Why is a power generation industry publication covering the smart grid (SG), which most people tend to equate with managing electricity use (and maybe its transmission)? Of the many reasons, here are two of the most obvious. Slowly but surely, SG projects will have implications for those involved in everything from resource management planning (Do we build another gas-fired plant, or add a solar plant to an existing gas plant, or integrate distributed solar resources?) to staffing power generation projects (Can we scale back at our thermal plants so we can add more maintenance staff for distributed generation resources?). Second, as more renewable resources get added to the grid, the operation and maintenance of baseload plants becomes more complex—at least until better grid-balancing tools are in place across the continent.

In conjunction with POWER’s January forecasting issue, this report looks at the state of the smart grid and offers a few predictions about what its near-term future holds.

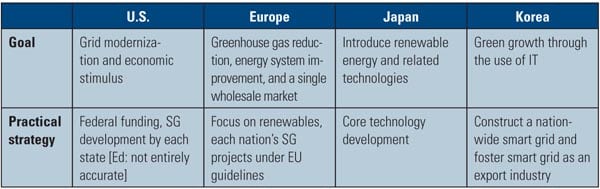

Also see the related stories that explore how other countries are implementing elements of a smart grid (“Which Country’s Grid Is the Smartest?”) and what residents of SmartGridCity expect from that city-wide experiment (“What Do Customers Expect from the Smart Grid?”).

The Grid Is a Slow Learner

Few in the power industry would deny that the U.S. is way overdue to upgrade its electricity transmission and distribution grid. For well over a decade, technology vendors have been encouraging investment in transmission and distribution (T&D) projects, touting the merits for utilities and customers alike of digital tools to create a “smart” grid. Unfortunately for those manufacturers, “If you build it, they will come” remained mostly a wish rather than widespread reality.

Sure, there have been several relatively small-scale pilot projects involving everything from “smart/digital” meters to broadband-over-power line installations to digital fault-detection devices. But the cost of widescale implementation has been a showstopper for the most utilities—at least in the U.S.

Several converging factors indicate that 2010 may well be the year that the smart grid gets a substantial kick-start. They include:

- The economic meltdown of 2008, which led to American Recovery and Reinvestment Act (ARRA) funds being awarded in late 2009 for smart grid (SG) and T&D projects.

- High unemployment, and the resulting desire of federal, state, and local governments to show that they are creating new jobs. Among the areas most promoted are clean energy jobs. T&D projects that enable new renewable generation to reach load centers are placed in this category.

- Building momentum (internationally but also nationally) for climate change legislation, which puts a premium (one way or another) on low-carbon electricity sources. Renewable energy sources in many cases require new wires and more sophisticated grid management than current tools enable. Additionally, energy usage management, enabled by SG hardware and software, can mean reduced energy demand (MW) and consumption (MWh), hence lower (or slower-growing) greenhouse gas emissions.

- On Sept. 24, the National Institute of Standards and Technology (NIST) released “NIST Framework and Roadmap for Smart Grid Interoperability Standards Release 1.0 (Draft),” which proposed 77 standards for smart grid development. As the draft report notes, “Without standards, there is the potential for these investments [from ARRA] to become prematurely obsolete or to be implemented without necessary measures to ensure security.”

- The commitment of arguably the most influential corporation in the country, Google, to SG software and information management. For example, the company is promoting its Google PowerMeter, “a free electricity usage monitoring tool that provides you with information on how much energy your home is consuming. Google PowerMeter receives information from utility smart meters and in-home energy management devices and visualizes this information for you on iGoogle (your personalized Google homepage). And, Google PowerMeter is free.” This initiative has utility partners in the U.S., UK, and Germany, though more are said to be testing the service. Former astronaut Edward Lu, a physicist with a degree in electrical engineering, leads this Google venture.

- Industry consolidation is picking up steam, with bigger and better-financed companies absorbing smaller ones. Consolidation could simplify decisions for utilities and standard-setting entities.

Money Builds the Smart Grid

Some folks who monitor the smart grid universe had the distinct sense last fall that utilities and other companies that were in a position to engage in SG projects were holding on tight to their pocketbooks until the federal government sweetened the pot. For example, in an Oct. 23 blog entry Matt Marshall—editor and CEO of VentureBeat, a blog that tracks the venture capital market—noted that Silicon Valley startups hadn’t seen a lot of business from smart grid projects yet. Marshall, who was also the organizer of the GreenBeat 2009 smart grid conference last November, quoted Michael Kaufman, principal at the Westly Group, a venture capital firm that invests in green-oriented companies, as saying, “Most entrepreneurs are the most optimistic and energetic people in the world, . . . but Smart Grid people tend to look beaten down when they arrive at our office. We make the espresso stronger when they arrive.” Marshall and Kaufman noted that they expected opportunities to materialize once federal funds were released.

As expected, in the fourth quarter the federal government made a massive cash infusion into smart grid–related projects.

On Oct. 27, President Obama announced that 100 smart grid projects would share $3.4 billion in grant awards funded by ARRA. A condition of the awards is that they be matched by industry funding for a total public-private investment worth over $8 billion. Every state except Alaska will benefit from some aspect of at least one of the projects. (It’s not clear if Alaskan utilities even applied for the funds.) Then, the following month, winners of $620 million for smart grid demonstration and energy storage projects were announced. Those two award announcements accounted for the largest portions of the $4.5 billion in total ARRA funds being handled by the Department of Energy.

Earlier in the fall, at GridWeek 2009 in September, Secretary of Energy Steven Chu noted that, from the $4.5 billion being made available from ARRA funds for grid modernization, $750 million would go to transmission loan guarantees. He also announced at GridWeek the availability of $100 million to “train a new generation of utility workers” and $44.2 million in awards to state public utility commissions to “hire and retrain staff as utilities ramp up Smart Grid activities.” (For a full listing of smart grid–related federal funding opportunities, see this DOE site.)

So, once the fine print details of cost-sharing and other challenges get ironed out, will the grid be transformed overnight? No. One reason is that the U.S. has 3,100 electric utilities. The late-2009 funding assistance will affect a very small percentage of those companies, even if you consider just the 210 investor-owned ones. Another reason: There are far too many parts and partners involved.

But will we see localized, incremental improvements? We should for projects, such as integrating sensors to aid in predictive maintenance, that affect operation and maintenance at the distribution level, and those improvements should be measurable. If the numbers—for things like number of equipment-related outages, length of outages, speed of responding to outages, and the like—don’t improve, customers and taxpayers (who are footing the federal dollar component of these projects, after all) will have good cause to complain.

Utilities know they have too much to lose if they blow SG projects, so there’s a bit of a stick involved with any SG endeavor that should encourage them to ensure that they keep their promises about the benefits that SG initiatives can deliver.

For one thing, customers in service areas where smart (also known as digital or advanced) meters are installed will see physical evidence of a change. Because those meters can communicate outage information to the utility, outages should be noticed and resolved faster. A portion of those customers will also be eligible to monitor real-time energy usage and may even be able to control their energy bill to some extent by taking advantage of time-of-use rates. Such capabilities are one aspect of what utilities call demand-side management.

Who Pays for the Smart Grid?

A July 2009 DOE report, “DOE Smart Grid System Report” lists cost as a challenge to SG implementation. Estimates “for just the electric utility advanced metering capability [range] up to $27 billion.” And “the Brattle Group estimates that it may take as much as $1.5 trillion to update the grid by 2030.”

Who pays, and how, for smart grid projects varies considerably by region, regulation environment, and type of project. A September 2009 DOE report titled “The Smart Grid Stakeholder Roundtable Group Perspectives” noted that “Some commercial customers and others are pursuing smart grid options outside the traditional utility rate structure, particularly in deregulated states.”

For at least initial efforts, some projects, like Xcel Energy’s SmartGridCity, have been funded by utilities and their vendor partners. However, Xcel—which did not apply for the first-round ARRA funding and was shut out when the DOE cancelled the second round, in which it had planned to participate—recently gained Public Utility Commission approval to recover $11 million in SmartGridCity costs vai rate increases. A Nov. 3 Denver Post story noted that “The city of Boulder, however, argued that because Xcel did not apply for a certificate of need from the utilities Commission, there is inadequate oversight of the project’s finances.”

As the New York Times noted, “While Boulder has many wealthy residents, the projected $100 million cost of the new wiring, ‘smart meters’ and other sophisticated gear being installed for the pilot project is a big number for most people to swallow. It works out to about $10,000 for each resident. In its pioneering haste to put together the nation’s first sizable smart grid project, Xcel neglected to qualify for the Department of Energy’s economic stimulus package.”

The financing of SG projects is likely to remain a touchy subject for most U.S. companies and customers for the foreseeable future.

California Led the Way

Several cities had already initiated major SG projects before the federal awards were announced. Three are profiled below. But first we need to acknowledge the role played by that enormous West Coast state that has been a fertile laboratory for technology innovations: California.

California and a few utilities in other West Coast states were the earliest and most active in deploying technologies that have SG implications. This is not to dismiss pilot and larger projects in other parts of the country (see sidebar), but economic, environmental, and political forces converged to make California more fertile ground for testing and wider-scale deployment of everything from distributed renewable generation to smart meters. State policy has helped spur activity, but the largest investor-owned utilities (Pacific Gas and Electric, Southern California Edison, and San Diego Gas and Electric) have also been more proactive than most of their peers in other parts of the country.

And in October, California became the first to pass a statewide SG law. Venturebeat.com and other SG followers noted that the bill, Senate Bill 17, passed with little fanfare. It requires the California Public Utilities Commission to develop a comprehensive SG plan by July 1, 2011. Utilities with more than 100,000 customers have to present their own detailed timelines by that deadline as well.

A Grassroots Move in Texas

In Austin, the Pecan Street Project, initiated in August 2009, seeks to develop “a hub of clean energy development in Austin—implementing pilot projects, working with innovative companies in the smart grid arena, and continually seeking new opportunities to deploy cutting-edge technologies in the real world.” The Pecan Street Project Inc. operates as a Texas nonprofit corporation. Phase 1 of this project “was a loosely organized, all-volunteer effort led by a Governance Group that included representatives from:

- City of Austin

- Austin Chamber of Commerce

- Austin Energy

- Austin Technology Incubator

- Environmental Defense Fund

- The University of Texas at Austin”

It appears that this effort is one in which true grassroots efforts are providing the impetus to develop a SG strategy. One of the group’s goals is to “design and implement an energy generation and management system that generates a power plant’s worth of power from clean sources within the city limits and delivers it over an advanced delivery system that allows for unprecedented customer energy management and conservation.” (A spokesperson for the project told POWER that a major report on “every aspect of the smart grid, from environmental performance to technology gap assessments; from economic development opportunities to the thorny questions of utility business models” had been delayed from October to a December release—too late to be covered in this story.)

The collaborative Pecan Street Project has elements in common with the “local power movement” and takes a big-picture infrastructure view that even includes water conservation.

Miami: Bidding to Be on the Leading Edge

In April 2009, the city of Miami announced the launch of a $200 million SG initiative that was promised to include every electricity connection in Miami-Dade County by 2011. Florida Power & Light (FPL) is partnering with General Electric, Cisco, and Silver Spring Networks. In contrast with the Pecan Street Project, this one depends on a more conventional utility-driven/government funds–primed model.

Energy Smart Miami, as the program is known, is, according to its website, “a groundbreaking energy initiative that proposes to use federal economic stimulus funds to help spur a $200 million investment in ‘Smart Grid’ technology and renewable energy in Miami over the next two years.” Washington must have been listening. In the October announcement of ARRA funds for SG projects, FPL was allocated $200,000,000 for a project whose total cost was pegged at $578,347,232.

Energy Smart Miami promises to “help Miami-Dade County consumers save money by giving them more choices over how they consume and conserve electrical power. It would also generate near-term demand for ‘green collar jobs’ to support its implementation, while further solidifying Miami’s national leadership in championing the responsible environmental practices needed to address the longer-term challenge of addressing climate change, which poses a significant threat to Florida and its coastal regions.”

The city claimed that the project “has the potential to be the most extensive and holistic Smart Grid implementation in the country.” It will begin with installation of more than a million smart meters.

Colorado’s SmartGridCity

In early September, Xcel Energy proclaimed that “SmartGridCity becomes first fully functioning smart city in the world.” Well, not exactly. The release went on to say that Xcel “has completed construction of the infrastructure and launched the remaining software to enable [my emphasis] all SmartGridCity operational functions. This step makes it the first fully functioning smart grid enabled city in the world.”

Specifically, “This launch ties together all the automated functions of SmartGridCity including: switching power through fully-automated substations; re-routing power around bottlenecked lines; detecting power outages and proactively identifying outage risks. The deployment integrated more than 20 applications, 95 new interfaces and more than 300 test cases.”

A month later, Ventyx, one of Xcel’s SGC partners, added that the project had “enabled 45,200 premises with broadband over powerline (BPL)”

“The SmartGridCity project also included automating three of four distribution substations, four computer-monitored power feeders, and another 23 feeders that are watched for voltage irregularities. Approximately 200 miles of fiber optic cable, 4,600 residential and small business transformers and nearly 16,000 smart meters are now connected to the smart grid system.”

In late 2009, Xcel was “qualifying” a limited number of households to participate in a pilot Home Energy Manager study in which, according to the SGC website, “Qualified homes may receive no cost installation and use of smart in-home devices that help manage energy use and environmental impact.”

To learn how some Boulder residents view the project, read “What Do Customers Expect from the Smart Grid?”

Hype, Hope, and Help

As with any new idea, those promoting it need to, well, promote it, which leads to inevitable hype. That’s not to say that the claims made for a smart grid are untrue. It’s just that (especially when they are made by politicians or utility executives or equipment and software vendors) they may raise the general public’s hope a bit too high too fast.

However, when they talk seriously within the industry, smart grid players and analysts are usually quite measured when speaking of the speed and success of SG activities.

For example, in this YouTube corporate video, Enrique Santacana, president and CEO of ABB (a major SG technology player) says North America is “not close” to having a smart grid, and he spells out the many elements that must be aligned before that happens.

And in an October Smart Grid webinar hosted by The Energy Daily (a sister publication of POWER), the message was similarly realistic. Carol Stimmel, research director at Boulder’s E Source, an energy information services company, noted that the smart grid is “not a thing.” There’s no “end point,” and “we’ll probably never be finished” she said. (Disclosure: I was formerly an editor at E Source.)

Stimmel identified what may be the largest potential brake on the ability of SG projects to deliver on their promises: Real success for the smart grid “depends on customer involvement.” However, an E Source study showed that as many as 90% of customers don’t understand the value of a smart grid.

Tom Scaramellino, founder and CEO of Efficiency 2.0 and trained presenter for Al Gore’s Climate Project, also emphasized the key role that consumers will play. He depicted the smart grid as consisting of four steps: meter, network, management, and consumer. (Efficiency 2.0 describes itself as “the premier energy efficiency and social software provider for utilities and other organizations seeking to engage residential and small business customers.”)

In Scaramellino’s view, the biggest long-term value of the smart grid (at least as he pitched it for the largely utility webinar audience) is “enhancing customer relationships” by enabling the addition of other sources of value besides the electricity.

As for the environmental benefits that are sometimes claimed for the smart grid, Scaramellino acknowledged that because load-shifting would likely move demand to evening hours, the result on the generation side is that you’re shifting from gas to coal, so a smarter grid may not necessarily be entirely environmentally beneficial.

He also observed that regulators are allowing SG investments because operational-side savings accrue—although, as the Xcel case mentioned above shows, timing can be critical. Because “the costs are fundamentally on the backs of customers,” there may be some “regulatory backlash” if utilities can’t demonstrate customer benefits over the next couple of years.

What’s Next?

If the state of the U.S. economy prompts another “stimulus package,” as some have speculated is possible, more federal money could be up for grabs later in 2010. In any case, instead of federal funds, public policy is likely to be the next lever that moves SG projects forward. As federal and/or state renewable standards and greenhouse gas limits become reality, every utility will have a different sort of incentive to minimize load increases, shift load from peak periods, and integrate renewable generation into its resource plan.

At least in the short term, we can expect more project announcements and more publicity about the biggest or smartest rollout of this or that SG technology. However, because much SG technology is still in its infancy, there will be someone coming along in a month or a week with a project that’s “bigger” or “smarter”—for years to come.

Another trend we may see concerns litigation involving smart grid technologies. Because the smart grid has many parts, supplied by many vendors, using relatively new technologies (especially compared with analog meters and existing T&D infrastructure elements), there are bound to be some growing pains.

Take for example, the case of a California man in the Central Valley who saw his monthly PG&E bill jump from about $200 to over $500. As the San Francisco Chronicle reported on Nov. 9, “The class-action suit, filed on Oct. 16 in Kern County Superior Court, alleges that the meters aren’t accurate and lead to overcharges that PG&E should be forced to refund. PG&E denies allegations that the meters are faulty. Similar complaints surfaced as the utility began installing smart meters in the San Francisco Bay area.

The utility has slowed deployment of the advanced meters, and the state PUC ordered PG&E to hire a third-party expert to “test and validate meter and billing accuracy.” After field testing of 1,100 meters showed they were operating correctly, the utility offered alternate explanations for the high bills that included customers dropping out of subsidy programs and bills with fees for overdue payments. Nevertheless, as this story was being finished, a web site affiliated with a Bakersfield television station reported that more than 500 customers had joined the class action lawsuit.

At the very least, this case highlights the critical importance of communication—the old-fashioned kind, not the smart meter kind.

If, as some sources claim, the PG&E bills increased both because of rate increases implemented to pay for the smart meter implementation and because of running power-hungry devices during high-priced parts of the day, then companies like PG&E need to do a better job of communicating clearly, honestly, and proactively about the cost implications of their smart grid–related actions.

—Gail Reitenbach, PhD is POWER’s managing editor.