Decarbonization is becoming firmly entrenched in utility business strategies to address risks and opportunities posed by climate change. But setting out a sound plan amid so many uncertainties poses a number of challenges.

The much-publicized and often bitter politicking about climate change in the U.S. would have you believe that decarbonization is still at a soft, latent stage—and that the power sector, which is often cited as the largest source of CO2 emissions, is dragging its feet as it awaits a concrete policy direction.

|

|

1. The International Energy Agency (IEA) in March said while electricity demand continued to rise over the past few years, carbon intensity for the largest economies has continued to fall. However, while the agency expects decarbonization will continue at the same pace through 2040, despite improvements, large increases in electricity demand combined with a power generation mix that’s 50% fossil fuels means emissions from power generation will remain close to today’s levels in 2040. “Meeting global climate goals would require a fall in CO2 emissions from electricity generation by a factor of five by 2040,” the agency said. Courtesy: IEA |

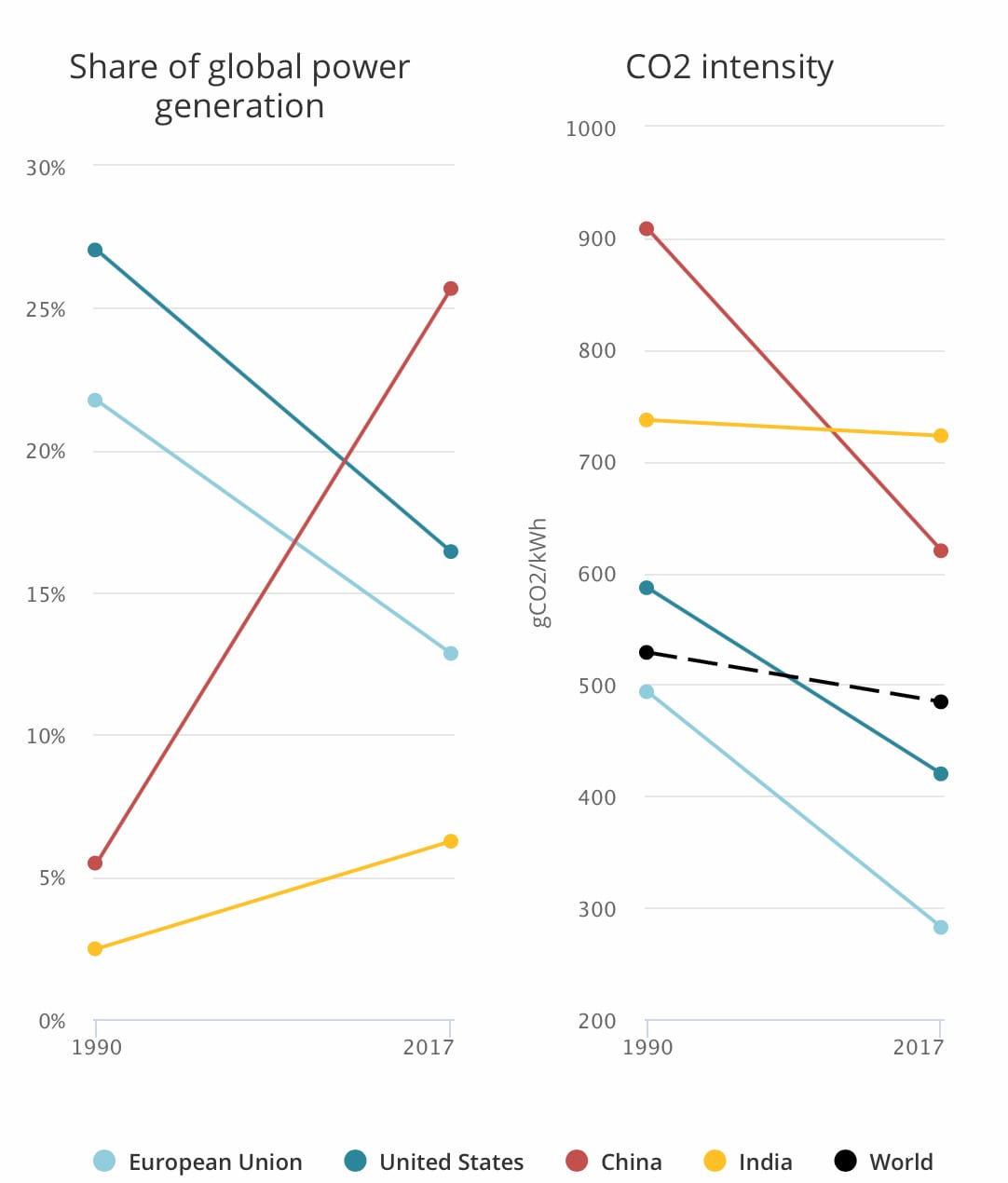

Governmental climate efforts have expanded dramatically since the 2015 Paris agreement: 192 countries have submitted “intended nationally determined contributions”—self-defined mitigation goals for the period beginning in 2020—but only 184 have ratified the treaty, and the U.S. has signaled it will withdraw from the landmark agreement. Still, according to the International Energy Agency (IEA), while power generation today accounts for 40% of energy-related CO2 emissions and more than a quarter of greenhouse gas (GHG) emissions—and despite the persistence of coal-fired power generation—the sector has contributed to a decline of about 2% annually in global carbon intensity over the past few years. A series of trends have driven the implied decoupling: improvements in power plant efficiency in many regions; switching away from fossil fuels; and greater penetration of low-carbon sources among major electricity producers (Figure 1).

What it means, according to Dan Bakal, senior director for Electric Power at sustainability leadership advocacy group Ceres, is that power companies are positioning themselves at the heart of global decarbonization. “It’s now about the pace of decarbonization, and the challenge now is that they need to increase ambition a bit more,” he told POWER in March.

Nigel Topping, CEO of We Mean Business, a coalition of seven international nonprofit organizations that works with businesses to accelerate the transition to a zero-carbon economy, agreed. “Over 40 power utilities companies have committed to bold climate action through the We Mean Business coalition’s Take Action campaign. This includes over 20 companies that have committed to science-based targets, such as Europe’s Ørsted, NRG Energy in the U.S., and CLP Group in China,” he said. The effect has been far-reaching. Owing to these efforts, he said, seven countries are already “very near” to using 100% renewable power grids, including Costa Rica and Norway, and more countries are setting out pathways to become 100% renewable, such as Spain.

The Quest for Certainty

But despite decarbonization’s obvious benefits to climate change mitigation, the impetus propelling the power sector toward low-carbon strategies appears to be its quest for sustainable business practices. As well as being one of the largest sources of GHG emissions in the U.S., it is also the most capital-intensive industry, and profitability is a key concern, noted Bakal.

Ceres, which also encapsulates Climate100-plus, a global collaboration of investors with $34 trillion in assets engaging with 160 of the biggest greenhouse gas emitters globally (about a dozen of which are power companies), notes that investors are increasingly aligning their investment decisions with environmental, social, and governance criteria. That’s one reason why shareholders of nine U.S. power companies filed resolutions in 2017 urging them to undertake analyses to examine business impacts of policies and market changes that would drive GHG emissions reductions to levels consistent with limiting a global temperature rise to below 2 degrees Celsius—a commonly accepted benchmark for climate change mitigation activities (though, in October 2018, the Intergovernmental Panel on Climate Change suggested a more stringent target of 1.5 degrees would better recognize climate action urgency).

And lately, spurred by the growing level of engagement and “investor appetite for meaningful climate disclose,” several organizations have moved to develop recommendations and guidance for companies to consider when assessing climate risks and opportunities, said Bakal. Companies appear to have settled on the Financial Stability Board’s Task Force for Climate-Related Financial Disclosures (TCFD). Those recommendations formed the basis of detailed climate scenario analyses and evaluations released by Entergy Corp. (which became the first U.S. utility in 2001 to cap CO2 emissions voluntarily and has committed to a 50% reduction in emissions rates from 2000 levels by 2030) this March, AES Corp. in November 2018, and others.

As Laurel Peacock, director of Sustainability at NRG Energy, one of the first U.S. investor-owned companies to commit to a science-based target, told POWER in April, disclosures are a key tenet of its strategy. “Managing your organization’s GHG emissions is about managing risk—and tapping into opportunity—which makes good business sense,” she said. “For NRG, setting a science-based target directly answered the needs of our customers, many of whom are thinking about their own carbon footprints. It is critical for stakeholders, who need to know that we are thinking of potential risks, in the short, medium, and long-term.”

A Long List of Power Company Climate Risks

But according to the TCFD, those risks form a lengthy list. Within the policy and legal realm, risks include increased operating costs and increasing insurance premiums associated with compliance, increased GHG emission pricing, reporting obligations, and mandates on existing products and services, as well as with litigation. Companies must also think about the financial impacts of asset impairment and early retirements owing to regulatory changes. Meanwhile, the never-ending stream of technological advancements could require lower-emitting substitutions, or end in unsuccessful investments, despite research and development expenditures. The adoption and deployment of new practices and processes are also costly. Market volatility, such as changing customer behavior, uncertainty in market signals, and increased costs of raw materials pose other financial hurdles.

Utilities have, of late, also had to grapple with acute financial impacts that stem from extreme weather events, such as hurricanes and floods—and these affect assets, operating costs, and revenues both from decreased production capacity and workforce impacts. Longer-term climate change effects on generation, such as water scarcity that diminishes hydropower generation or stymies cooling efforts at nuclear and coal plants, also pose risks. Finally, the TCFD recommends companies consider “stigmatization” if they do not act on climate change—which could result in reduction of capital availability, reduced demand for goods and services, and is a setback for employee attraction and retention.

Yet, Opportunities Abound

On the flip side, the TCFD also outlines a long list of climate-related opportunities that could offer substantial financial boosts. At the top of the list are efficiency gains sourced by reduced operating costs from more-efficient transportation, and less water usage and consumption. Shifting to lower-emission sources of energy could also reduce exposure to fossil fuel price increases and capital availability, as well as lead to a reputation boost. Opportunities also offer insurance risk solutions, business activity diversification, access to new markets and public incentives, and a better competitive position to reflect shifting consumer preferences.

Customers are emerging as a key center in the power sector decarbonization movement, as Sam Kimmins, head of RE100—an organization that was set up in 2014 by The Climate Group and the Carbon Disclosure Project (CDP), and today represents more than 180 TWh of demand—told POWER. “There’s a real market-driven transition from a corporate buyer’s point of view,” he said. “The cost of renewables is going down around 10% a year, and it seems to be an unstoppable drop in price. That really is causing companies to see it as an opportunity rather than a risk.”

The momentum among industrial power buyers is especially notable, John Hodges, managing director at BSR, which functions as a nonprofit consulting group for the world’s largest business network for corporate sustainability, told POWER. Walmart in April 2017, for example, launched Project Gigaton, a sustainability platform that encourages its broad network of suppliers to eliminate one gigaton of emissions by focusing on manufacturing, materials, and product consumption by 2030. “They’re taking it a step further and saying we’re actually going to influence other adjacent businesses as well.” In their quest to meet commitments, industrial buyers will consider all options, Hodges said. “They’re saying, ‘We want renewable power generation and we’re willing to go around our utility and go directly to a developer in order to get it done.’ ”

Corporations are so driven by sustainability commitments that this March, 300 major companies—including Google, Facebook, General Motors, and Walmart—banded together to launch the Renewable Energy Buyers Alliance (REBA). In 2018, corporate buyers in the U.S. alone made 75 deals for 6.53 GW of renewable power, including power purchase agreements (PPAs), green power purchases, green tariffs, and outright project ownership.

PPAs are taking off globally, too. In its annual report released this April, the Global Wind Energy Council (GWEC) said the model to source power through PPAs directly from wind asset owners has “matured.” During 2018, “Several sourcing and PPA models were executed (e.g. multi-buyer PPAs, proxy revenue swap, private wire PPAs etc.) and corporates, asset owners, financiers and banks have increased their experience of how to structure such deals,” it said.

|

|

2. In 2018, corporations signed power purchase agreements (PPAs) to buy a record number of megawatts directly from onshore and offshore wind asset owners, continuing a notable trend. According to the Global Wind Energy Council (GWEC), PPAs made up 12.5% of total global market volume (of 50 to 55 GW each year based on order intake activity and installations) during 2018. That compares to 7.4% in 2017. Courtesy: GWEC/BloombergNEF Corporate PPA Database. |

An estimated 60% of wind energy corporate sourcing deals (Figure 2) in 2018 were signed in North America alone, where the largest volumes were sourced by AT&T, Walmart, and Facebook. In Sweden, NorskHydro signed a PPA for 235 MW for as long as 29 years—the longest duration of a wind corporate PPA so far. GWEC suggested that corporate sourcing’s potential to become an even stronger and stable growth driver will depend on how developing countries integrate the agreements. Another lucrative avenue could emerge if smaller/local corporates enter corporate sourcing through aggregation of a customer base—an approach Swedish utility Vattenfall is reportedly working on.

Navigating the Complex Issues

Nearly every expert that POWER spoke to underscored uncertainty as the biggest challenge to business decisions concerning decarbonization. But Carlos Sallé, senior vice president of Energy Policies and Climate Change at Iberdrola, said it wasn’t insurmountable. “Almost two decades ago, Iberdrola realized that climate change was a real challenge for humanity that required urgent action. We also realized that the electricity sector was key to providing solutions to combat this global problem,” he said. The Spanish multinational utility focused on a long-term strategy, first moving to integrate climate change in its by-laws, mission, vision, and values, and then gradually shuttering 15 coal and oil plants worth 7 GW. “In two decades, we have progressed from being the twentieth utility by market capitalization worldwide, to being placed in the top five. This pioneering investment approach has demonstrated that what is good for planet and citizens is also good for our shareholders,” he said.

Key to Iberdrola’s success was looking at the long term, Bakal pointed out, and now, more companies are following suit. “The real shift that we’ve seen, in an industry where so many companies did not have long-range or medium-range GHG reduction goals, is that so many of them have now set them over the last year and year-and-a-half.” The majority of those goals are for an 80% reduction in GHG emissions by 2050 or for a 50% reduction by 2030, he noted. Kimmins added that while tough targets are typically slanted to global benchmarks, ratcheting them up actually makes “good business sense,” because they drive innovation.

But according to Steve Rose, a technical executive at the Electric Power Research Institute, assessing how a company today might be impacted by global scenarios by mid-century climate objectives—such as those focused on a 2-degree-C temperature constraint—is extraordinarily complex. “At the highest level, there is uncertainty in the relationship between a global temperature goal and global greenhouse gas emissions. From there, the uncertainty only increases as we move from global to country to local emissions with additional factors entering the story at each level,” he said. How technology, markets, and policies will evolve is also uncertain. “Research also illustrates that the emissions pathways associated with limiting global warming to 2 degrees C will be extremely demanding and may be unachievable, so companies don’t know if and when global emissions will peak and start declining.”

Working to address those uncertainties, the nonprofit last October released findings of a study to assess scientific understanding and provide guidance to companies seeking to issue climate scenario reports. Among its key findings were that utility discussions have been focused on a narrow body of scenarios—though more than 1,200 scenarios from more than 30 models exist to help them draw insights. EPRI also found applying uniform emissions reduction targets—it notes 2 degrees C above pre-industrial levels is a goal, not a scientific threshold—directly to companies is “not likely to be cost-effective for society,” and that companies should apply their individual perspectives to identify relevant uncertainties. Perhaps more significantly, they should also build flexibility into strategies, it found.

Mariana Heinrich, manager of Climate & Energy with the World Business Council for Sustainable Development (WBCSD), noted that various resources to help companies make sound data assessments and create targets to fit them are readily available. The “gold standard” appears to be the Science-Based Targets Initiative (SBTi), a collaboration between CDP, the United Nations Global Compact, World Resources Institute, and the World Wide Fund for Nature. The SBTi is designed to help companies determine pathways for reducing their emissions in line with the Paris agreement’s goal of limiting global warming to well below 2 degrees C. “We encourage our companies to look into the SBTi and see if they can align their business, and then see where do they want to place themselves in this ambition ladder,” she said. “They’d probably start with an internal process, and then go into an external process, and ultimately go into the SBTi and validate their targets publicly,” she said.

Complexity in Regulated Markets

The journey gets even more complex depending on the market, as several experts noted. Regulated utilities face special hurdles. “In many, if not most, economic sectors, changes in markets, customer needs, and technology can challenge the ability of regulators to keep up,” said Scott Smith, vice chairman, U.S. Power and Utilities leader at Deloitte.

“For utilities, this is a much more fundamental issue than in most other sectors because incumbent regulatory structures, mainly at the state level, govern so much of what a utility can do,” he said. The traditional utility regulatory model of cost recovery and allowed rate of return on investments often does not encourage innovation, and “will likely need to evolve and adapt” to recognize and incentivize new technology options such as utility involvement in energy storage, two-way power flows, cloud-based solutions, behind-the-meter customer solutions, and innovative technologies throughout the business, he added. “Fortunately, some more-flexible regulatory initiatives are emerging—and we will be watching closely to see how far these types of moves may expand—bringing new opportunity to utilities.”

Another substantial ongoing change is how business models and market structures will conform to decarbonization. The intersection between customer empowerment and enrichment of technological choice is opening new business models for incumbent utilities, but also market structures in which new, nontraditional players can enter the market, Smith noted. “For example, with the rise of behind-the-meter generation, community energy projects, and new options for households such as rooftop solar coupled with battery storage, utilities have a tremendous opportunity to develop new profitable businesses around offering services related to these developments—from installation, maintenance, and reliability services to tracking and load balancing with on-grid resources,” he said. “While we do not expect the old profit model of achieving a regulated rate of return on assets to disappear, we see the emergence and rapid growth of alternatives driven by an increasingly competitive market. In this environment, the most successful utilities may be those that can recognize and grow profitability of segmented products and services,” Smith said. ■

—Sonal Patel is a POWER associate editor.