The Department of Energy (DOE) has closed a $26.54 billion loan package—the largest single loan commitment in the agency’s history—with Southern Co. subsidiaries Georgia Power and Alabama Power to finance more than 16 GW of “firm” generation and more than 1,300 miles of transmission infrastructure and grid enhancement across the Southeast.

The transaction, announced Feb. 25 by the Office of Energy Dominance Financing (EDF), the DOE’s newly created lending arm, consists of two loan agreements totaling up to $26.54 billion—$22.4 billion to Georgia Power and about $4.1 billion to Alabama Power. The loans will carry an approximately 30-year term and remain available for draw through Sept. 15, 2033.

The financing will support roughly 5 GW of new natural gas generation, about 6 GW of nuclear uprates and license renewals, hydropower modernization, battery energy storage systems, and grid enhancement projects within the companies’ regulated service territories, the DOE said. “Once all funds are received through the program, the loans are estimated to reduce Southern Company’s interest expenses by over $300 million per year, helping expedite lower electricity costs for customers,” it said.

The ‘Largest Government Investment’ to Lower Power Costs, Increase Grid Reliability

The financing will be administered through DOE’s EDF, which is the rebranded successor to the department’s longstanding Loan Programs Office (LPO). EDF operates under the statutory authorities originally granted to DOE’s LPO through the Energy Policy Act of 2005. The office says it “possesses all authorities, receives all appropriations, and performs all requirements assigned to LPO.”

Through its Energy Dominance Financing Program—identified by DOE as Section 1706— EDF guarantees loans to projects that “add energy to the grid or enhance reliability.” Rather than issuing direct capital, the program provides a federal loan guarantee, effectively substituting the U.S. government’s credit backing for a portion of a borrower’s debt. That backing seeks to reduce borrowing costs, which utilities may then recover through regulated rate structures at lower financing expense than traditional market debt.

The EDF program took its current form when the One Big Beautiful Bill Act, signed July 4, 2025, replaced the Biden-era Energy Infrastructure Reinvestment Program under Section 1706 of the Energy Policy Act, moving to drop the prior requirement that projects reduce greenhouse gas emissions in favor of three new eligibility criteria. These include retooling or replacing energy infrastructure that has ceased operations; enabling operating infrastructure to increase capacity or output; or supporting the provision of “known or forecastable electric supply” to maintain or enhance grid reliability.

The DOE, notably, implemented the change through an Interim Final Rule on Oct. 28, 2025, which amended 10 C.F.R. Part 609. The $250 billion aggregate loan cap was carried over from the prior program. The OBBBA extended the deadline for issuing guarantees to Sept. 30, 2028, and appropriated an additional $1 billion for credit subsidy costs and administrative expenses.

Following a portfolio review that restructured or canceled more than $83 billion in Biden-era loan commitments, the DOE in January said EDF has more than $289 billion in available loan authority. In the final months of 2025, the office closed three loans totaling $4.1 billion: a guarantee supporting Constellation Energy’s restart of the Crane Clean Energy Center in Pennsylvania—the former Three Mile Island Unit 1—marking the first restart of a closed U.S. nuclear plant; a loan to an AEP subsidiary for transmission reconductoring and line rebuilds; and financing for Wabash Valley Resources in Indiana to repurpose a coal power plant for fertilizer production.

The Southern Co transaction, at $26.54 billion, notably eclipses the entire prior EDF loan portfolio in a single closing. On Wednesday, the DOE said the transaction aligns with President Trump’s January 20, 2025, executive order, “Unleashing American Energy,” which directed federal agencies to prioritize domestic energy production and grid reliability and would be funded under President Trump’s agenda-specific “Working Families Tax Cut.”

“Southern Company is among the first utilities working with the DOE and the Trump Administration to restore American energy dominance through common-sense energy investments. In 2025, Southern Company announced their plans to enact multiyear rate freezes,” the DOE noted.

However, it also noted: “DOE remains committed to setting a new standard for government energy financing, ensuring that loans deliver affordable, reliable, and secure energy for the American people.”

Why Southern Co. Was Chosen: Vertically Integrated Bet

Southern Co. in a statement on Wednesday said its “vertically integrated, state-regulated model provides an orderly and transparent framework for working with regulators to deploy essential energy infrastructure investments—like those supported by the EDF loans for the benefit of customers.”

“These investments will support the extraordinary and transformative projected growth we’re seeing across our company,” noted Chris Womack, Southern Co. chairman, president, and CEO. “At Southern Company, we are focused on serving growth while maintaining rate stability and driving long-term savings for customers.”

During its fourth-quarter earnings call on Feb. 19—six days before the federal announcement—the company disclosed an $81 billion capital investment plan for 2026 through 2030. That represents an $18 billion—or roughly 30%—increase from its prior five-year forecast. CFO David Poroch told analysts the plan is “$81 billion over the next 5 years, 95% of which is at our state-regulated utilities,” and that it “supports projected long-term state-regulated average annual rate base growth of approximately 9%.”

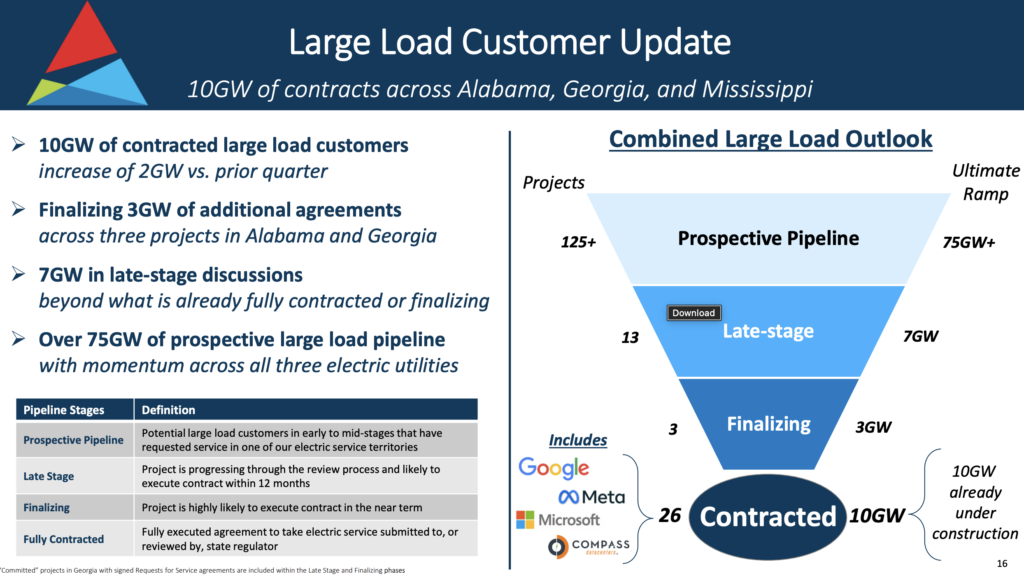

That plan rests on 10 GW of fully executed large-load service agreements and a prospective pipeline that grew from 50 GW to over 75 GW versus the 2024 fourth quarter. The company pointed to 26 fully signed contracts representing 10 GW of committed load—nearly all currently under construction. Those projects “include load ramps totaling 8 GW by the end of our 5-year planning horizon, ultimately ramping up to 10 gigawatts beyond 2030,” Poroch noted.

Poroch emphasized that Southern Co.’s regulatory construct enables “bilaterally negotiated contracts for large load customers rather than the use of a standard tariff,” which provides flexibility to price service “in a manner designed to more than cover the incremental cost to serve them.” Contracts carry minimum terms of at least 15 years for data centers, he said. Poroch described the pricing provisions as “fixed or minimum bill provisions similar to take-or-pay structures” designed to cover “at least 100% of the annual incremental cost to serve, including the necessary generation and transmission investments, incremental O&M, and our cost of capital,” he explained. Each agreement also includes “termination payments tied to the incremental cost to serve over the life of the remaining contract” and “significant collateral requirements tied to the termination payments.”

Southern Co.’s weather-normalized retail electricity sales grew 1.7% in 2025—more than double the cumulative growth of the prior decade, he said. Commercial sales led by data center customers expanded 17% year-over-year for the second consecutive year. In addition, he projected average annual retail electricity sales growth of 10% from 2026 through 2030, up 2 percentage points from prior guidance.

Outcomes are already visible in the rate structure, Poroch noted. “Georgia Power and Alabama Power, our two largest subsidiaries, worked constructively last year with each of their public service commissions to implement multiyear rate stabilization agreements.” In July 2025, the Georgia Public Service Commission (PSC) froze the utility’s rates through at least the end of 2028, while Alabama Power committed to keep customer rates steady through 2027. Poroch added that in December, “as a part of its certification process for new generation, Georgia Power was able to quantify at least approximately $1.7 billion of benefits that will help to lower cost to serve existing customers from 2029 through 2031.” Georgia Power also filed that week for storm and fuel cost recoveries that, if approved, “would collectively lower rates for customers starting this summer.”

Southern Co., meanwhile, is also tracking roughly 3 GW of additional load that Poroch described as in final counterparty review and “highly likely to progress to an executed contract in the near term”—contracts he confirmed are “baked into our forecast today,” though their associated “ramp rates… move out beyond our planning horizon.”

Beyond the five-year base, Alabama Power and Georgia Power have launched or are preparing generation [request for proposals (RFP)] processes targeting resources for 2031 through 2033. Southern Power, its competitive generation subsidiary, is notably evaluating capacity uprates of up to 700 MW on its existing gas fleet—Womack said those could come online “as soon as 2029″—and new gas development at six brownfield sites in the Southeast. The Southern Natural Gas pipeline system is evaluating a fifth expansion project jointly owned with Kinder Morgan.

For now, all necessary equipment—including turbines, battery systems, solar components, and transmission materials—has been physically reserved for projects through 2029, the company’s earnings presentation shows. Turnkey fixed-price engineering, procurement, and construction (EPC) agreements are also in place for externally contracted work. The presentation indicates the company’s internal construction team is self-performing the McIntosh Unit 12 combined-cycle plant and the associated McIntosh BESS project.

Loan to Reduce Southern Co.’s Interest Expenses by Over $300M per Year

However, speaking last week, Womack said Southern Co.’s regulated model depends on coordinating capital investment with customer growth and regulatory cost recovery. “The orderly, transparent, and constructive regulatory processes in which our utilities operate are designed to reliably and sustainably serve growth while helping to ensure that all customers benefit from that growth. And this design is proving effective.”

The historic $26.5 billion federal loan package, notably, arrives as Southern Co. faces significant financing demands. To fund the $81 billion capital program without straining its credit ratings—a prerequisite for maintaining investor confidence and keeping borrowing costs low—the company has been steadily locking in the equity capital it needs. Southern Co. has already addressed roughly $9 billion of that equity requirement through a combination of stock sales and convertible securities, including $4 billion priced through its at-the-market program with forward contracts settling through 2026 and 2027 and $2 billion in equity units that will convert to shares in 2028. Poroch told analysts that “nearly all $9 billion of the equity we have already addressed is expected to be issued or settled by 2028,” leaving a remaining need of “approximately $2 billion through 2030.”

The DOE loan may serve to reduce pressure on that financing plan. By cutting more than $300 million in annual interest expenses, the approach could increase the cash Southern Co. generates relative to its outstanding debt (a core metric credit agencies use to assess financial health). The company has committed to sustaining that ratio above 15% through 2027 and improving it to approximately 17% by 2029. The loan’s structure may also provide flexibility, given that Southern Co. can draw funds incrementally as individual projects reach financial close. Those draws are “subject to satisfaction of conditions and may be made through September 15, 2033”—a seven-year drawdown window—the company said Wednesday.

Pressed by a Barclays analyst on whether the company’s escalating guidance reflected genuine contract visibility or optimism, Womack was unambiguous. “You know us. You know how disciplined we are, you know how thoughtful we are in terms of setting expectations,” he said. “And so as we look forward in terms of the execution around these 10 GW of projects and what we see, the 3 GW in final stages, the 7 GW in late stages, and looking at the pipeline of some 75 GW, I mean, that gave us confidence to make the changes and the adjustments that we’ve announced today.”

—Sonal Patel is a POWER senior editor (@sonalcpatel, @POWERmagazine).