There is no doubt that the year-plus since passage of the American Recovery and Reinvestment Act of 2009 (Recovery Act) has borne witness to a great deal of activity among the diverse groups of smart grid stakeholders. On May 18, 2009, U.S. Energy Secretary Steven Chu declared: "The Smart Grid is an urgent national priority that requires all levels of government as well as industry to cooperate…. We still have much to do, but the ultimate result will be a much more efficient, flexible power grid and the opportunity to dramatically increase our use of renewable energy."

In the fall of 2009, the federal government announced Recovery Act awards totaling more than $4 billion to 132 smart grid projects around the country. In January 2010, the National Institute of Standards and Technology (NIST), acknowledging the need to accelerate the establishment of a "flexible, uniform and technologically neutral" set of standards to guide smart grid component vendors, published its final Phase 1 report entitled "NIST Framework and Roadmap for Smart Grid Interoperability Standards, Release 1.0." In short, the federal government has made its priorities clear.

Something Different for Everyone

The story of the blind men and the elephant has resurfaced as a popular metaphor for describing smart grid development to date. It is hard to imagine stakeholders with less in common: venture capital – backed software and technology vendors and electric utilities. The former have been entering the space in large numbers since about a year ago, offering home energy management systems (HEMS), home area networks (HANs), in-home displays (IHDs), and other Internet-age data processing and management products. The electric utilities, on the other hand, are necessarily circumspect in their approach to overhauling the grid while simultaneously delivering uninterrupted, reliable, stable electrical service.

The overall vision of a "smart" electricity grid is exhilarating: integrating software, communications, and automation technology to digitally monitor, process, and communicate massive amounts of real-time data bi-directionally, all for the purpose of reducing our energy consumption, enabling the deployment of more renewable and distributed generation energy resources, and delivering less-expensive electricity to consumers in a reliable and secure way. But given the complex realities of the grid, it’s not surprising that initial attempts at smart grid deployment have been marked by fragmentation.

Finding Common Goals

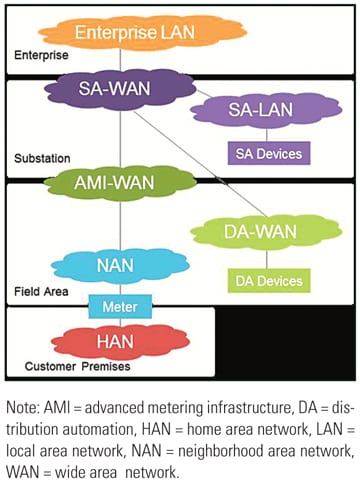

The smart grid enterprise is beginning to come into focus. From the utilities side, deployment of smart meters and advanced metering infrastructure represents the first foray into new technology integration. Spurred by Recovery Act funding, the smart meter market is expanding rapidly, and according to one report, the number of installed smart meters worldwide is expected to grow from 46 million in 2008 to 250 million in 2015. Given their familiar form and functionality, smart meters enable utilities to take a nonthreatening first step in the migration to a smarter grid. Utilities can initially use them to collect energy usage data in real time, where it can be used for billing purposes and remote connection and disconnection of customers. As utilities become acclimated to the data collection and two-way communications capabilities of smart meters, they are also beginning to apply what they are learning to systems optimization, thereby paving the way to integrate new technologies that will improve the reliability and efficiency of the grid.

Coming at it from another direction, the deployment of smart meters has spawned a wave of innovation by privately funded start-up companies focused on electricity consumers and offering HEMS, HANs, and IHDs. One industry analyst projects that the HAN market alone will reach $3 billion annually within the next two years. These products and devices promise to enable consumers of electricity, both commercial and residential, to use the data collected by smart meters to monitor their energy usage and make informed consumption decisions. Ultimately, real-time data and bi-directional communications between utilities and electricity consumers could yield more systemic benefits. They include leveling the load curve by offering consumers time-of-use pricing that will incentivize them to do things like program their home systems to turn off air conditioners and appliances during high-demand times (when electricity is more expensive).

The froth in this nascent smart grid technology space makes it difficult to differentiate among different companies’ offerings or determine their relative longer-term value to the smart grid endeavor. Companies that have adopted go-to-market strategies that directly target electricity consumers while largely sidestepping utilities may enjoy a modest first-mover advantage from early adopters of technology on the end user side of the equation. It is logical to assume, however, that companies that prove successful at leveraging relationships with utilities, whether directly or through technology aggregators, will enjoy deeper and more widespread penetration into homes and commercial buildings.

Smart Vendors

The "smartest" smart grid vendors, however, may be those who take the time to engage utlities now. Those that put together easy-to-deploy, out-of-the-box, end-to-end solutions that combine low-cost, user-friendly interfaces with stable, secure, thoughtful, and sufficiently powerful data processing and management functions, as well as flexible open platforms that allow utilities to "drop in" new applications as their needs evolve, likely stand to gain the most. Although utilities are historically slow-moving and circumspect customers of new technologies, when it comes to understanding how electricity is bought, sold, delivered, and managed, no one knows more, and the customer is always right.

—Haeryung Shin (haeryungshin@dwt.com) is chair of the Clean Technology Group at Davis Wright Tremaine LLP.

[Ed: This byline was corrected 5/4/10]