Beacon Power Makes a Comeback

Beacon Power Corp. was founded in 1997 to develop flywheel-based energy storage technology. By 2007, the 100-kW/25-kWh Gen 4 flywheel system was commercialized and deployed in several projects. However, market conditions pushed the company into bankruptcy in late 2011. The company has since emerged, reinvigorated with new investment and a new name: Beacon Power LLC.

Fundamentally, Independent System Operators (ISOs) are responsible for the continuous balancing of electricity supply and demand on their regional grids so that the grid frequency remains as close as possible to 60 Hz at all times. In the past, an ISO would send an automatic generation control (AGC) signal to utility generators to increase or decrease output to maintain the supply-demand balance. This process made maintaining grid frequency relatively straightforward.

However, integrating large amounts of intermittent and unpredictable renewable generation on the grid, particularly wind and solar, makes maintaining the supply-demand balance more difficult, particularly when the response of traditional electricity supply resources is relatively slow compared with the rapid see-saw output from a photovoltaic system on a partly cloudy day.

Researchers at Pacific Northwest National Laboratory studied the comparative value of the relatively slow response of AGC-controlled resources with fast-response flywheel-based regulation and reported their conclusions in a report: “Assessing the Value of Regulation Resources Based on Their Time Response Characteristics.” An important conclusion was that 1 MW of fast-response energy storage–based regulation has twice the system regulation value of average conventional regulation resources.

Why Flywheel Energy Storage?

There are other important advantages to an ISO of using flywheel-based frequency regulation. For example, the flywheel energy storage system allows the ISO to recapture a portion of the generation capacity that otherwise would have been allocated for frequency regulation.

Also, if the flywheel-based system is located so that it can inject regulating power on the transmission system, then transmission and transformation losses may be reduced, freeing up transmission line capacity in congested regions. A flywheel system can be sited so it can inject regulating power at the distribution level to reduce grid losses, eliminating the need for conventional regulation plants to use a portion of needed grid capacity for regulation. In addition to grid frequency regulation, once flywheels are fully charged, they can also be used as a temporary grid backup and may be suitable for “black start” service in certain applications.

Beacon Power Corp. was founded in 1997 to commercialize flywheel technology to address the rapidly developing fast-response frequency regulation market and went public in 2000. Its first flywheel systems, the first and second generations of the technology, were deployed in North America for telecommunications backup power applications. Since 2004, the company’s focus has been development of a system that could “recycle” electricity from the grid, absorbing it when demand dropped and injecting it when demand increased.

The first grid-connected Gen 3 (15 kW/4 kWh) was introduced in 2004, followed by the familiar Gen 4 (100 kW/25 kWh) model in 2006 that now has over 3 million operating hours in commercial service (see sidebar). During 2005–2006, Beacon Power participated in 100-kW demonstration projects (using multiple Gen 3 modules) in New York and California. ISO-NE also sponsored a very successful 3-MW pilot program during 2008–2010.

How the Flywheel System Works

Beacon’s flywheel is a mechanical battery designed for a minimum 20-year life, with virtually no maintenance required for the mechanical portion of the flywheel system over its lifetime. Of critical importance in performing frequency regulation with energy storage–based systems is their cyclic life capability.

Beacon’s experience to date in ISO New England shows that 6,000 or more effective full charge/discharge cycles per year are required. The system is capable of more than 100,000 full charge/discharge cycles at a constant full power charge/discharge rate, with zero degradation in energy storage capacity over time. For the frequency regulation application, flywheel mechanical efficiency is over 97%, and total system round-trip charge/discharge efficiency is 85%.

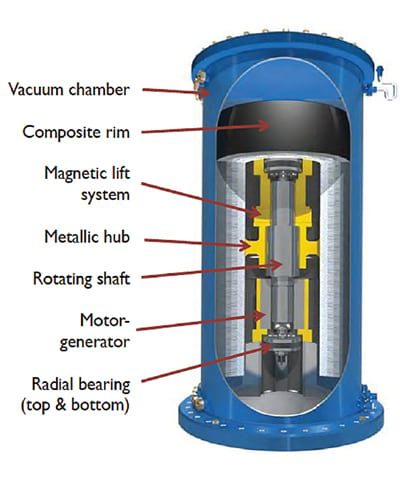

At the heart of Beacon’s Gen 4 flywheel is a high-strength carbon fiber composite rim, supported by a metal hub and shaft, with a motor/generator on the shaft. Together, the rim, hub, shaft, and motor/generator assembly form the rotor. To nearly eliminate friction, the rotor is sealed in a strong vacuum chamber and levitated magnetically. Figures 2–4 show the assembly of a flywheel unit.

|

| 2. Flywheel cutaway. The 100-kW Gen 4 flywheel uses a magnetic lift system to suspend the rotating mass within a vacuum to reduce friction. A motor-generator is used to spin up the rotating shaft when absorbing power but is used as a generator when injecting power into the grid. Courtesy: Beacon Power LLC |

|

| 3. Rim install. A composite rim is installed inside the vacuum chamber in the company’s manufacturing facility located outside Boston. Courtesy: Beacon Power LLC |

|

| 4. Finish assembly. A worker completes installation of the motor-generator and other internals in a 100-kW Gen 4 flywheel module. Courtesy: Beacon Power LLC |

The rotor spins between 8,000 and 16,000 rpm. When absorbing energy, the flywheel’s motor acts like a load and draws power from the grid to accelerate the rotor to higher speed. When discharging, the motor switches into generator mode, and the inertial energy of the rotor drives the generator, creating electricity that is injected back into the grid as the rotor slows down. At 16,000 rpm, a single Gen 4 flywheel can deliver 25 kWh of extractable energy (100 kW for 15 minutes). Multiple flywheels are connected in parallel to provide any desired rating. The Stephentown Project, rated at 20 MW/5 MWh, consists of 200 Gen 4 modules.

The culmination of a decade of product development and testing was the grid-connected 20-MW frequency regulation plant at Stephentown, N.Y., in 2011, owned and operated by Beacon Power (as is a 0.5-MW facility in Massachusetts). That made it the world’s largest commercial grid-scale flywheel facility when it went fully commercial in June 2011, supplying the NYISO market.

The Stephentown Plant consists of 10 Gen 4 100-kW modules to produce each 1-MW unit. Twenty units are combined to form the plant’s 20-MW rated capacity (Figure 1). Electronic containers are installed for each group of 10 modules, and a cooling system is installed between two 1-MW units. Each unit is equipped with a transformer that increases the voltage output from 480 V to 13.8 kV. A switchyard transformer increases the plant output voltage from 13.8 kV to the New York grid 115 kV transmission line voltage. Plant reliability remains above 99%, and reached 100% during the last quarter of 2012, with 4,000 effective full charge/discharge cycles per year in response to remotely dispatched NYISO signals.

|

| 1. Power on tap. The Stephentown Plant consists of 200 100-kW modules that provide up to 20 MW for 15 minutes whenever required by NYISO. The plant has been in service for over two years, with overall plant reliability approaching 100%. Courtesy: Beacon Power LLC |

The Stephentown Plant is a “first responder” to frequency deviations in NYISO, where—under a new tariff—resources are dispatched in order of fastest ramp rates. NYISO requires a ramp rate of 20 MW within 6 seconds, although the plant can respond faster, with no limits on degradation due to cycle, duty, depth of discharge, charging rate, ambient temperature, and so on. The plant’s NYISO “performance index” average is greater than 95% since inception—better than any competing technologies. In fact, the plant is capable of providing 35% of NYISO’s regulation requirements with only 10% of the market regulation capacity.

To build the Stephentown facility, in 2009, Beacon Power received a U.S. Department of Energy (DOE) $43 million loan guarantee (of which the company drew about $39 million). When Beacon Power Corp. filed for bankruptcy protection on Oct. 30, 2011, as part of the bankruptcy court proceedings, the company agreed, on Nov. 18, to sell its Stephentown facility to repay the DOE loan.

On Feb. 6, 2012, private equity firm Rockland Capital bought the plant and most of the company assets. It has since rehired most of the staff, renamed the company Beacon Power LLC, and funded construction of a second 20-MW plant in Hazle Township, Pa., that will provide frequency regulation services to PJM. That plant, configured like the Stephentown Plant, will place the first 4 MW into commercial service in September 2013 and the remainder by the second quarter of 2014.

Beacon Power Rebounds

In late April, POWER discussed this remarkable turnaround with Beacon Power CEO Barry Brits to explore the underlying cause of the bankruptcy and how the company expects to earn revenue and build a business. Brits shared that in the past, the company struggled to earn revenue when there was no market tariff in place that placed a monetary value on regulation services, particularly fast-response regulation.

Today, tariff changes are in place in several ISO regions that will pay for regulation services. Other markets are developing, such as MISO and CAISO. Brits believes that Beacon Power is well situated to compete in those markets, particularly as the company’s cost/cycle is much lower than its primary competition, batteries. Brits expects the remaining ISO markets to follow suit in time and develop attractive tariff structures. With an established tariff, Beacon can build plants and earn a return on its investment. This is what Brits described as the company’s short-term plan, over the next year or so.

In the long term, the company will pursue global opportunities where fast-responding grid regulation services have a prescribed market value, particularly in islanding applications and in regions with high power prices and a high percentage of renewables. Not surprisingly, Brits was in Germany exploring market opportunities when we made contact by phone.

Brits noted that the Stephentown plant has provided grid regulation services (called ancillary services in other regions) for two years, earning revenue 24/7 while maintaining high reliability of service. With new tariffs for these services now available, the uncertainty that made investors reluctant to provide financing in the past has been removed. Brits suggests that there is ample money available from energy private equity or from hedge funds to construct new projects without difficulty. The company’s new connection with Rockland Capital has also opened new networks for project financing, expected to be in the range of 50% to 60% debt-to-equity.

As a taxpayer, it was very good to hear that Beacon Power has committed to the repayment of at least 70% of the DOE loan, unlike other firms that have walked away from loan repayments. Beacon’s repayment commitment is a good sign that the company has a strong product and is investing in that product with a long-term perspective.

— Dr. Robert Peltier, PE is editor-in-chief of POWER.