Construction activity on wind projects across the U.S. surged to a record level of more than 20 GW in the third quarter of 2018, and about 35.1 GW of new wind capacity was under construction or in advanced development at the end of 2018, according to the American Wind Energy Association (AWEA).

In 2018, the wind industry installed 7.59 GW of new wind capacity—marking the fourth year in a row that the industry has installed at least 7 GW, the trade group said in its annual market report. Once projects in the pipeline are complete, they will boost the current total of 96.4 GW (from 56,000 wind turbines operating in 41 states plus Guam and Puerto Rico) to 131 GW.

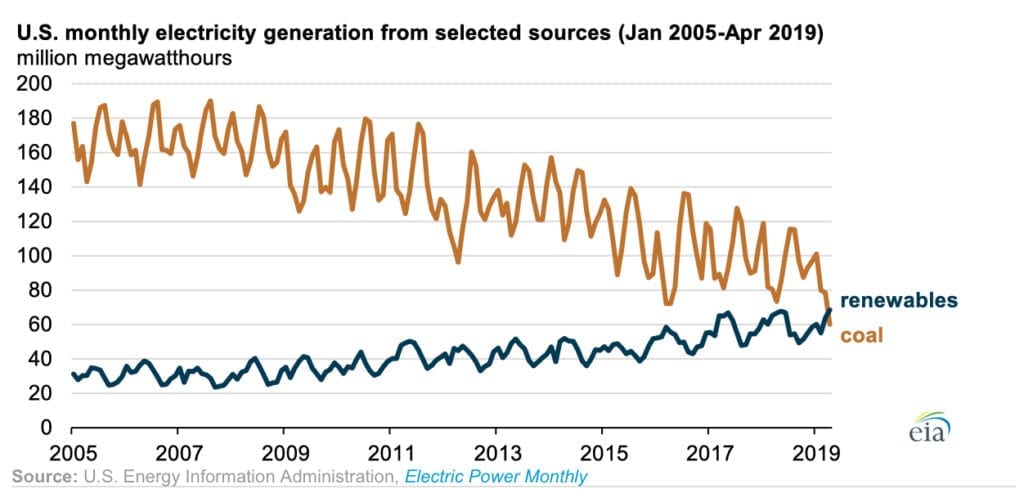

A History of Boom and Bust

The construction frenzy is partly due to the looming phase out of the production tax credit (PTC), which allows wind developers to qualify either by starting physical construction or making a 5% capital investment in a project by the year-end deadline. It also requires projects to begin operations within four years after construction begins. The PTC was extended in December 2015 at full value for projects that began construction by the end of 2016, but it is designed to diminish to 80% of full value in 2017; 60% in 2018; and 40% in 2019.

“When you see the charts included in the 2018 market report, you’ll see historically, this boom-bust thing going on, and you’ll see, since 2015, a very steady strong deployment—7, 8 GW for several years now,” AWEA CEO Tom Kiernan told reporters at a briefing in Houston on April 9. “And we anticipate that will continue, if not, frankly, increase in the next several years, and again it’s because of that long-term policy that has allowed any number of companies to make investments.”

Several major original equipment manufacturers have announced new, more-efficient and larger turbine designs to keep driving down costs, Kiernan added. “I think in the long term, as we phase off the PTC, there’ll probably be a softening. But because of this five-year horizon, we’re going to be one or two product cycles further in the technology, and we’re optimistic long term, given we’re the currently cheapest source of new electricity in most parts of the country—unsubsidized.”

Drivers: Low Costs, Soaring Corporate Uptake

AWEA told POWER it pegs the levelized cost of electricity to a number of sources, including Lazard (see “The Big Picture: Cost of Power Comparison” in POWER’s April 2019 issue), BNEF, Navigant, and others. The group claims the cost of wind has fallen 69% between 2009 and 2018 as the industry continues to improve performance through new technologies.

Declining costs and the stable price of wind power are already driving new power purchases, Kieran noted. In 2018, 37 corporations, including 21 first-time buyers, signed wind energy contracts totaling a record 4.2 GW. At the end of 2018, meanwhile, commercial and industrial purchasers had signed contracts for more than 11.3 GW of wind, while utilities signed contracts for 4.3 GW.

Those agreements are transforming generation profiles in key markets, which marked notable wind power records in 2018. Southwest Power Pool (SPP), for example, generated 24% of its power from wind, and the Electric Reliability Council of Texas (ERCOT) generated 19%. Wind output records were also set across the country in “every regional transmission organization and independent system operator at some point in 2018,” Kiernan added. ERCOT, for example, experienced the most wind output at a single point in time at more than 19 GW, while SPP set a record at 16.3 GW.

ERCOT’s surge in wind and solar generation, and recent coal plant closures, prompted worries about a generation scarcity this summer, and the grid operator in March warned that it could issue energy alerts at “various times.” According to the Texas Competitive Power Advocates, a group whose members collectively produce about 60% of Texas’s power, the grid’s reliance of intermittent resources like wind poses a major risk.

AWEA CEO: Wind Will Not Do It Alone

On Tuesday, Kiernan acknowledged concerns about variability, but he noted the market was shaping new solutions. WINDPOWER, AWEA’s trademark conference which will be held in Houston this May, will be attended by more than 8,000 attendees, many from other sectors, including solar, storage, and gas, he said. “Increasingly, we’re seeing it’s all about ‘wind-plus.’ It’s about wind connecting with solar and gas and storage,” he said. “That’s where the grid is heading and we’re very much part of that future.”

However, to keep the “momentum going,” the industry will still continue to seek state policies that support low costs. “In states, we’re looking for economic environments that have low cost and stable pro-investment policies,” he said. Transmission is also a key focus on a federal level. “Our transmission grid is outdated and is not built out to provide the clean energy sources for the future.” And while the “cost of transmission is built into the cost of wind energy,” the industry will still “need to get the transmission planned and permitted,” he said.

AWEA is also backing policies to promote storage, such as the storage investment tax credit bill introduced in the U.S. House on April 4. “A tax credit for storage on the grid would help wind, but it would also help solar and all other sources of electricity on the grid because it makes the grid stronger and more reliable,” Kiernan said.

At the same time, it is collaborating with the solar industry and others to encourage the creation of markets for reliability services. “So, for example, when you have to start up the grid or to maintain certain voltage levels or frequency levels, wind does that really well on the grid, but it isn’t currently compensated for that,” he said. “So, shocking concept, we’re saying, hey, create a market where we compete—wind and solar and gas and coal and whomever—compete to provide those reliability services and then compensate that source of electricity … that is able to provide that service at the lowest cost.”

A Gust for Offshore Potential

Meanwhile, the wind industry is closely watching developments concerning the offshore wind sector. AWEA said that improving project economics and growing backing from state policies led to a surge in offshore wind activity in 2018. By the end of the year, project developers had a potential offshore wind pipeline of more than 25.7 GW spanning 10 states in the Northeast, Mid-Atlantic, and Great Lakes region. Six offshore wind projects, totaling 2.1 GW could be operational by 2023, it said. Over 2018, meanwhile, utilities selected 1.5 GW of offshore wind capacity through state-issued solicitations, and power purchase agreements were signed for two offshore projects totaling 1 GW at prices below $100/MWh.

Kiernan told POWER that activity is concentrated on the East Coast for two likely reasons: “One, there’s a lot of consistent wind there, and two, there’s a lot of load.” Analysis has been conducted for the Great Lakes, off the coast of California and Hawaii, and possibly even the Gulf Coast, he said. AWEA noted that states have “taken the lead in looking at how to develop” offshore projects, owing to carbon or renewables goals.

—Sonal Patel is a POWER associate editor (@sonalcpatel, @POWERmagazine)