Will the world face a glut of uranium enrichment capacity for fueling civilian nuclear power reactors in the years ahead? That circumstance appears to be increasingly likely, as firms and nations, responding to the presumed worldwide boom in construction of new nuclear plants, are adding enrichment capacity at a steady and increasing pace.

A recent Energy Daily webinar asked two questions: "New Uranium Enrichment Capacity: Will It Meet Demand? And at What Cost?" The answer to the first question appears to be yes, without much doubt. The second question is more problematic. The purveyors of enrichment services may have already made the capital expenditures that lead to oversupply by the time a glut has developed. By that time, costs are already sunk. So the question becomes: At what profit? The answer? Probably at a loss.

And a third question now presents itself: Can new technology totally upend the market, rendering the conventional profit and loss calculations irrelevant? The answer to that is perhaps. It is certainly possible, without too much pie-in-the-nuclear-sky hypothesizing.

The market largely determines the price for separative work units (SWUs), the product of enrichment. As Dave Sexton of Urenco Group explained to the webinar, an SWU "is a standard measure of the work required to achieve a given enrichment independent of efficiency of enrichment process employed."

If SWU supply exceeds demand, the price might fall enough to drive some of the capacity—most likely the older, less-efficient enrichment processes, such as the large legacy gaseous diffusion plant in Kentucky created during the World War II Manhattan Project—out of the market. If demand exceeds supply, profits will accrue to incumbent enrichment operations and attract new entrants. That’s classic Economics 101. Unfortunately, the enrichment market doesn’t always follow classic economic descriptions, as there is a mix of private, government, and quasi-governmental parties involved in the business.

A Tight Market Develops

At the Energy Daily webinar, Ron Witzel of Longenecker & Associates, a California nuclear fuel consulting company formed by John Longenecker, who headed the Department of Energy (DOE) enrichment program in its dying days, took a look at the market for SWUs. He observed that the "post-2016 market becomes very competitive" with new capacity from two major European enrichment firms, French-based (and government-owned) AREVA and the UK-headquartered Urenco Group (a British, Dutch, and German consortium) offering new capacity. Add potentially large uncontracted supplies from Russia’s TVEL-TENEX, also a government enterprise, to the economic stew.

Last June, the World Nuclear Organization (WNO) updated a paper on worldwide enrichment that looked at enrichment capacity in 2005, 2008, and 2015. It reported that 2008 capacity was 59.7 million SWUs/year, with demand for 48 million to 48.5 million SWUs annually. By 2015, the estimated supply would be 69 million yearly SWUs supplying a demand of 47 million to 61 million SWUs.

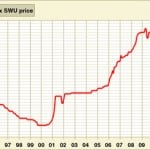

SWU prices have declined recently, from $165/SWU to $153, according to reports from UxC Consulting, a Roswell, Ga., firm that tracks nuclear fuel prices. Witzel added that "SWU pricing is not transparent" and that "reported pricing does not reflect varying terms."

That price opacity reflects the mixed nature of the market. It also is a result of the variety and complexities of contracts for enriched fuel, as consultant Jim Malone explained to the Energy Daily online audience. There are two basic contract forms (and plenty of variations inside that Manichean construct): long-term and spot market. The $153/SWU price as of the end of July is a spot price, according to UxC.

Contract Complications

Enrichment supply contracts can be for EUP or "enriched uranium product" or just for SWUs, only the enrichment process itself. As explained by the U.S. Supreme Court, in a case involving alleged unfair competition in the U.S. market (U.S. v. Eurodif, No. 07–1059), under EUP "the utility simply pays the enricher cash for [low-enriched uranium (LEU)] of a desired quantity and ‘assay,’ i.e., its percentage of the isotope necessary for a nuclear reaction."

In an SWU contract, the court noted, "The utility provides a quantity of feed uranium [UF6] and pays the enricher for the SWUs to produce the required LEU quantity and assay. SWU contracts do not require that the required number of SWUs actually be applied to the utility’s uranium. Because feed uranium is fungible and essentially trades like a commodity, and because profitable operation of an enrichment plant requires the constant processing of feed uranium from the enricher’s undifferentiated stock, the LEU provided to a utility under a SWU contract cannot be traced to the particular unenriched uranium the utility provided."

The Players Around the World

For the U.S. market, the main player is USEC (U.S. Enrichment Corp.), based in Bethesda, Md. The DOE formally spun off its government-owned enrichment enterprise, a relic of the World War II Manhattan Project, to USEC in the early 1990s, as a government-controlled, private corporation. USEC evolved into a free-standing, shareholder-owned enterprise at the turn of the 21st century. USEC was the sole provider of U.S.-based enriched uranium services until earlier this year, using its inherited, elderly, and inefficient gaseous diffusion technology to produce 11.3 million SWUs a year.

But after an 11-year business and regulatory marathon, Urenco this summer began operating a modern centrifuge enrichment plant in Eunice, N.M., at an unofficial cost estimate of $3 billion. By 2020, the plant should be producing 5.7 million SWUs per year (and is currently at 3 million SWUs). AREVA is also planning to directly enter the U.S. enrichment market, with a $2 billion DOE loan guarantee for a plant in Eagle Rock, Idaho, which should produce 3.3 million SWUs a year by 2017, at a plant cost of $3.3 billion. According to Witzel, the plant would expand to 6.6 million SWUs by 2022.

AREVA held public meetings in Boise and Idaho Falls in August on the planned Eagle Rock plant. The company hopes for a combined construction and operating license (COL) from the U.S. Nuclear Regulatory Commission (NRC) for the plant in the middle of next year and commercial operation in 2014.

USEC is also planning a major expansion, moving from its technically obsolete diffusion technology to advanced centrifuges to separate U235 from U238 in the uranium hexafluoride feedstock. But there is a technical gamble involved in the project, planned for Piketon, Ohio. It will use large centrifuges never before put into commercial application. USEC took over the Piketon project from the DOE, as a failed research and development effort of the 1980s, when it was consistently over budget and off schedule. USEC has dubbed it the "American Centrifuge" to differentiate the technology from the smaller centrifuges used by Urenco and AREVA. USEC says it has solved the technical issues and has run "more than 480,000 machine hours" in tests since 2007.

USEC applied for a $2 billion DOE loan guarantee for the centrifuge project under the terms of the 2005 Energy Policy Act. The DOE rejected the application in 2009, citing technological and financial issues. In late July, USEC submitted a new application. "We have addressed, head on, each concern raised in the independent engineer’s report that was prepared for DOE last year. The American Centrifuge program is much stronger today because of that sharp focus," said John K. Welch, USEC CEO, in a press release. On the financial side, Babcock & Wilcox and Toshiba Corp. have agreed to invest a total of $200 million, in three increments and contingent on the DOE loan guarantee, for the $4.4 billion project. According to industry sources, USEC is continuing to look to Japan for additional investment. The project is designed to produce 3.8 million annual SWUs.

Enrichment Wild Cards

On top of the known plans for expansion, there are some wild cards in the SWU capacity game. One is Russia. Tenex, the Russian enrichment enterprise, has excess capacity, according to Ron Witzel. He noted that TVEL Fuel Co. has taken over the activities of Tenex, which will be only a marketing arm for Russian SWUs. Both are state-owned. The implication of this consolidation in Russia, Witzel said, "is not totally clear at this point." He said two enrichment suppliers from Russia may emerge, and there is a possibility is that SWUs made in China from Russian technology could move into the U.S. Russian enrichment capacity is about 25 million SWUs today, according to the WNO, and could grow to 33 million by 2016. A U.S. Department of Commerce quota limits imports of Russian SWUs, but Russia could create a gray market to get around the quota, much as it did through a process called "flag swapping" in the 1980s.

That leads to a second wild card: China. According to the WNO report, the China Nuclear Energy Industry Corp. (CNEIC), based in Beijing, today has capacity to produce about 1.3 million SWUs per year. By 2015, that could more than double, to 3 million. Recently, according to Witzel, "CNEIC offered 300,000 SWUs/year for five years to Korea Hydro and Electric and 150,000 SWUs/year to a U.S. utility," and there are other long-term offers of Chinese SWUs to U.S. utilities on the table.

Finally, there is a technological wild card: laser separation of U235 from U238. The DOE pioneered this technology, known at the time as "atomic vapor laser isotope separation," or Avlis, and turned it over to USEC, which planned for it to be the next generation of enrichment production. But USEC was unable to take the technology any further toward commercial operation.

New Technology

In the meantime, Australian inventors Michael Goldsworthy and Hans Struve came up with a laser enrichment technology that has commercial promise, called "separation of isotopes by laser excitation" or Silex. They won a major investment in 1996 from USEC. Struggling to keep itself financially afloat during a soft market combined with high costs, USEC bailed out of Silex six years later.

General Electric licensed the Silex technology, and it is now owned by a GE-Hitachi-led group known as Global Laser Enrichment, or GLE Silex. The firm is operating a test loop in Wilmington, N.C., and applied to the NRC for a full-fledged COL last January. The developers say they expect NRC action by the end of next year or early in 2012, under the agency’s 30-month process for license reviews. Unlike the USEC project, GLE Silex does not depend on a DOE loan guarantee for its financing, as its partners have deep pockets of their own.

According to Australian press accounts, GLE expects its commercial Silex project, to be located in North Carolina, to have an annual capacity of 3 million to 6 million SWUs, at a capital cost of $1 billion. If those estimates are in the ballpark, Silex will be a major game changer. It could leave a lot of red-faced developers sitting on new plants that cost three times or more per SWU than the Silex technology.

—Kennedy Maize is MANAGING POWER’s executive editor.