large presence in Europe, South Africa, and Australia. Walsh said its business is growing in the Middle East and in a few countries in Asia (he specifically mentioned Thailand). The company’s goal is to offer as many insurance options as possible for the full lifecycle of a renewable energy project.

For a typical wind power project, for example, a development policy will be the first step. Usually, meteorological data will need to be gathered from a site to gauge the viability of a location. That doesn’t involve a lot of equipment, and potential losses are fairly small, so the development policy offers relatively inexpensive coverage to get through the process. Companies are also wise to have a general liability policy during the development stage to protect against leased-land exposure, among other things.

Once a project comes to fruition, construction all-risk and liability policies are the norm. Many things can go wrong while construction is in progress, so lenders generally have very specific insurance requirements that owners must meet. Most wind farms have a large number of turbines that make up the project. Naturally, they don’t all get done at the exact same time, so there is usually a clause in the policy that allows continued coverage of operational turbines on the construction side, until the entire project is complete.

“The goal is to be as seamless and cohesive as possible, so GCube can be a one-stop shop for the insured,” said Walsh.

Weather Risk Transfer

One of the complaints often railed against renewable energy is that it doesn’t generate power when the sun doesn’t shine or the wind doesn’t blow (or the rain doesn’t fall, which has affected some hydropower facilities). Weather variability poses a problem not only for the grid and those charged with keeping the lights on, but also for renewable energy owners. And it’s a risk that shouldn’t be overlooked.

“In 2015, there were large swathes of the U.S. that had much lower wind speeds because of El Niño,” said Walsh. As a result, a lot of wind projects throughout the southwestern U.S. under-produced by as much as 40%. For small- and mid-sized independent power producers, a lack of production such as that can be a massive hit to the bottom line.

To provide some assurance of revenue, owners have been searching for ways to transfer that weather risk. One product that GCube offers to address the problem is a weather hedge mechanism for the wind and hydroelectric energy markets. It enables buyers to guarantee a floor on financial performance and unlock additional value for projects and their stakeholders.

“It differs a little bit from insurance in the sense that it’s more of a financial product versus simply an insurance product,” Walsh said. “But I think a lot of project owners are looking to weigh whether that’s a coverage they now want to supplement a standard property and general liability program with to make sure that they’re getting enough revenue in a given year.”

When Catastrophe Strikes

Partnering with companies that have proven track records should be high on the list of requirements when developing a project. That not only extends to insurance providers, but also to original equipment manufacturers (OEMs).

For example, many wind turbine OEMs offer a two or three year equipment warranty. The first line of recourse following a component failure is to submit a warranty claim. Catastrophic losses, such as gearbox failures or up-tower fires, can often be measured in terms of millions of dollars. Working with a bankable OEM that has a record of standing behind their product can save a lot of headaches.

Having comprehensive insurance coverage should be next on the list of important project musts. Generally speaking, if a broker offers three policies for an owner to choose from and one is significantly cheaper than the other two, that should raise a red flag. The cheaper policy may be excluding something that could leave the insured with a significant loss on its hands.

“In the event that the manufacturer’s warranty does not respond, our policy steps out to make sure that the insured is made whole,” Walsh said. He also noted that even if the manufacturer’s warranty does pick up the physical damage loss, there could still be lost revenue resulting from business interruption. “Our policy would step in and pay those out,” he said.

Although many projects are planned with 20-year lifespans, history has shown that wind turbines on average are not lasting that long before having breakdowns (Figure 3), such as blade issues or gearbox problems. The costs to fix those failures can be quite significant. Cranes are often required, which adds to the expense.

If fleet-wide defects transpire, owners will appreciate having a reputable OEM. The reason: Most insurance policies have serious-loss clauses and/or defect exclusions. What that means is coverage tapers off at some point.

“If you were to pick a manufacturer that ultimately goes out of business and five years down the line their equipment starts to fail on a fleet-wide basis, there’s going to be an issue,” Walsh said. “Insurance will provide coverage for the first set of losses, but after that, the exclusions will start to step in.”

Solar Power Project Hazards

While wind is a necessity for successful wind power projects, it can be a real hazard for solar projects. Once installed, solar panels are generally designed to withstand relatively high winds, but it is nearly impossible to fully protect a site against natural disasters, such as hurricanes and tornados (Figure 4). Last year, Hurricane Matthew resulted in multimillion-dollar losses to power projects, and Superstorm Sandy, as noted previously, was a particularly devastating storm.

It’s not always the wind that causes the most damage, however; storm surges can be even more destructive. Salt water is very corrosive and can create a lot of problems. Walsh suggested that projects are particularly vulnerable while under construction. “They tend to perform better once they’re operational versus during the construction phase when not everything may be tied down or there’s loose equipment on-site,” he said. “Stuff can be picked up by high winds and cause a fair amount of damage.”

Solar projects also seem to be more susceptible to contractor errors and theft. Walsh said that most of the projects GCube has underwritten in the U.S. haven’t experienced huge losses, but the company’s European counterparts haven’t been as lucky. Not only are thieves stealing solar panels, but they’re also taking copper wiring from sites. “Site security and the steps that are taken to mitigate those types of losses are very important,” he said.

Although solar projects don’t have the large up-tower problems and the associated crane-type losses that wind projects encounter, equipment does break down. A couple of the more common failures are to inverters and transformers, which can lead to large financial losses. Some sites have been designed with all power being offloaded through a single-point transformer, so the loss of one of those can take an entire site down. GCube partners with a third-party engineering service to look for that type of situation and to develop a plan, when necessary, to mitigate the risk.

Cyber Protection

As power plants have become more connected with digital technology, the risk of cyberattacks has increased. Insurance companies have come to understand the risk, however, and many have developed policies to protect customers against losses caused by hackers. FM Global is one that began offering cyber policies as far back as 2001, and McAdams said the company recently expanded its coverage.

FM Global says its all-risk policy has no cyber exclusions for physical loss or damage. Rather, it covers common cyber loss events including damage to data, programs, or software created by viruses or malware; computer network service interruption caused by malicious cyber activity; and third-party data services interruption—cloud outages—leading to business interruption or property damage.

“If [hackers] were to get into the control systems, they could potentially do physical damage to your generators and other property. That’s obviously a big piece of that exposure,” McAdams said.

In the end, however, AGCS’s Campos suggested that the most important thing is to have a good broker. Finding a trustworthy agent to help assess the coverage that is needed and customize an insurance solution to mitigate the exposure is invaluable. Walsh agreed. He said nearly all of GCube’s clients work with a broker who will evaluate the coverage for them and make sure the policy is comprehensive and appropriate. ■

—Aaron Larson is POWER’s executive editor.