POWER breaks down the top insights from Data Center POWER eXchange, its unique one-day summit curated by POWER’s editorial team and convened to examine the collision between accelerating data center load and tightening grid constraints.

The rise of artificial intelligence is poised to create the fastest, largest, and most concentrated surge of electricity demand in modern U.S. history. While load is doubling in some regions and transmission timelines have frozen development in others, the power sector is bracing for a structural mismatch between the speed of digital expansion and the pace at which the grid can be planned, permitted, and built.

POWER, which has been watching this collision gather speed in its reporting on load forecasts, interconnection backlogs, transformer scarcity, and the rise of data-center co-location, in January set out to cultivate a summit that reflected the actual mechanics of the problem. The objective was fundamental: bring utilities, hyperscalers, grid operators, regulators, financiers, and project developers into the same room and, bolstered by the facts, encourage a project-level discussion about what it now takes to deliver power at the scale AI demands.

From the outset, the inaugural Data Center POWER eXchange (DPX), which took place in Denver on October 28, was framed by core questions: How do you build firm capacity fast enough? Who pays for the infrastructure? How do you maintain reliability when multi-gigawatt requests outrun planning cycles? What happens to ratepayers? How do projects move when transformers and substations face multi-year delays? And where does community acceptance fit when the siting footprint keeps expanding?

Guided by a cross-sector advisory board, the exclusive editorially curated program was built around the full lifecycle of a modern infrastructure project—site selection, development and permitting, financing and on-site generation, operations, and forward planning—so every panel confronted the same constraints: long-lead equipment shortages, transmission limits, unstable timelines, cost-allocation disputes, and the widening gap between hyperscaler speed and utility planning cycles.

Christie Warns of a Dual Crisis: Reliability Strain and Rising Customer Costs

Mark Christie, the former chair of the Federal Energy Regulatory Commission (FERC), opened the day by grounding reliability in plain terms. “When Americans talk about reliability, what they mean is, I want power 24/7 365,” he said. “That’s what Americans expect.” On the cost side, he pointed to an accelerating trend. “EIA just came out yesterday and said that year over year, prices increases in power bills for consumers was 6% over the last year. That’s way over the rate of inflation,” he said. “And if you look at the last five years, we’ve had more increases in power bills over the last five years than the previous 25.”

In This Issue

Full issueUninterrupted service combined with rising monthly bills creates the political tension Christie believes the sector now faces. He invoked Alexis de Tocqueville’s warning to the French Parliament on the eve of 1848: “We are all sleeping on a volcano.” His own assessment of the present moment: “I think rising power prices are a political volcano that’s on the verge of exploding.”

According to Christie, a “dual crisis” now confronts the sector. Supply-side, the U.S. has been “retiring prematurely too many dispatchable generating units, particularly coal,” he said. “We have not been replacing coal with equivalent dispatchable generation. We simply have not been doing that.” In regions such as PJM that depend on capacity and energy markets to finance new generation, the result has been sustained erosion of firm supply.

Demand-side, meanwhile, the curve is being reshaped by a narrow band of very large customers. “The increase in load, marginally driven by marginal customers, micro-scale customers, has increased load forecasts,” Christie said. In PJM, “the load forecasts become the demand curve, and the demand curve becomes the single biggest determinant of the prices in the PJM capacity market.” His conclusion: “Load increases without generation. Something’s got to give.”

Christie, speaking from 17 years as chairman of the Virginia State Corporation Commission and five years as a FERC commissioner, narrowed his concerns to three regulatory questions. “How are we going to finance that new generation? Is it going to be a rate-based mechanism? Is it going to be capacity markets? Is it going to be energy-only markets?” he asked. He then clarified the limits of federal authority, leveraging a distinction sharpened by his dual experience navigating both state and federal energy policy. “People frequently say, ‘Well, what’s FERC going to do to build generation? Why doesn’t FERC just order more generation?’ Well, guess what? FERC doesn’t order generation to be built.” States, he noted, issue certificates of public convenience and necessity and approve integrated resource plans.

Finally, he asked: “What is the best regulatory framework at the state level to get generation built and to serve reliability? Is it the ‘deregulated’ model that we see in many PJM states, or is it a vertically integrated model where generation can be financed through rate base?”

Cost allocation, Christie argued, is the underlying constraint. “How do you allocate the cost, who pays?” he said. And affordability sets the boundary for any solution. “We have to do this while making sure that customers can actually afford to pay that monthly power bill, and that electricity doesn’t become a luxury item that only a few can afford, because if that day happens, I think the political explosion on that is just going to be breathtaking in its consequences.”

‘Ground Zero’: Dominion CEO’s View of the AI Load Surge

Presenting a crucial power-sector perspective, Robert Blue, chairman and CEO of Dominion Energy, in his keynote, revealed what AI-era load growth looks like within the vertically integrated utility that Christie had just described as “ground zero of the data center revolution.”

“Our mission is to deliver the reliable, affordable, increasingly clean energy that powers our customers every day,” Blue said. “And data centers make up a large and growing share of our customer base.” A decade ago, Dominion Energy Virginia was “connecting 100 to 200 MW of data center capacity a year.” Half a decade ago, it was “connecting on average, 600 MW of data [center] capacity per year.” For the last three years, he said, “we have connected about 1 GW of data center capacity per year. But it’s not just that data center load is growing. The rate of overall growth is increasing as well,” he said.

Blue first “level set” on the two pillars Christie had just highlighted. Dominion’s system, he said, delivers 99.98% reliability “exclusive of major storms”—a standard the company “can never compromise on.” On affordability, he noted that Dominion’s residential rates “have long been below the national average and comparable to or below relevant regional averages” and that they have “been consistently below the overall rate of inflation for decades.” He pointed to a recent study that found rates in Virginia tracked below inflation from 2019 to 2025 “even as growth has accelerated to record levels and the Commonwealth has become the home to the largest array of data centers on the planet.”

To “jump to 2025,” Blue said, “data centers now account for 27% of Dominion Energy Virginia’s sales.” Most of that load is concentrated in Northern Virginia’s Data Center Alley, “where it’s estimated that 70% of the world’s internet traffic passes through. The data center market there is bigger than the next five U.S. markets combined. That’s the reality on the ground today.”

The forward curve has shifted just as sharply. Back in 2021, PJM “was projecting the rate of growth for our summer peak to be around a half of a percent.” By 2023, that figure was 5%. “And today, PJM is projecting 6.3% annual growth. We expect demand to double by 2039 driven in no small part by the expansion of the data center industry.” These are forecasts, he stressed, but “we’re seeing the growth happen in real time. Our top 10 all-time peaks in customer demand occurred this year, and 24 of our 25 all-time summer peaks have occurred in the last two years.”

All of this will require “some significant adjustments,” Blue said. “To start with, we need an all of the above energy policy.” Politicians sometimes embrace that phrase “with an asterisk listing exceptions,” but Dominion’s position is different, he said. “We need all of the above period. More natural gas, more solar, more wind, more storage, and even potentially, more nuclear generation. That’s the only way we can hope to meet rapidly rising demand.” The company’s latest long-term plan for Dominion Energy Virginia “includes more than 33 GW of new power generation over the next 20 years from all of the above sources.”

On the transmission side, Dominion invested $2.1 billion last year—about 18% more than the year before—and is “looking at greater than $2.8 billion” in annual transmission capital spending starting in 2027 “because we need a way to get all the new power to all of the new customers, while ensuring costs are fairly allocated,” he said.

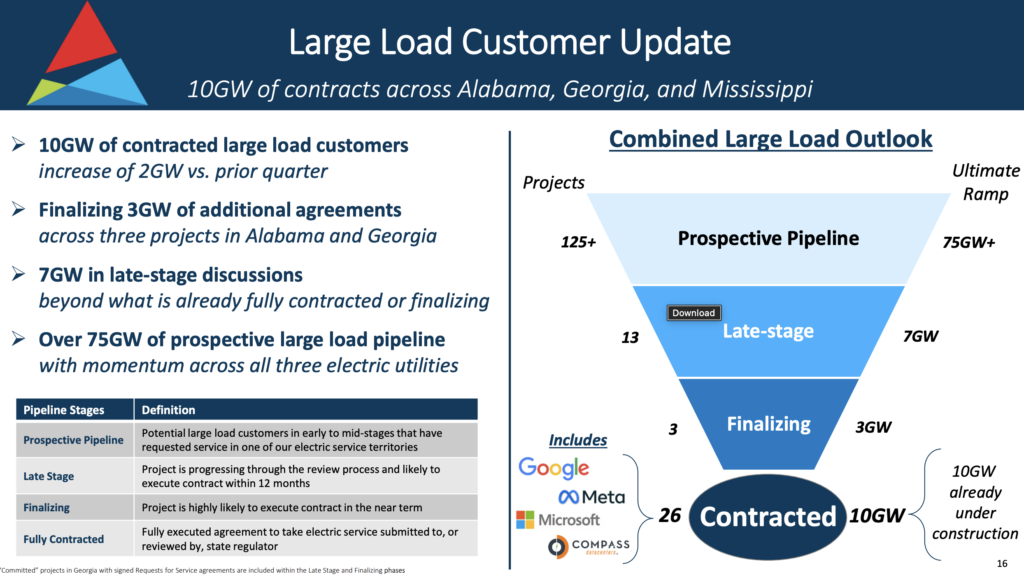

During Dominion’s third-quarter earnings call at the end of October, Blue notably laid out how much of that growth is already under contract. “We now have approximately 47 GW in various stages of contracting as of September 2025, which compares to around 40 GW as of December 2024, an increase of 7 GW or 17%,” he told investors. Of that, “about 9 GW” are in construction-stage agreements, and “we now have nearly 10 GW in Electric Service Agreements” committing customers to multi-year ramp schedules. The energization dates for those delivery points, for now, “stretch through 2031,” he said.

Executive Dialogue: Hyperscalers Are Pressing for a Grid ‘Facelift’

While Blue detailed the operational pressures on a utility absorbing unprecedented load, the succeeding executive dialogue exposed a complementary strain on hyperscalers. Drawing on her decade of experience leading Google’s global energy strategy and now advising technology clients as founder and CEO of Envision Energy Advisors, Caroline Golin, PhD, described how quickly planning scenarios have shifted for the digital sector.

“I’ll be honest when I say the majority of us just didn’t believe it, like because I think the majority of our utility partners just didn’t believe it,” she said. “We were sort of in a situation [of] the stages of grief, you know, like disbelief, fear, paralysis. You know, we’ve all sort of moved through that, and we didn’t believe it, largely because the data center industry [has] had sort of these erratic projections in the past, and we’ve seen these cycles of boom, and in large part, that’s—as most of you all know—because our demand projections really chase the customer cycle, right?”

“Between two and three years ago, we started to see this huge uptake. I mean, the hockey stick, right?” she said, referencing a curve that stays relatively flat before rising almost vertically. “And I personally sat my team down, you know, hundreds of people in Google, and we said, we’re probably going to make some bad decisions over the next couple of years, figuring this out. We need to be able to keep our focus and be able to see what is the forest through the trees.” As someone who “frankly, didn’t really believe that this growth was real for the first year and a half,” she told the room, “I now firmly believe it is real.”

For Golin, the more important question is what kind of system the capital surge will build. She argued that treating AI-era demand as a passing “bubble” would lock regulators and utilities into “the same cycles” and “the same business models” they have used for decades, instead of asking “what do we want the catalyst of these 350–400 billion [dollars] … flow to the U.S. of capital to do to our system.” She said the U.S. grid, “while reliable, is in massive need of a facelift.”

Dominion, she emphasized, “is not one of these,” but “many, many of the utilities throughout the U.S. have no idea where their load is. They actually have no idea how their distribution system is operating. They have no idea how to take load off their distribution system and redirect it to the transmission system. And that’s because they really haven’t had to.”

That complacency is no longer tenable, she argued. Golin called the present moment “a great forcing function” for investing in “grid-enhancing technologies” and “behind-the-meter” and storage solutions that make the system more flexible, interoperable, and transparent. She also pointed to studies suggesting the U.S. system has “50, 60, 70 GW of latent capacity in the system, but we have no idea how to harness it … because we’ve never been incentivized to.”

“The crunch is the next three years,” she said. “We’re in an AI training race globally. If we don’t meet the next three to four years of need, that training will go someplace else, or it will get beaten by other global actors that are just going to train their models through whatever means necessary. So we have this little arc. You can’t build natural gas, you can’t get the transformers, you can’t build the poles and wires fast enough for the next three years. And we can’t build the wind and solar, frankly, fast enough for the next three years either. So we as a grid are going to have to figure out how we can achieve this, and that’s going to come down to, I think, a lot of different business models than we’ve ever seen before.”

Rather than arguing over “deregulated versus regulated” in the abstract, Golin said, the priority should be “get[ting] the market signals right.” A regulated utility, she argued, “can do it just as well as anyone” if it is “incentivized towards the right solutions,” including partnerships that bring in third-party and hyperscaler capital to modernize the grid and “set it up for electric vehicle transport,” industrial electrification, and a “smart home future” that will persist long after the current wave of AI buildout.

—Sonal Patel is a POWER senior editor (@sonalcpatel, @POWERmagazine).

Editor’s Note: This is Part 1 of POWER’s ongoing coverage of the Data Center POWER eXchange (DPX), held October 28, 2025, in Denver. Subsequent articles will examine grid modernization and interconnection bottlenecks, on-site power and advanced solutions, operational risk management, and state regulatory frameworks. Read the full series at powermag.com.