A week after the Department of Energy (DOE) proposed a rule to bolster uneconomic coal and nuclear generators in competitive power markets, Luminant announced that an “unprecedented low power price environment” will force it to retire a 1.9-GW coal-fired power plant operating in the Texas market. The plant’s economic woes suggest a larger swath of Texas baseload generators may face a similar fate.

Luminant will take its Monticello Power Plant in Titus County, Texas, offline in January 2018 because low prices within the Texas competitive wholesale bulk-power market managed by the Electric Reliability Council of Texas (ERCOT) have “profoundly impacted its operating revenues and no longer [support] continued investment,” said Curt Morgan, president and CEO of Vistra Energy, Luminant’s parent company, on October 6.

Along with Monticello, Vistra on October 13 also announced plans to shutter two other massive coal-fired plants in Texas—the 1.1-GW Sandow Power Plant (which includes a 2009-built unit) and the 1.2-GW Big Brown plant—in early 2018.

Luminant said that it filed a notice with ERCOT to retire Monticello, a process that will trigger a reliability review. “If ERCOT determines the units are not needed for reliability following this 60-day review, Luminant expects to stop plant operations on Jan. 4, 2018,” it said.

The coal plant’s closure will affect about 200 company employees. Financially, Vistra expects to take a hit of between $20 million to $25 million, a figure that includes employee-related severance costs and non-cash charges for materials inventory and the acceleration efforts to reclaim the plant’s mines, which were shuttered in the spring of 2016.

Spotlight on Pricing Woes in ERCOT

The Monticello Steam Electric Station, which was a POWER magazine Top Plant nearly a decade ago, comprises three supercritical units. Monticello Units 1 and 2 are each rated at 565 MW and are powered by a Combustion Engineering boiler and a Westinghouse turbine-generator. They came online in 1974 and 1976, respectively. Unit 3, rated at 750 MW and powered by a Babcock & Wilcox boiler and a turbine-generator from General Electric, went online in 1978.

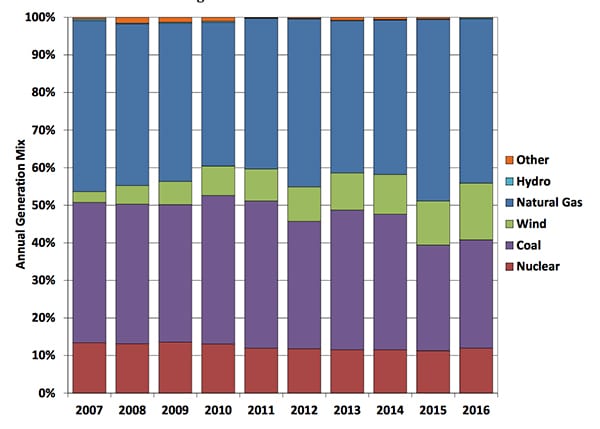

The 1.9-GW plant made up a fraction of the 101 TWh ERCOT’s coal plants generated in 2016. Coal generation made up 28.8% of ERCOT’s total generation mix, which has been shrinking as more natural gas plants and wind farms are added to the grid. In 2016, gas’ share was 43.7%, nuclear generated 12%, and wind generated 15.1% (soaring from just 3% in 2007).

- ERCOT’s annual generation mix. Courtesy: Potomac Economics

But Monticello’s economic worries aren’t unique in the Texas wholesale market, which got its start around 1995. According to the 2016 State of the Market Report issued in May by Potomac Economics, ERCOT’s independent market monitor, economic pressure is clearly mounting on ERCOT’s existing coal and nuclear units because their non-shortage prices—the vast majority of net revenues they earn—have been “substantially affected by prevailing natural gas prices.”

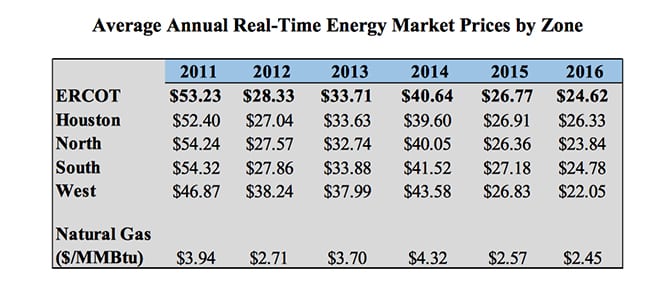

Other industry observers point out, however, that the overarching issue is how drastically wholesale power prices have fallen in ERCOT—the entity that manages 90% of Texas’ electric load, three-quarters of which is in the competitive market. In 2014, for example, while prices varied by zone across the market owing to congestion costs, the average annual real-time energy market price hovered at $40.64/MWh. In 2016, that average fell to $24.62/MWh—an all-time record low in ERCOT (Figure 1). In the first eight months of 2017, meanwhile, prices averaged $28.64/MWh.

2. The price drift. In its “2016 State of the Market Report” published earlier this year, Potomac Economics, ERCOT’s independent market monitor, said the average annual real-time energy market price decline is largely pegged to “lower natural gas prices and surplus supply.” Courtesy: Potomac Economics

2. The price drift. In its “2016 State of the Market Report” published earlier this year, Potomac Economics, ERCOT’s independent market monitor, said the average annual real-time energy market price decline is largely pegged to “lower natural gas prices and surplus supply.” Courtesy: Potomac Economics

As some experts note, falling wholesale power prices are indicative that competition is functioning as it should. ERCOT’s unique energy-only market is designed so that net revenues from the real-time energy and ancillary services markets alone provide the economic signals that inform generator decisions to invest in new generation or retire existing generation. The market was also designed so that generators should shoulder the risk of building new power plants, and that new power plants produce more electricity per unit of fuel, noted the Association of Electric Companies in Texas.

ERCOT has said that wholesale energy prices have fallen so quickly partly because of the efficiency of its competitive market wholesale market, but they also resulted primarily from “very low natural gas prices,” averaging $2.45/MMBtu, as well as an influx of wind power production. Since 2009, ERCOT’s wind capacity has nearly doubled to more than 17,000 MW and an additional 5 GW may connect to the grid this year based on existing transmission agreements.

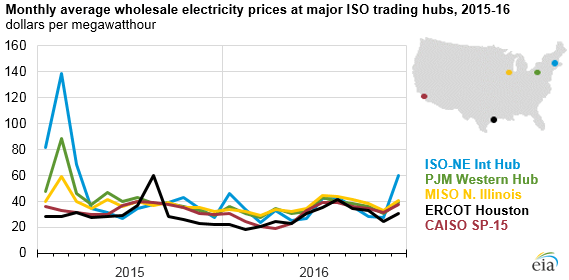

3. How ERCOT compares. Average wholesale power prices at major trading hubs across the U.S. were significantly lower in 2016 than in 2015. This was primarily driven by the sustained low cost of natural gas, a fuel that often determines the marginal generation cost in most power markets. Source: EIA/SNL Energy

Yet, the depressed power prices have left even the most efficient gas generators with sparse profit margins. This May, Panda Temple Power, a private equity merchant power developer that in 2014 put online a 758-MW gas-fired combined cycle power plant in Temple, Texas, filed for bankruptcy. The Dallas-based company is now suing ERCOT for its plight.

In a declaration filed in Delaware bankruptcy court this April, the company claimed that capacity, demand, and reserves (CDR) reports released by ERCOT in 2011 and 2012 projected a supply shortfall, which led Panda Power to invest in Temple I and other plants. However, during 2015 and 2016, the company began to experience revenue, cash flow, and liquidity challenges “due in large part to deteriorating market conditions within ERCOT.” The company alleges that after Temple I came online, ERCOT changed its forecasting methodology and inputs to depict an oversupply, which has had the effect of depressing the price of power in the spot and forward markets.

“The lawsuit is based on a misunderstanding of the purpose of ERCOT’s [CDR] reports, how the reports are prepared in accordance with the methodology in the ERCOT Protocols, and the open and public stakeholder discussion ERCOT goes through before changing components of the CDR,” ERCOT told POWER on October 12. “ERCOT will continue to vigorously defend its position as it responds to the lawsuit.”

Last week, meanwhile, Talen Energy notified ERCOT that it would retire the 1974-built Unit 1 at the 964-MW gas-fired Barney Davis power plant near Corpus Christi. Talen spokesperson Todd Martin told POWER that the unit is “one of the smaller, older units in the fleet and the company has decided to invest its resources into assets that generate greater customer value and financial return.”

Monticello Economically Hurting for Years

For Vistra Energy’s head, Curt Morgan, the decision to retire Monticello was purely economic, and it was made after a year of “careful analysis.” Vistra Energy—formerly known as TCEH Corp.—in November 2016 changed its name after it emerged from Chapter 11 as a standalone company through a tax-free spinoff from Energy Future Holdings Corp. At the time, Morgan said the rebranding was intended to capture the “vision of an energy company preparing for the future,” while still taking into account its 130-year heritage of serving Texans.

But at Monticello the situation has been dismal for years. “The economics of this plant no longer make it a viable option for our fleet,” explained Vistra Energy spokesperson Allan Koenig on October 10, though he didn’t respond to questions about what the company has done to cut costs. “Over the last few years, wholesale power prices have continued to decline, causing this facility to fall below breakeven on a sustained basis.”

Luminant hinted it would shutter two units at the massive coal plant as early as 2011 if forced to abide with the Environmental Protection Agency’s (EPA) Cross State Air Pollution Rule, which required generators to dramatically reduce sulfur dioxide and nitrogen oxide emissions from power plants. Koenig told POWER that “For the past two or three years, the plant has been running in a seasonal operations status, but is not currently in that status.”

Koenig declined to comment on the status of Luminant’s other Texas coal plants, including the 1970s-era Big Brown and Martin Lake plants, as well as its 2.3-GW Comanche Peak nuclear power plant. (On October 13, days after this article was published, Vistra announced it would shutter the 1.2-GW Big Brown plant as well as the 1.1-GW Sandow Power Plant—which includes a 2009-built unit—in early 2018.) “We do not report a unit-by-unit economic view of any of our fleet outside of the normal [U.S. Security and Exchange Commission] reporting periods,” he said. If ERCOT told Luminant that Monticello or other plants were necessary for reliability, it would “enter into a Reliability Must Run agreement with ERCOT,” he said.

While Koenig also did not respond to questions about whether anything can be done on a market basis to aid uneconomic baseload power plants, Vistra’s announcement to shutter Monticello came a week after the DOE proposed its “Grid Resiliency Pricing Rule,” a controversial measure that directs the Federal Energy Regulatory Commission (FERC)—an independent regulatory government agency that is officially organized as part of the DOE—to exercise its authority under sections 205 and 206 of the Federal Power Act and require that independent system operators (ISOs) and regional transmission organizations (RTOs) “establish just and reasonable rates for wholesale electricity sales” for power plants that show “reliability and resiliency attributes.”

The rule has divided the power sector, pitting coal and nuclear generators against a slew of other power entities, including natural gas and renewables generators, competitive market participants, and regulatory bodies. FERC has begun accepting comment on the rule in Docket No. RM18-1—but it intends to close comment on October 23—and a number of market stakeholders have already filed comments, or sought to intervene.

Luminant is watching FERC’s efforts to enter in a rulemaking “with interest,” Koenig said. He noted that “there are many uncertainties facing generators, and this may ultimately be of assistance in some markets.” For the most part, however, the company is “against government subsidies and intervention into competitive markets,” he said. But even if finalized, it is unclear whether the rule would benefit generators in ERCOT as the ISO does not fall under FERC’s jurisdiction, he said.

ERCOT Coal, Nuclear Plants Economically Bleeding

ERCOT, which is conducting a study to determine whether Monticello’s removal from the grid poses a concern regarding transmission system reliability in that area, told POWER on October 12 that from a systemwide resource adequacy perspective, based on current information from market participants, it expects to have sufficient generation capacity available to serve expected demand over the next several years.

“We also have a number of tools to maintain overall system reliability in a wide range of scenarios,” said Robbie Searcy, an ERCOT spokesperson. “Investment and interest in new generation continues in the ERCOT market.”

In fact, she noted, Luminant has added two new combined-cycle power plants to its fleet within the past two years.

According to the ISO’s market monitor Potomac Economics, however, the economic standing of massive coal and nuclear power plants deserves ERCOT’s attention because their closure may adversely impact reliability.

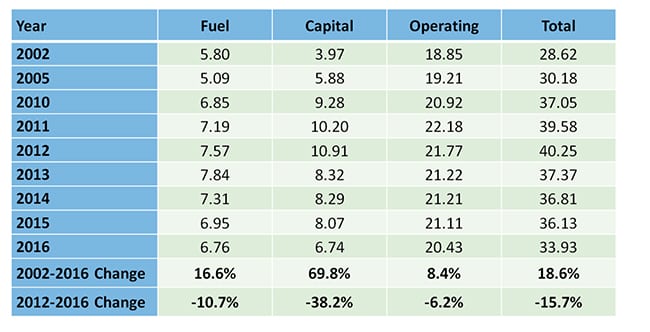

Potomac noted that generation-weighted average price per MWh for the four nuclear units in ERCOT—about 5 GW of capacity—was only $21.46/MWh in 2016 (falling from $24.56/MWh in 2015). If—as the Nuclear Energy Institute suggested in an April 2017 white paper—these plants’ total fuel and operating costs mirrored other nuclear units across the U.S., which averaged $27.17/MWh in 2016 (Figure 4), it is likely that these units were unprofitable based on fuel, operating, and maintenance costs alone, it said.

“Although not profitable on a stand-alone basis, the nuclear units have substantial option value for the owners because they ensure that their cost of serving their load will not rise substantially if natural gas prices increase. Nonetheless, the economic pressure on these units does potentially raise a resource adequacy issue that will need to be monitored,” Potomac added.

4. U.S. nuclear plant costs (2016 $/MWh). According to a recent white paper from the Nuclear Energy Institute, in 2016, the average total generating cost—factoring in fuel, operating and capital costs—for nuclear energy was $33.93/MWh. The average annual real-time energy market price in ERCOT in 2016 was $24.62/MWh. Courtesy: NEI, Nuclear Costs in Context (August 2017)

Meanwhile, the generation-weighted price of all coal and lignite units in ERCOT during 2016 was $23.98 per MWh. Potomac’s 2016 market survey report notes that, although specific unit costs may vary, index prices for Powder River Basin coal delivered to ERCOT were approximately $2.50/MMBtu in 2016, a decrease from approximately $2.60 per MMBtu in 2015. For the past two years, costs for delivered costs in ERCOT has still been about $0.03 to $0.05/MMBtu higher than natural gas prices at the Houston Ship Channel, it said.

“Given that the coal units generally have higher heat rates and more expensive non-fuel operations and maintenance costs, they have been losing market share to natural gas. As with nuclear units, it appears that coal units were likely not profitable in ERCOT during 2016,” it noted.

The implications on ERCOT’s reliability efforts could be profound, it said. The bulk of ERCOT’s coal fleet is more than 30 years old, and the retirement or suspension of “some of these units” could cause “ERCOT’s capacity margin to fall to unreliable levels more quickly than anticipated,” it added.

As significantly, the market monitor also expressed concerns that “relatively infrequent shortage pricing” may hinder announced generation from coming online as planned, and its report concludes that ERCOT’s planning reserve margins, which range between 20.2% and 19% from 2018 to 2021, may be overestimated.

ERCOT to Bank on Natural Gas, Wind, and Solar

ERCOT’s Searcy confirmed that the grid entity “announces and accounts for retirement notices as they are received,” because generators make decisions about the future of their plants based on factors unique to their companies.

But ERCOT isn’t alarmed by the potential mass retirements.”The ERCOT market has seen cycles of retirements and new investments in the past, so these types of shifts are not without precedent,” she said.

Asked about ERCOT’s current market outlook for coal and nuclear generation, Searcy pointed out that the ERCOT market “provides a diverse portfolio of resources to support reliability.”

However, she noted, all new generation in the Texas pipeline is natural gas, solar, or wind. “As of Sept. 30, more than 21,000 MW of potential utility-scale solar generation was under study, along with more than 20,000 MW of potential wind generation and about 4,000 MW of potential gas-fired generation resources. This is in addition to existing interconnection agreements for 10,511 MW of new gas-fired generation, 2,050 MW of new solar and 8,655 MW of new wind,” she said.

For now, ERCOT has an adequate reserve margin of 16.9% for 2017, which exceeds the 13.75% target. That’s a significant improvement from dismal reserve margin projections from only six years ago, when ERCOT declared several emergencies to reduce electric demand, and stricken with capacity shortages, forecast a negative margin by 2022. The grid entity, which has neither a capacity market nor a requirement that generators build or purchase reserve capacity to meet unexpected supply shortages, has since taken a number of price-related actions to encourage investment in generation.

In 2014, for example, the Public Utility Commission of Texas in 2014 approved an Operating Reserve Demand Curve (ORDC), which raises wholesale market prices in the real-time energy market when operating reserves decrease to established targets, as well as an incremental increase in the systemwide offer cap from $3,000 to $9,000 per MWh. “Additionally, ERCOT has taken steps to improve its load forecasting methodology, which affects expectations for future planning reserve margins,” Searcy said.

Yet, looking into the future, all resources suggest that ERCOT’s oversupplied market will remain saturated with natural gas, wind, and solar. The entity’s most recent CDR report released in May shows more than 10,000 MW of planned resources with interconnection agreements will begin operations by summer 2018. That includes more than 3,500 MW of new gas-fired generation, with additional resources planned in 2019 and beyond.

The short-term, too, may offer no relief to coal and nuclear generators. As it released its Seasonal Assessment of Resource Adequacy for the fall season this September, for example, ERCOT noted that nearly 86 GW of total generation resources are currently available for peak demand. Significantly, it said, it would enter the fall season with about 3 GW of new generation capacity since a preliminary assessment was released in May.

That includes two gas-fired combined cycle units totaling 2.2 GW. Another 1.5 GW will be added by the end of the year—837 MW of which will be new wind and solar.

—Sonal Patel is a POWER associate editor (@sonalcpatel, @POWERmagazine)

Updated on October 13: Adds ERCOT’s comments