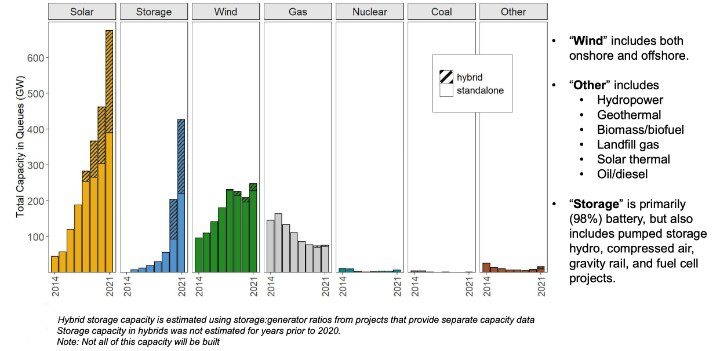

A study conducted by the Lawrence Berkeley National Laboratory (Berkeley Lab) shows more than 1.1 TW of solar and energy storage capacity were in the U.S. power grid’s interconnection queue at the end of 2021. Notably, that total is more than the currently existing capacity in the U.S. power fleet.

Additionally, Berkeley Lab researchers found that 247 GW of wind power and 75 GW of gas power capacity were also in the queue, along with other miscellaneous projects, bringing the total of proposed projects seeking connection to the U.S. grid to more than 1.4 TW (Figure 1). The total cost for these proposed projects is estimated to be more than $2 trillion.

“The sheer volume of clean energy capacity in the queues is remarkable,” Joseph Rand, a senior scientific engineering associate at Berkeley Lab, said in a statement releasing the study’s findings. “It suggests that a huge transition is underway, with solar and storage taking a lead role.”

The truth is, however, most of the projects in the queue will never be built. History shows that plans often end up in the garbage. For example, less than 23% of projects requested from 2000–2016 have reached commercial operation today. About 72% of projects requested over that timeframe were ultimately withdrawn. Still, if 23% of the projects in the current queue are completed, that would total 322 GW, which is more than one and a half times the capacity of all utility-scale coal-fired power plants operating in the U.S. today.

The interconnection queue is basically a list of proposed projects compiled by utilities and regional grid operators (ISOs and RTOs). These entities generally require projects seeking to connect to the grid to undergo a system impact study before they can be built. This process establishes what new transmission upgrades may be needed before a project can connect to the system, and then estimates and assigns the costs of that equipment.

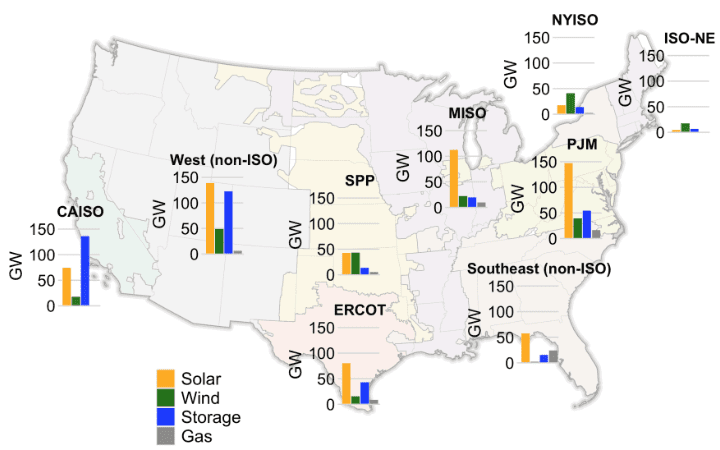

As part of its study, Berkeley Lab compiled and analyzed data from the seven organized electricity markets in the U.S. and 35 additional utilities outside of those regions, which collectively represent more than 85% of all U.S. electricity load. The researchers found that proposed capacity is widely distributed across the U.S. (Figure 2). Almost all regions showed substantial proposed solar capacity in the queue. Energy storage proposals were mainly focused in CAISO and other non-ISO parts of the Western U.S., but PJM also had significant energy storage capacity proposals.

Another notable finding from the study is that projects are sitting in the queue longer than they used to. For five regions where data were available—CAISO, ERCOT, NYISO, PJM, and one utility (APS)—the time projects spent in queues before being built increased from about 2.1 years for projects built in the 2000–2010 time period up to about 3.7 years for those built in 2011–2021.

The researchers also noted that interest in hybrid plants has increased. At the end of 2021, 42% of solar projects in the queue (285 GW) were proposed as hybrids, as were 8% of wind projects (17 GW). Those percentages were up markedly from 2020, when proposed hybrid projects accounted for 34% and 6% of solar and wind proposals, respectively. Solar + storage is by far the most common hybrid configuration proposed.

—Aaron Larson is POWER’s executive editor (@AaronL_Power, @POWERmagazine).