Grid-connected batteries have long been touted as a tantalizing prospect that could help balance electricity supply and demand as the amount of installed variable renewable generation ramps up. New developments suggest that prospect is now a reality.

Energy storage using grid-connected electrochemical battery systems has widely been hailed as a crucial tool to enable widespread integration of renewables, unlock grid flexibility, and bolster grid reliability. For years, battery storage was considered elusive, hindered by high upfront costs and technical setbacks. But over the past decade, battery storage has taken great leaps toward mainstream use, expanding exponentially alongside renewable technologies.

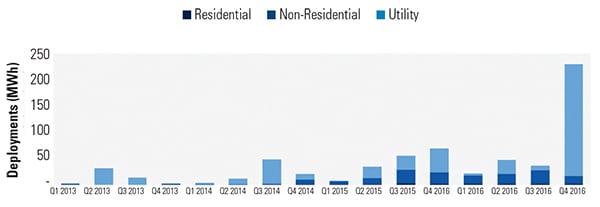

In the U.S., which harbors substantial reserves of pumped hydropower storage, battery storage is now clearly an established market. Battery storage deployments—including from lithium-ion, lead acid, sodium chemistries, and flow technologies—grew to 336 MWh in 2016, doubling megawatt-hours deployed in 2015, according a report released by GTM Research and the Energy Storage Association (ESA) in the first quarter of 2017. The entities remarked that in the final quarter of 2016 alone, 230 MWh came online—more than the sum of the previous 12 quarters combined—driven by a burst in utility installations (Figure 1).

|

| 1. U.S. energy storage deployments (MWh). Source: GTM Research/ESA (U.S. Energy Storage Monitor) |

Worldwide, as of early April, about 733 grid-connected electrochemical projects with a total rated power of 1.8 GW (of varying duration) have been installed, according to the U.S. Department of Energy’s Global Energy Storage Database.

A Global Factor

While a vast amount of research and analyses on the sector exists, the consensus is this growth is expected to continue. IHS Markit, which owns the Energy Storage Intelligence Service, records a global 390-MW pipeline for battery projects, characterized by new announcements in China, Australia, South Korea, and India.

“Energy storage is set to grow as fast as solar photovoltaic energy has in recent years, sparking strong interest from a wide range of players and underscored by recent mergers and acquisitions among car manufacturers, major oil and gas companies, and conventional power suppliers,” said Marianne Boust, a principal analyst at IHS Markit.

Industry experts caution, though, that this growth won’t be even. Several fundamental contributing factors are setting the stage for future battery storage growth in different regions. Every country around the world, they note, has a unique energy storage potential that is based on the combination of energy resources, historical physical infrastructure, and electricity market structure, as well as regulatory framework, population demographics, energy demand patterns and trends, and general grid architecture and condition.

It is more valuable to assess general drivers affecting the sector, the experts say. One of the most important drivers of utility-scale battery storage systems, for example, continues to be the substantial growth in the amount of renewable energy being deployed around the world. Bloomberg New Energy Finance said in a 2016-released long-term forecast that 644 GW of new wind and solar photovoltaic (PV) capacity could be installed worldwide over the next five years. That variable generation could present a host of challenges to electrical grids not designed to handle them, particularly in the developing world, where grids are already stressed delivering existing generation.

Another key driver will involve national targets to curb greenhouse gas emissions under the Paris Agreement negotiated by 197 countries in late 2015. Countries are also generally moving toward improving the resilience of their grids in the face of heightened climate disruptions.

Meanwhile, falling system costs are making battery storage an attractive alternative to certain infrastructure investments. The sector’s relative maturity is also prompting many utilities to consider energy storage systems in resource planning. The financial community, too, is getting comfortable with investments in battery storage.

In the Act of Consolidating

Yet, the sector is still in a state of flux, and it is still unclear whether this will help or hinder the widespread deployment of battery storage.

Surging interest and rapid deployment have attracted an increasing number of actors in the sector, such as utilities, battery manufacturers, and renewable project developers, which are generally helping to drive competition. Greensmith Energy, a U.S.-based firm that designs and deploys energy storage systems and software, noted that in the face of diminished venture capital funding, market participants are also looking to execute on growth strategies and scale-up to maximize profits or decrease costs along the value chain.

Those are some reasons the sector saw multiple large corporate deals during 2016. Total Energy, for example, acquired industrial battery maker Saft, Engie bought Green Charge Networks, Doosan struck an agreement with energy storage systems software provider 1Energy Systems, and Tesla Motors acquired SolarCity.

“Under synergistic circumstances, mergers can certainly jumpstart long-term growth for an enterprise, but the failure rate of mergers and acquisitions is between 70%–90%,” said Ian McClenny, a research analyst with Navigant Research in an August blog post.

McClenny pointed out that enterprises might also choose to acquire companies to fundamentally shift their core competencies to another business segment.

“Creating shareholder value is important to secure longevity in any market; investor expectations help incent company innovation,” he said. “Key motivations behind these acquisitions appear to be project financing and accessibility to behind-the-meter customers. Having more financial resources bolsters a storage company’s influence when bidding for larger grid storage contracts.”

A Technology Shakeout

Meanwhile, over the past three years, battery storage technology markets have seen a general upheaval.

David Hart and Alfred Sarkissian from the Schar School of Policy and Government at George Mason University note that battery technology has followed a diffusion pathway that is characteristic of rapidly growing industries. In the U.S., between 1990 and 2009, battery chemistry or application showed no specific trend. Backed by state research and development, and commercialization programs, such as in New York and California, fewer than 10 projects that were larger than 250 kW came to fruition. Most used sodium-based battery technologies, followed by lead-acid and then nickel-based technologies.

It wasn’t until 2009 that A123 Systems and AES began commercial operation of the first 12-MW/4-MWh lithium-ion battery system for a spinning reserve project at AES Gener’s Los Andes substation in Chile’s Atacama Desert. That year, AES also started up an 8-MW lithium-ion frequency regulation project at a generation plant in Johnson City, N.Y., a project that was the first of its kind to be classified as a generator by the U.S. Federal Energy Regulatory Commission (FERC).

The Battery Pack

Lithium-ion and lead-acid battery technologies contended for dominant market share between 2011 and 2014, a period that also ushered in commercial use of the first flow battery. The U.S. Department of Energy noted that most battery systems installed during that period were used for renewables capacity firming, electric energy time shifting, frequency regulation, and electric bill management. Notable projects that came online during that period were Duke Energy’s 36-MW advanced lead-acid Notrees Wind Storage Demonstration Project in Goldsmith, Texas, a project that sought to optimize energy delivery from an adjacent 153-MW wind farm. AES also started up the Laurel Mountain Project in West Virginia. Rated at 32 MW/8 MWh, that lithium-ion project was sited with a 98-MW wind farm, providing frequency regulation and ramping services to PJM.

Then, two years ago, grid-scale battery systems began to see a more intense period of growth. About 145 MW of lithium-ion projects came online in the U.S. alone in 2015—four times the rated power from lithium-ion systems in any prior year and more than what was added during the entire period between 2009 and 2014—boosted by private financing and fostered by PJM’s now-established frequency regulation services.

Lithium-ion batteries still dominate markets in the U.S. and around the world. GTM Research noted that for the entirety of 2016, lithium-ion batteries held a U.S. market share of about 97% or greater, driven in large part by “massive declines in lithium-ion battery prices and growing acceptance of the technology’s bankability, leading to lithium-ion batteries’ implementation in the majority of large utility-scale projects throughout the year,” the research group said. “This trend is expected to continue, as numerous megawatt-scale procurements were awarded in 2016 to developers implementing lithium-ion technology; these projects are expected to come on-line over the next three to five years.”

Global technology research company Technavio last year suggested that the growing demand for electricity storage could fuel a similar boom worldwide for lithium-ion batteries, projecting that the segment could surpass 3,130 MW by 2020.

Meanwhile, in 2016, lead-acid battery technologies snagged a 1.6% share of installed U.S. battery storage capacity. Technavio suggests that this technology, conceived in the 1960s, will also see significant growth, reaching 990 MW worldwide by 2020. Technology innovations have helped lead-acid batteries achieve increased efficiency and overcome challenges such as slow charging. At the same time, the abundance of available raw materials for lead-acid batteries has increased the number of installations of the battery, said Sayani Roy, an industry expert at Technavio. However, future growth may be tempered by the technology’s short operational lifetime, which only spans on average between three and four years, as well by high maintenance requirements. Additionally, it will face stiff pricing competition from lithium-ion-based systems.

The sodium sulfur (NaS) battery segment is generally expected to do better, growing to 1,450 MW worldwide by 2020. NaS batteries, first developed in 1966 by Ford Motors, offer high energy density compared to other stationary storage batteries, and they can be compact.

Japan’s NGK Insulators in March 2016 built a 50-MW/300-MWh NaS storage system that was delivered to Kyushu Electric Power Co.’s Buzen Substation six months after it was ordered by Mitsubishi Electric Corp. The storage system consists of 252 NGK containerized NaS battery units, and it was installed on a site measuring about 14,000 square meters (Figure 2). One of the world’s largest stationary storage installations, the battery system is part of Kyushu’s demonstration to balance the grid using energy storage on Kyushu Island in southwestern Japan, where huge amounts of solar power have been installed following the 2012 introduction of a feed in tariff.

|

| 2. A large experiment. NGK Insulators supplied 252 containerized sodium sulfur battery units (shown here) for a demonstration project designed to balance the grid on Kyushu Island in Japan. Courtesy: Mitsubishi Electric |

Costs for the technology are also continuously falling. “Also, its high energy density and operating temperatures along with the corrosive nature of sodium polysulfide make it suitable for large grid energy storage,” said Roy. Yet, as with lead-acid batteries, the segment will face competition from lithium-ion technologies, she noted.

Costs for flow batteries have also fallen and efficiencies have improved in recent years, but despite the hype surrounding this segment—they’ve long been touted as the logical choice for grid-scale applications because of their long durations and lifespans, and because they see less degradation from repeated charging cycles than other technologies—advances haven’t been broadly implemented in the field. Progress is on the horizon, however.

Primus Power recently announced that it has started production of its second-generation EnergyPod 2 flow battery, which it says has a five-hour duration, a 20-year lifespan, and costs 50% less than the leading conventional lithium-ion battery system. The company is shipping its battery systems to U.S. and international utilities, such as Puget Sound Energy in Washington.

At the same time, more companies are exploring the potential of flow battery systems. In March, for example, San Diego Gas and Electric (SDG&E) and Sumitomo Electric unveiled a 2-MW vanadium redox flow battery storage pilot project to test whether flow battery technology can economically enhance the delivery of power over the next four years.

Another battery technology that has flourished—but gets little attention despite its competitiveness with lithium-ion batteries—is zinc-air, a battery system that uses air for the cathode, and cheap, abundant zinc in the electrolyte. Arizona-based Fluidic Energy has deployed more than 100,000 zinc-air hybrid batteries in 10 countries, with applications spanning rural electrification and grid-reliability.

Fluidic’s initial commercial installation for Indonesian telecom customer Indosat has been online for over five years now, and since then, the company has expanded to rural electrification, taking the place of diesel gensets in island microgrids (Figure 3) that cannot connect to the national grid. The company is currently preparing to put up a battery system for Duke Energy in North Carolina that will serve a renewable energy microgrid at Great Smoky Mountains National Park.

|

| 3. A lifetime retreat. Fluidic Energy’s zinc-air long-duration energy storage technology has helped offset diesel use in microgrids on 94 Indonesian islands, such as at Sekunyit Island, shown here. The company says the system’s low cost and remote monitoring capabilities are its biggest advantages. Courtesy: Fluidic Energy |

Fluidic said its Indonesian systems, which can be remotely monitored and are theft-proof, fare well in hot and humid regions, and continue to achieve more than 99.5% uptimes. But the technology’s most prominent selling point is cost, which is achieved with low material, manufacturing, and installation prices, Fluidic Chief Technology Officer Ramkumar Krishnan told POWER. “Just to give you perspective, about $5 million of capital can produce about 100 MWh of battery storage on an annual basis,” he said. “And, this is nearly 20 to 25 times lower than a lithium-ion plant or even a lead-acid plant.”

A Shift to Longer-Duration Applications

The fourth quarter of 2016 marked another turning point in battery storage history in terms of application. Over the years, grid-connected battery storage has been used in various ways, including for energy arbitrage, generation capacity deferral, ancillary services, ramping, transmission and distribution capacity deferral, and end-user applications—which entail managing energy costs, power quality and service reliability, and renewable curtailment. During 2016, the burst of new U.S. installments was characterized by large four-hour systems, noted GTM Research. That trend is likely to persist over the coming quarters.

About 88% of installed capacity in the fourth quarter was in California in response to a catastrophic natural gas leak at the massive Aliso Canyon gas storage facility above the Porter Ranch section of Los Angeles in the fall of 2015. That event, thought of as one of the worst environmental disasters in U.S. history, left regional gas-fired generators in a lurch, but rather than reestablishing gas supplies, the California Public Utilities Commission in May 2016 expedited the approval of around 100 MW of battery storage in Southern California Edison (SCE) and SDG&E territories. By the end of February 2017, seven of eight Aliso Canyon–related projects had been completed under emergency tenders, with only 5 MW of the 104.5 MW contracted remaining to come online.

On December 31, 2016, energy infrastructure company AltaGas, which owns six gas power plants in California, started up the Greensmith Energy–built AltaGas Pomona Energy Facility, a 20-MW/80-MWh system. The company also signed a 10-year energy storage agreement (ESA) to furnish SCE with 20 MW of resource adequacy capacity for a continuous four-hour period. The company will receive fixed monthly resource adequacy payments under the ESA and retain rights to earn additional revenue from energy and ancillary services provided by the batteries.

On January 30, SCE opened the 20-MW/80-MWh Mira Loma Battery Storage Facility, constructed by Tesla in just 88 days. The installation features two 10-MW systems comprising 198 Tesla Powerpacks and 24 inverters that were manufactured at the Tesla Gigafactory in Nevada (see sidebar: “A Gigafactory Race”).

| A Gigafactory Race

Tesla Motors this January began mass production of lithium-ion battery cells for energy storage at its Gigafactory (Figure 4) outside Sparks, Nev., a sprawling 5.5 million-square-foot manufacturing facility. The high-performance cylindrical “2170” cell jointly designed by Tesla and Japanese partner Panasonic will be used in Tesla’s Powerpack 2 (see opening photo), Powerwall 2, and by 2018, for its Model 3 electric vehicles.

The facility, which is being built in phases, was about 30% complete as of January. It is expected to be capable of producing 35 GWh of lithium-ion battery cells per year. The facility’s completion in 2020 could mark a new turning point for battery storage technology, as mass production will make batteries cheaper than ever before. Tesla—which is calling a solar photovoltaic module facility acquired from SolarCity in Buffalo, N.Y., “Gigafactory 2”—has plans for Gigafactories 3, 4, and possibly 5. The locations of those plants may be finalized later this year. It has its sights set on Europe, too, acquiring German manufacturing automation specialist Grohmann Engineering last November to help it ramp up production volume and quality while cutting costs. France, Spain, the Netherlands, and Portugal are actively wooing Tesla to establish manufacturing capacity in their countries. But by the time those Tesla facilities ramp up to full capacity, the market could be crowded. German battery firm BMZ in May 2016 opened the first phase of its lithium-ion battery factory in Karlstein, Germany. Samsung SDI in August 2016 said it would start up its own massive electric vehicle battery production factory in Hungary by mid-2018, a facility that could churn out 2.5 GWh per year. South Korea’s LG Chem, meanwhile, is already building a battery cell factory in Poland and has plans for new factories in Michigan and China. And this March, former Tesla executives who founded InnoEnergy unveiled plans for a $4 billion factory in the Nordic region that could produce up to 32 GWh per year of lithium-ion battery cells. |

And on February 24, Sempra Energy subsidiary SDG&E unveiled a 30-MW/120-MWh lithium-ion battery energy storage system in Escondido, Calif. (Figure 5), just days after it put another 7.5-MW/30-MWh system online in El Cajon. AES Energy Storage built the two projects, fast-tracked under “expedited ongoing negotiations.”

|

| 5. Instant recharge. Wrapping up a fast-track procurement process that began less than a year ago, California utility San Diego Gas & Electric (SDG&E) on February 24 officially put into service the 30-MW/120-MWh system supplied by AES Energy Storage in Escondido, Calif.—a project that is currently the largest lithium-ion storage battery in the world. Source: POWER/Tom Overton |

At the facility’s unveiling, Josh Gerber, SDG&E’s manager of advanced technology integration, told POWER it would serve mainly in a time-shifting role, charging during the day and discharging during the evening as a “bulk resource for the grid.” AES Energy Storage President John Zahurancik noted that the quick evolution of battery storage technology had made this new role possible. Battery storage system costs have plunged 85% since AES’s first project in Huntington Beach, Calif., in 2009, he said. “If we had faced these challenges just a few years ago, we would be looking at a new gas power plant.”

Charging Forward

According to GTM Research, the momentum from the Aliso Canyon response will continue, enabling California to further its dominance as the biggest battery storage market over the next five years. Hawaii, Massachusetts, New York, and Texas will vie for the second spot, buoyed by promising policy developments. Generally, the U.S. market will see a nearly 12-fold expansion from 221 MW in 2016 to roughly 2.6 GW in 2022, GTM Research forecasts.

Among recent crucial front-of-the-meter policy developments, Oregon’s Public Utility Commission earlier this year issued guidelines under the 2015-enacted HB 2193, a law that requires Oregon utilities Portland General Electric and PacifiCorp to have a minimum of 5 MWh of energy storage in service by January 2020. Massachusetts, in August 2016, meanwhile, became the third U.S. state to enact an energy storage mandate, though the exact volume that must be procured by January 2020 won’t be decided by the state Department of Energy Resources until this summer. California, which enacted a mandate in 2014, requires utilities to procure 1,325 MW of energy storage by 2020.

As significantly, New York City in September 2016 unveiled the first citywide mandate, aiming for an energy storage goal of 100 MWh by 2020. Hawaii, which recently passed a 100% by 2045 renewable energy mandate, saw its state legislature introduce bills on energy storage tax credits and infrastructure loans.

On a federal level, FERC issued a notice of proposed rulemaking calling for broad changes in organized wholesale markets to encourage energy storage participation. In Congress, a bipartisan group of lawmakers introduced a bill to establish a 30% investment tax credit for storage, though industry observers are skeptical this will come to fruition any time soon.

Around the world, a number of countries also implemented policy measures that should help battery storage thrive in commercial markets. In late 2016, the UK’s Electricity Storage Network awarded 15-year contracts to projects with storage components. In the European Union, where a market design initiative already seeks to provide a level playing field for all electric grid flexibility solutions, a proposed recast of the Renewable Energy Directive seeks to support energy storage for integration of renewables on the grid.

According to the International Finance Corp. (IFC), China—which has already widely been deploying storage throughout its grid—is in the process of reforming its energy markets, opening opportunities for independent power producers to provide ancillary services and capacity with battery storage systems. Similar measures are underway in Chile, Brazil, and Mexico.

In India, a July 2016 tender for several hundred megawatts of solar PV capacity includes the requirement for every 50 MW of PV capacity to have 5 MW/2.5 MWh of associated storage. And in sub-Saharan Africa, where remote power systems are expected to provide roughly 70% of energy services over the next few decades given the lack of grid connectivity, “It is expected that the majority of these remote power systems will include energy storage as the technology continues to decrease in price, and many power systems will begin to rely more heavily on variable renewables,” said the IFC.■

—Sonal Patel is a POWER associate editor.

Editor’s note (May 9, 2017): Corrects quote by Fluidic Chief Technology Officer Ramkumar Krishna to read: “And, this is nearly 20 to 25 times lower than a lithium-ion plant or even a lead-acid plant,” not “20% to 25%” as the original article noted. Also notes that Fluidic’s installation for Indonesian telecom customer Indosat has been online for more than five years now, and that the company has since expanded to rural electrification.