The People’s Republic of China’s Congress approved a much-anticipated draft of the country’s 12th Five-Year Plan (2011–2015) on March 14. Along with key objectives that included boosting its gross domestic product (GDP) by 7% annually on average, the country for the first time in a five-year plan established targets to tackle climate change. It plans to reduce carbon dioxide emissions per unit of GDP by 17% from 2010 levels by 2015 and to reduce energy consumption per unit of GDP by 16% from 2010 levels by 2015.

China achieved to some extent what it had set out to do in its 11th plan, managing to reach a 19.1% reduction (of a planned 20%) in energy intensity and producing 9.1% of primary energy from non–fossil fuel sources. It should be noted, however, that as pressure intensified on local officials to meet these targets in late 2010, last-minute measures resulted in disruptive actions that included blackouts and forced factory closures.

Meanwhile, power consumption continues to soar. As reported by the State Grid Corp. of China, it was already up in the first two months of this year, reaching 702.2 TWh—12.3% above last year—and estimates are that this year’s total consumption will reach 4,600 TWh, up 10% from last year.

To meet demand, as it did in its 11th five-year plan in 2006, the country’s 12th plan lays out aggressive energy targets and plans to phase out inefficient coal plants. About 70 GW of small, inefficient coal-fired capacity was phased out between 2006 and 2010, and 8 GW is scheduled to be phased out in 2011. The 12th plan includes an increased percentage of “new energy” consumption, totaling 11.4% by 2015, though analysts point out that this is still under discussion. (In the 12th plan, the category of “new energy” includes cleaner coal and coal-bed methane power projects as well as smart grid projects.) A total investment (public and private) of 5 trillion yuan ($761.3 billion) is expected in the sector by 2020.

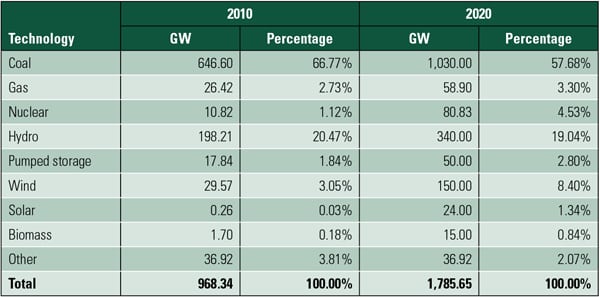

About 40 GW of this cleaner energy was expected to come from nuclear power by 2015, though after the Japanese nuclear crisis, China’s media reports that plans have been pulled back to 80 GW from the 90 GW previously expected to be built by 2020. Emphasis will be on reactors based on Westinghouse’s third-generation AP1000 reactor. The new plan also calls for a massive, 75-GW expansion of new hydroelectric capacity (12 GW of which would be pumped storage), a 13-GW to 33-GW surge in gas generation, and 90 GW in new wind capacity (5 GW of which is to be offshore wind). Analysts expect China could far exceed its 150-GW target for 2020; installations of cleaner power could total 240 GW, they say.

The country will continue to source a majority of its power from coal, and it plans to add an estimated 260 GW of coal power by 2015, though coal’s share is expected to fall to 63% from the current 72%. A key difference between the 11th and 12th plans is that the government will likely control the growth of the coal industry and cap annual production capacity at 3.8 billion tons by 2015, up from the current capacity of 3.2 billion tons. “To cap growth at this level means the growth rate will need to be less than half of the rate in the 11th [five-year plan] period,” analysts from HSBC said.

|

| 2. A river bank. In its 12th five-year plan (2011–2015), China is looking to expand its hydropower capacity by 63 MW, and add 12 GW of pumped storage, to boost its non-fossil-powered portfolio and meet newly established climate change targets. Several mega-dams are under construction, though none as big as the Three Gorges Dam on the Yangtze River (shown here). One facility that will come online during the 12th plan is the gargantuan 6.4-GW Xiangjiaba hydropower project in southwestern China, expected to be fully operational in June 2012. Courtesy: Le Grand Portage |

The 12th plan also calls for a fundamental shift in the nation’s solar photovoltaic (PV) industry. Analysts say that in 2011, China is expected to increase its share of the global PV module market by 10%, making it responsible for 59% of the world’s solar PV industry. The country recently enacted regulations to phase out excess polycrystalline silicon manufacturing in the long term; overproduction led to a supply glut in 2010.

Last year China made major strides in installing high-voltage transmission lines, and within the next five years it will continue to develop its grid. State Grid has announced an investment plan for 2009–2020 with provisions for 384.1 billion yuan (US$58.5 billion) worth of investment in smart grid technology (split between 30.8% for smart use, 23.2% for smart distribution, and 19.5% for substations). This will account for just 11% of total grid investment, however.

—Sonal Patel is POWER’s senior writer.