U.S. Microgrid Market Development

Microgrids have been around for decades, but today, more potential customers, owners, technologies, and vendors than ever are part of the market. Increased interest in this special grid resource means there’s more competition, which is generally a good thing, but there are also new challenges.

“You have to have some serious staying power” to be in the microgrids market, observed David B. Chiesa, senior director, global business development at S&C Electric Co.

Chiesa, who served as summit chair for the Infocast Microgrid Markets Summit East (Microgrids Summit) in mid-March, noted that projections for the sector have been too optimistic. We are still seeing “pilots,” and new microgrids are all one-offs, where the pieces are still being fitted together like a jigsaw puzzle. Much of the difficulty, he suggested, is that you can’t be an expert in just one area to be successful with microgrid projects, because they involve generation, storage, controls, and maintenance.

Microgrids Old and New

Microgrids have been around for many decades, predominently on educational, medical, and corporate campuses (see sidebar, “Different Microgrids for Different Purposes”). The motive for developing a campus microgrid in the past was usually some combination of lowering energy costs with onsite combined heat and power (CHP), providing reliable power to critical loads, and, less often, enabling “island” operation (disconnecting from the larger distribution grid) during times of grid service disruption, although some were originally designed to operate disconnected from the grid most of the time.

|

Different Microgrids for Different Purposes In a February interview with POWER at IHS CERAWeek, ABB Chief Technology Officer Bazmi Husain called microgrids “one of the most fundamental changes” in the power industry. Different geographies will use different fuels and technologies in their microgrids, he said, just as some will be isolated and others will be connected to larger grids (though still capable of islanding). Microgrids, Husain said, are a great solution “to quickly reach those who don’t have access to electricity today.” That includes India, where “upward of three million people do not have access to electricity.” The business case is strongest in developed and developing countries for campuses or hospitals, which have a need for high reliability, he said. |

More recently, interest in new and different configurations of microgrids has come in basically two flavors.

For geographically islanded customers—whether on an actual island or in a remote region like Alaska (see sidebar “Alaska Goes Big for Microgrids”)—microgrids, often with at least some renewable power to mitigate the cost of long-distance fuel delivery, can offer the most economic way to provide electricity service. Elsewhere, military installations and civilian communities (especially those that have experienced lengthy outages as a result of intense storms) have been the driving forces behind studies, pilots, and deployments of microgrids that combine newer forms of energy generation, storage, and delivery.

|

Alaska Goes Big for Microgrids At IHS CERAWeek in February, Senator Lisa Murkowski (R-Alaska) commented, “Microgrids are going to be my state’s future.” They’re also its present. Unlike the lower 48, Alaska has no “main” grid and doesn’t interconnect with other large grids (and opportunities for such interconnection are very limited). It’s also different from Hawaii because of its smaller population spread over a far larger geography, so microgrids make a lot of sense. In December 2014, Navigant Research declared that Alaska led the world in microgrid deployment, with between 200 and 250 “permanently islanded” microgrids—ranging from 30 kW to 100 MW in size and with a total capacity of over 800 MW. Some have operated for more than 50 years. |

The diversity of goals, components, and configurations of newer microgrid concepts means that microgrid definitions vary. Many proponents would say that a microgrid must be able to operate both connected to the larger grid and in islanded mode; others argue islanded operation is not essential. But anyone involved in developing microgrids would agree that, whatever combination of loads and distributed energy resources (DERs) are included, they must be in communication with each other and be interconnected by way of a dedicated control system that can operate all the elements as a discrete entity.

The necessity of independent control means that early efforts by U.S. Department of Defense (DOD) branches at a variety of facilities have not been actual microgrids. Although the DOD was an early and enthusiastic adopter of onsite renewable generation and storage to support energy supply resiliency and renewables targets, the controls component was not always present; generation and distribution assets were either owned by the utility or unable to island from the utility grid. That’s not necessarily a bad thing; it depends on the microgrid’s goals.

Speaking of resiliency, one Microgrid Summit attendee challenged the use of that term. What was really being discussed was reliability, he implied. Reliability is a familiar metric for the electricity sector, whereas resiliency is a newer term that has been used by utilities, consultants, and governments. Microgrids may provide resiliency for facilities, processes, and communities by providing a more- reliable power source—at least for critical loads—during times of grid stress when the transmission and/or distribution grid is down if they switch to islanded operation. They can provide that reliability because, in addition to providing onsite generation, they typically underground any distribution lines that run beyond a single building. They may also enhance distribution grid resiliency by providing DER at critical feeder locations.

Microgrids Are Part of the Big Grid

The addition of sometimes complex grid resources “behind the meter” raises a variety of concerns. On the distribution side, many operators are used to dealing with large, self-generating customers and with demand response programs. But adding microgrids to other DERs (which are proliferating in some places) raises the question of how to upgrade a distribution grid that optimizes “going from a quartet to multiple orchestras,” as Christopher B. Berendt, partner with Drinker Biddle & Reath put it.

Nevertheless, as several speakers at the Microgrid Summit observed, microgrids are becoming an integral part of the larger grid. In many ways, they provide more stability and predictability than other isolated DERs, especially rooftop solar.

Microgrids are becoming an “alternative service delivery model,” said San Diego Gas & Electric’s (SDG&E’s) Neal Bartek, distributed energy resources manager. Jim Reilly of Reilly Associates, agreed, observing that microgrids are becoming more a part of the distribution system, not just something used in emergencies.

That shift has been enabled at least in part by Federal Energy Regulatory Commission Order 745, which was upheld earlier this year by the U.S. Supreme Court. Order 745 enables grid operators to include demand response resources in organized wholesale markets, where they are eligible for payments.

For example, as Esrick O. McCartha Sr., senior business solutions analyst at PJM Interconnection, explained, microgrids can go far beyond playing a grid-balancing role through demand response. He said PJM is interested in microgrids from the perspectives of load forecasting (though its 15-year look-ahead has not yet included microgrids), visibility, and planning. PJM welcomes microgrids, he said, though if they aren’t connected to PJM, they aren’t visible or dispatchable.

If you have all the microgrid components, you can participate behind the meter (as load) as a resource for generation by reducing load. But (at least in PJM), if you have DER such as behind-the-meter generation or battery storage, then you also can inject power into the system in front of the meter—as supply. Doing so, McCartha told POWER in a post-session interview, requires an interconnection agreement, which is available to anyone who pays for it. To date, however, although PJM does have battery energy storage in front of the meter as well as demand response microgrid resources (including Princeton University’s), it doesn’t have a connected microgrid that is both behind and in front of the meter.

The Role of States in Microgrid Development

As distributed energy generation and storage markets continue to grow while costs drop, there’s more interest in exploring microgrid options from both commercial and industrial and municipal entities. But developing a microgrid beyond a single building can raise questions of rights of way, interconnection rules, rates, and other regulatory issues (see sidebar “Who Benefits and Who Pays?”). That’s why state utility regulators are seen as key stakeholders in microgrid market development.

|

Who Benefits and Who Pays? The question of who benefits from microgrid development raises obvious questions about who pays for it. In the case of building-only or campus-only grids, answering those questions is relatively straightforward. But in the case of “community microgrids”—a newer concept—the answers are far from clear and will require careful analysis and, likely, policy updates. For example, should the costs of a microgrid that supports selected “critical services” in a community, such as a fire station or wastewater treatment plant, be spread across all customer classes in an entire service territory? Aside from the financing aspect, who benefits can become complicated for other reasons. Allison Archambault, president of Earthspark International, noted at the March Microgrids Summit that one difficulty for microgrid development is that the different value streams may accrue to different stakeholders. Consider a community microgrid that encompasses a combined heat and power (CHP) plant, some solar photovoltaic (PV) capacity, battery storage, and electric vehicle (EV) charging stations. The municipal government might own the PV and EV chargers, but a private entity (a small college) might own the CHP plant, and an out-of-state third party might own the battery. In the case of an extended outage, assuming the microgrid can island, the college could presumably shelter and provide some essential services to more than just its regular campus users. In this scenario, the microgrid provides community resilience benefits that exceed the ongoing economic benefits derived from the CHP plant and battery storage—assets that may be tied to a transmission operator that pays for demand response and ancillary services. Konterra Realty has experienced the split–value stream problem firsthand. Two years ago, Richard McCoy, the development company’s executive vice president, spoke at the same microgrid event, excited about hosting a 400-kW microgrid at a Konterra corporate facility that included PV, EV charging, and a microgrid controller. But this year he noted that the goals of participating in demand response and peak shaving “have been difficult to achieve,” largely because of ownership changes affecting the microgrid portion of the project, which is owned by a third party. Konterra owns the PV generation and shares ownership of the inverter. |

Microgrid Summit attendees heard from regulators and those who interact with them in several states, including Arizona, California, Connecticut, Maryland, New York, and the District of Columbia. All of the states represented are interested in developing microgrids and are seeing a lot of interest in them from the public. (Though one regulator mentioned that some environmental groups have unrealistic expectations for microgrids—something they have in common with some utility executives, as was mentioned in a different session.)

Jamie Ormond, advisor to California Commissioner Catherine J.K. Sandoval, underscored the importance of engineers, vendors, and other interested parties participating as interveners in dockets before utility commissions—like the microgrid interconnection docket currently before the California Public Utilities Commission (CPUC)—to ensure that commissioners understand all the issues around microgrids and how the rules are established for their operation.

New York is seen as one of the leaders in microgrid market support as a result of its Reforming the Energy Vision (REV) initiative (see “New York’s Reforming the Energy Vision” in the May 2015 issue of POWER) and the $40 million New York Prize, offered by the New York State Energy Research and Development Authority (NYSERDA) to help “communities reduce costs, promote clean energy, and build reliability and resiliency into the electric grid” via microgrids.

One panel at the summit discussed progress to date in New York. Michelle Isenhouer Hanlin, energy program manager at Booz Allen Hamilton, commented that, where microgrids are concerned, REV has opened a big door, but it makes “a nebulous ask” of utilities [to increase DER and revise their business models] that operate in a very formulaic environment. More public service commission guidance is needed, she said, on how the money will flow to projects and whether projects can be rate-based.

Other challenges that REV and NYSERDA are facing include a higher-than-expected volume of applicants and program timeframe slippage. As early-stage, unique initiatives, a learning curve is to be expected, and Isenhouer Hanlin suggested that Hawaii, California, and other states learn from New York’s experience. New York wanted to “stimulate an energy market,” and “they have done that,” she said, but not every community can have a microgrid—for a variety of reasons. Still, she noted that there are other ways to participate in REV, including energy efficiency and renewable energy resources.

States may play other nontraditional roles in the microgrid market as well. Connecticut, for example, was the first state to launch a green bank to leverage public and private funds for clean energy development.

The Role of Utilities in Microgrid Development

The Microgrid Summit included panels devoted to progress in individual states as well as at DOD sites. Although the military has some special considerations for microgrids, it has to answer some of the same questions most new microgrids must answer: Who develops, owns, and operates them?

The utility may be the obvious answer in some cases, as utilities have expertise managing loads and generation. That said, the Navy has been more successful in partnerships with some utilities than others, said Monica DeAngela, director, installation energy program integration, assistant secretary of the Navy (Energy Installations and Environment). She specifically called out Groton Utilities as a good partner as well as Arizona Public Service (APS), with which the Navy is currently working on a microgrid at Marine Corps Air Station (MCAS) Yuma (Figure 1).

|

|

1. Backup for the backup. Two HH-1N “Huey” helicopters sit on the grounds outside of the Search and Rescue (SAR) hangar aboard Marine Corps Air Station (MCAS) Yuma, Ariz., Feb. 12, 2016. The MCAS Yuma SAR team hosted a conference with regional emergency services personnel to discuss tactics, techniques, and procedures. MCAS is leasing land to Arizona Public Service to develop a microgrid that will supply backup power for the installation. Source: Photo by Lance Cpl. Brendan King |

The Yuma project uses a lease model wherein the Navy leases land to APS for 30 years for development, operation, and maintenance of a 25-MW diesel generating unit, which was selected because it provides the fastest reliable startup. In November last year, an APS press release noted that the microgrid, which is the first for the utility, will supply 100% of the backup power for MCAS Yuma should there be a grid disruption. The facility was expected to be online by the end of the second quarter of 2016. DeAngela noted that the Navy is also looking at adding fuel cells and renewables to the project.

How eager a utility is to develop microgrids or partner with third-party developers depends on its specific circumstances. Most are in the very early stages of considering their role in microgrid development. The state of Illinois, for example, asked ComEd to build six microgrids to protect critical public infrastructure, and the utility has two grants to date from the U.S. Department of Energy to support that work. In California, SDG&E developed the Borrego Springs microgrid project (Figure 2) on its own initiative, initially because it saw the project as a way to study the behavior of anticipated large amounts of DERs being added to its system, and it wanted to learn how to accommodate them.

|

|

2. Backing up solar photovoltaic generation. Lithium-ion batteries are an important component of San Diego Gas & Electric’s Borrego Springs microgrid. Courtesy: SDG&E |

SDG&E is, in fact, learning from this project. Disconnecting from the grid during a summer thunderstorm enabled the microgrid to remain online and power the community of Borrego Springs. However, during a more recent disruption, the utility couldn’t operate the microgrid because of a problem with the transmission grid, and the microgrid failed to island. That experience is a reminder that microgrid operation isn’t easy.

Tom Weaver, PE, manager, distribution system planning for American Electric Power (AEP) commented that although his company doesn’t yet have a commercial microgrid, it has experience with all the parts and sees multiple benefits of microgrids, including the abilities to:

■ Provide distribution circuit–level reliability

■ Power community critical loads

■ Power customer critical loads

■ Integrate renewables

However, AEP and other utilities need to figure out who owns what parts of a microgrid, because regulated utilities can only ratebase the portion that fits with their regulatory compact.

Another potential role for utilities is “microgrid as a service,” something Duke Energy is developing.

Beginning in 2013, Duke began pitching the idea of a consortium of companies involved with a variety of grid modernization pieces, from meter manufacturers to control systems providers. Getting companies on board was challenging, because Duke’s plan was that everyone would “openly share their knowledge, products and expertise,” according to a Duke statement. Initially, only six companies joined what Duke calls the Coalition of the Willing: Echelon, S&C Electric, Alstom Grid, Verizon, Ambient Corp., and Accenture. Since then, a total of 25 companies have joined the initiative, including ABB, GE, Honeywell, Schneider Electric, Schweitzer Engineering Laboratories, and Siemens.

A related step for Duke has been moving into “green microgrids” and selling microgrids as a service to businesses as well as state and municipal agencies. It has even suggested that it might offer this service beyond the U.S. through Duke Energy International. Duke has developed a Mount Holly, N.C., microgrid test center that has been focused on interoperability issues and what it calls a “field device interoperability solution designed framework,” known as the trademarked Open Field Message Bus (OpenFMB).

One microgrid-as-a-service customer is coalition partner Schneider Electric, which announced earlier this year that it is developing a microgrid that includes solar generation and battery storage at its Andover, Mass., campus. At IHS CERAWeek in February, Andy Bennett, senior vice president, infrastructure and energy for the company’s U.S. operations, said in an interview with POWER that, instead of paying National Grid about $0.14/kWh, Schneider is “paying Duke to pick up our energy bill… and now we’re going to pay $0.085/kWh.” Duke Energy is also picking up the capital costs because “it’s a good investment for them,” he said.

Bennett anticipates that regulated utilities, especially investor-owned ones, are going to “look at taking market share out of some of their potential competitors’ territories” with microgrid-as-a-service offerings. He said his company expects to see “grid parity in a majority of the states for PV plus battery storage by 2020,” and at that point, microgrids will become more compelling.

Microgrid Business Models

Utilities may not be the only front-runners for developing, owning, and/or managing the newer non-campus types of microgrids.

In a Microgrid Summit session on Connecticut’s microgrid grant and loan program, Dr. Sudipta Lahiri, team lead–microgrids, DER for DNV GL-Energy, commented that “the time is ripe for a microgrid service provider”—someone who brings the vendors, engineer/procure/construct firm, finance, and all the other pieces together and then sells the service (rather than the physical microgrid assets).

When POWER asked Dr. Lahiri what type of entity that might be—utility or non-utility—he responded, “It can be a startup.” He suggested it was possible that someone less entrenched than a utility, yet someone with deep financing, would come in and get stakeholder agreements, do performance validations, and develop the project. The end user shouldn’t have to worry about any element, he said.

Session moderator Steve Pullins, vice president, microgrid solutions for Hitachi Social Innovation Business-Americas, added that his company is one of those service providers, especially for campus customers. Other vendor companies, especially control system providers, also have played the role of system integrator to one degree or another.

The service provider, Dr. Lahiri clarified, could be independent from the technology provider.

During one of the event breaks, an industry participant suggested to POWER that Lockheed Martin could potentially be positioned as a one-stop shop to integrate and develop entire projects, but “nobody has all the pieces,” he said. One reason is that microgrids might include any of the following generation types—diesel, gas, fuel cell, PV—all of which have different suppliers and inverters.

Whether utilities, technology providers, or independent third-party upstarts are best suited to create a reliable recipe for microgrid development remains an open question.

Lessons Learned to Date

Although new microgrid configurations, technologies, and business models are still evolving, some lessons have been learned in the past few years.

Design Holistically. In contrast to pilot projects or “science projects” to test the operation of a particular component, microgrids work best when all components, benefits, and stakeholders are considered from the start. Just wanting to add renewable generation to a building project, for example, isn’t sufficient to ensure success.

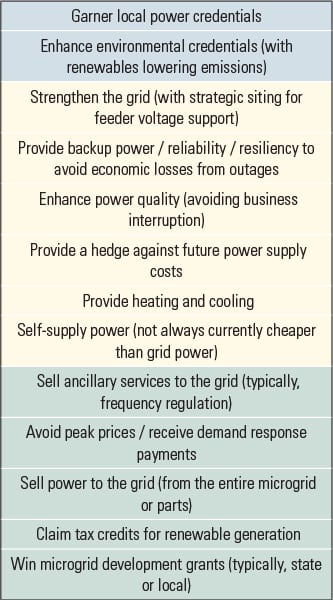

Optimize Value. A related lesson is to wring as much value from a project as possible from the start—even though some future benefits may accrue that cannot be anticipated (see sidebar “Stacking Microgrid Benefits”). For example, use economies of scale and diversity, as far as possible, to aggregate multiple loads with complementary demand profiles.

|

Stacking Microgrid Benefits Microgrid developers and financers often talk about the importance of “pancaking” value streams to make a project financially viable. Just providing backup power, for example, is unlikely to make a project pencil out. More recently, “resiliency” for a customer or community—supported by the electricity reliability provided by a microgrid—has become a primary motive for considering microgrid development. The problem is that, while few would argue against resiliency, there’s currently no way to make it a bankable benefit for financing purposes. That’s why everyone with any experience in this energy supply area agrees on the importance of finding multiple value streams. For example, looking at Figure 3, that might mean bundling rooftop and carport photovoltaic generation with battery storage, electric vehicle (EV) charging/energy storage, and a small fossil-fueled genset—all of which might enable (where allowed) the microgrid to earn revenue from selling ancillary services to the grid, lowering overall electricity costs, providing tenant/customer EV convenience as well as power supply security.

Note that each wholesale energy market and state has different rules for what sorts of generation can be owned by customers behind the meter and how power can be moved over what geographic lines. States also vary in interconnection requirements, net metering rules, and what distributed energy resources a utility may own behind the meter. All those factors combine to create an enormous amount of variability in terms of determining what’s legally—let alone financially—viable for a new microgrid. As a result, especially when you look beyond building-level microgrids, project design is likely to require customization for the foreseeable future. |

Model Before You Build. For years, microgrid developers have recognized that, although the parts of a microgrid are all familiar, designing an effective installation (especially one with multiple generation and storage components) poses new sorts of system integration challenges. Especially in an arena where you have new players and familiar players in new roles, there are going to be unknown interconnection behaviors that can potentially damage expensive equipment. The more you model, the less you’ll have to figure out while operating a microgrid. One new tool to assist with this task is the Microgrid Controller Hardware-in-the-Loop Demonstration Platform (see the images at the top of this story) developed at the Massachusetts Institute of Technology’s (MIT’s) Lincoln Laboratory (Lincoln Lab).

Several researchers involved in the Lincoln Lab project were on hand at the Microgrid Summit to display and discuss their “physical model” of a microgrid—essentially a test integration model. Researchers hope it will be used as a development, deployment, and standards-testing platform to help accelerate microgrid deployments, MIT’s Kendall Nowocin explained. The platform uses the configuration of an anonymized real-world power system (code name “The Sheriff”) operating as a microgrid.

There are three levels of control on a grid of any size, Nowocin told POWER: primary—for performing equipment protection at microsecond to millisecond speeds, secondary—for controlling forcing functions (frequency, voltage, power, power factor) at millisecond to second speeds, and tertiary—the supervisory level that doesn’t directly control equipment, operating at seconds to minutes speeds. The Lincoln Lab model can import a one-line diagram (schematic) of any existing or planned microgrid in the 1-MW to 50-MW range to test how microgrid controllers (the tertiary level) from various vendors would behave—thereby eliminating many of the current unknowns that can spell trouble for one-off projects.

Anyone, including vendors, can use the “Sheriff” model, and the lab planned to release the model’s source code publicly in April (contact [email protected]). Phillip Barton, director of Schneider Electric’s North American Microgrid Competency Center, said he recommends working with Lincoln Lab and that, as his company moved into hardware-in-the-loop testing, they learned it is less risky than onsite testing.

Consider Different Configurations for Different Purposes. Although there are benefits to standardization and replicability, some circumstances may call for atypical solutions. Direct current (DC) microgrids are one example.

Andrew Yip, a business development manager with Robert Bosch (Bosch), told POWER his company is developing high-voltage building-level DC microgrids. It has two systems in place in North Carolina (one at Fort Bragg) and two more going in this year, one at a Bosch facility in Michigan and another supported by a California Energy Commission (CEC) grant for a project in Los Angeles.

By coupling solar and storage with heavy AC loads that are converted to DC loads—especially LED lighting, industrial fans, and forklift chargers (Figure 4)—Bosch says it can save 3% to 4% on conversion losses. That can add up to substantial energy savings for businesses.

|

|

4. DC microgrids yield savings. Loads can be as important to microgrid success as generation. By converting large commercial and industrial loads like LED lighting, fans, and forklift chargers to direct current (DC) power, solar-plus-storage microgrids delivering DC power can skip the inverter and the associated conversion losses. Courtesy: General Electric |

Reliability Is Always Important. Whether you are designing a microgrid primarily for backup power or to participate in energy markets to reduce power purchase costs, reliability as a means of securing resiliency for a building, process, or community, should always be considered—even if assigning this benefit a dollar value is difficult. If you are not providing some level of resiliency, you’re leaving value on the table.

Third-Party Financing Remains Important. As in the early days of solar power, external financing sources can help get a microgrid project off the ground. CPUC advisor Ormond noted that different funding options can be available depending on the microgrid’s goal. In California, for example, there are options for projects related to energy and water management.

When Will Microgrid Business Models Mature?

How long will it take for the emerging forms of microgrids, especially community microgrids, to move beyond pilots and one-off projects to predictable, purposeful, and profitable?

Three main factors were mentioned repeatedly at the March Microgrid Summit as being critical to increased and improved microgrid deployment: energy storage, regulatory reform, and financing. In contrast to discussions at the event two years ago, technology conundrums were much less of a concern—which is not to say that designing and controlling a microgrid is easy.

The good news is that most of the people involved in discussions about microgrids today understand that ensuring a facility’s or a community’s resiliency by way of a reliable microgrid requires more than renewable generation; it also requires rechargable energy storage and/or some form of fossil-fueled generation (typically, natural gas or diesel) with an ensured fuel supply.

During one of the summit’s closing sessions, moderator Steve Pullins asked his panelists how long it would take for microgrid business models to mature. Responses ranged from two years to eight years, with Pullins falling into the “next couple of years” category because, he said, activities like the New York Prize and CEC programs will help everyone figure out the business models.

Others noted earlier in the session that the solar PV market faced similar challenges and that the solar cost and business maturity curve shifted quickly, even though a decade ago it struggled to define the value proposition and figure out a financing model.

To that point, John May, managing director of Stern Brothers & Co., said he thinks of SolarCity “as one of the great finance companies.” He thinks the value proposition could be clarified once the microgrid market determines if it’s dealing with a “project asset or a service.” It took SolarCity years to figure that out, he observed. May said there’s plenty of money out there, and he doesn’t see “the story of microgrids” as complex for firms that are already investing in solar and other DERs.

We’ll see in a couple of years if these predictions were on target. ■

— Gail Reitenbach, PhD is POWER’s editor.