Much has been made recently of Mexico’s energy sector reforms, and because those reforms are still in being implemented, it can be useful to compare their progress with the outcome of previous reforms in Latin America. (A condensed version of this material appears in the January 2015 print issue of POWER: “Can Mexico’s Electricity Reform Deliver on Its Promise?”)

Starting in the 1980s, many countries in Latin America carried out reforms of their electricity sectors that opened up to private investors services previously provided by vertically integrated state-owned utilities. According to the World Bank, since 1984, when Chile adopted reforms, the region has received nearly US$270 billion in private investment in electricity projects, of which $33 billion went to divestitures of state-owned assets and $168 billion to greenfield projects. Argentina, Colombia, Brazil, Chile, Ecuador, and Peru, which undertook deregulation and privatization programs to varying degrees and adopted different market structures, account for over 80% of these investments. The opportunities to invest, and the performance of investments following reforms, varied across countries, depending on the electricity deficit at the time of reform, the structure given to markets, and the country’s geographic and resource endowment.

In Chile, for example, private investors entered the electricity market by purchasing existing state-owned assets. Market rules allowed some early players to become dominant: In a few years, Endesa came to own nearly 60% of the generation market in the Central System, along with ownership of transmission and distribution, and control of most the country’s water rights. Endesa and AES, another early participant, were responsible for nearly half of all investment in new electricity generating capacity between 1984 and 2004. On the whole, the Chilean reform introduced market-driven incentives that greatly improved the performance of the system, while at the same time allowing high levels of market concentration. Consumer prices declined, but not as much as wholesale prices, which fell nearly 40% in the first decade, with distribution companies capturing the difference.

Learning from its neighbor’s experience, Argentina adopted reforms that went further in deregulating its electricity sector. Its market rules forbid majority cross ownership across generation, transmission, and distribution; they also forbid any generator owning more than 10% of installed capacity. At the time of reform, Argentina was suffering power shortages and blackouts, and with market reforms the number of generating companies increased from 25 to 43, with a total of 96 power generating plants. Open access to the grid and cost-based dispatch led to the gradual elimination of older, less-efficient facilities as well as a significant decline in prices—and profit margins.

Brazil followed the model of Chile and Argentina but undertook partial reforms that were later modified in response to the severe drought of 2001–02. Brazil is overwhelmingly reliant on hydropower, and the purpose of reform was to attract more thermal power to add stability to the system. The dispatch rules, however, allowed hydro to maintain dominance in wet years and provided weak signals for investment in new capacity. The unreliability of the gas supply added to this uncertainty. As a result, the addition of both thermal and hydro capacity has lagged behind demand. Most thermal generators have either pass-through contracts with the distribution companies or contracts with Petrobras that provide a revenue guarantee.

In general, the international experience with market reform of electricity has shown that creating competition by attracting new investment cannot be achieved by simply abolishing monopolies. Adequate regulation is essential for the system to send the right price signals to potential investors.

Mexico Takes the Baton

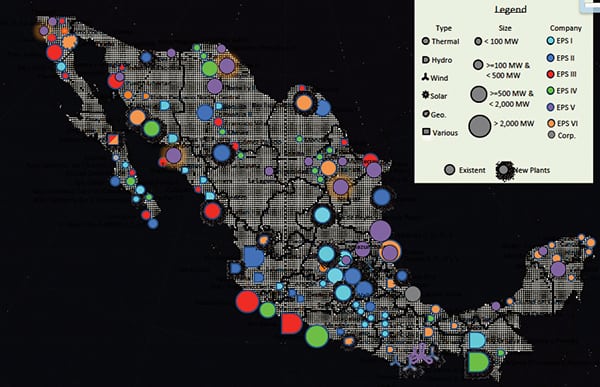

The Mexican government first passed reforms in 1992 to allow privately owned and operated generation of electricity. Ten years later, independent power producers (IPPs) started coming online and now account for 21% of installed capacity. Private participation, in and of itself, did not have the desired effect of reducing prices. Under the first reforms, the Federal Electricity Commission (CFE) continued to be the sole authorized provider of electricity, purchasing all of the power generated by IPPs under long-term contracts. The reforms also allowed self-supplying power producers (an additional 10% of installed capacity) to sell to captive industrial customers, but not to the system.

The reforms passed in 2013 went further and eliminated the state’s monopoly of the energy sector, opened access to transmission and distribution systems to private power producers, and created an independent operator to run the wholesale market. Large customers are now allowed to contract directly from generators and are expected to drive the demand for new generation. In order for customer demand and new electricity supply to meet, however, the rules of the market will have to address the unusual position of CFE in the system.

CFE continues to own and operate all transmission and distribution, along with two-thirds of existing generation. Furthermore, CFE receives subsidies from the government, which are unlikely to disappear, given the promise of reducing prices that drove the reform. These factors can strongly affect both the ability of the system to operate as intended and the potential for investment in new generation.

A Competitive Electricity Market

In a competitive electricity market two systems operate side by side: the dispatch operation, including short-term energy transactions, and the long-term contract market.

The system operator is responsible for dispatching generators to meet demand based on declared costs (or bids) and taking into account the load distribution and availability of transmission in the system. Plants are dispatched in increasing order of cost (or bid price) until demand is satisfied. The last unit to be dispatched determines the marginal cost of the system, from which the spot price is derived.

In a system that operates solely on a spot basis, generators are paid the spot price every hour (or fraction thereof), allowing more efficient generators to make the difference between their costs and the price set by the last unit to enter the system. The system operator also pays for capacity made available by generators, with a variety of designs in place with regards to reserve capacity and capacity from renewable sources, such as hydro.

The second system entails long-term commercial transactions among generators and large customers and, in a few cases, commercial intermediaries or brokers. Generators and large customers, including distribution companies, can sign long-term power purchase agreements (PPAs) at negotiated prices. Under long-term PPAs, the customer pays the generator for the energy consumed at the agreed price, regardless of fluctuations in the spot price of energy and the order in which generators are dispatched. Generators may freely negotiate PPAs with large-scale customers, but they may be subject to regulation when negotiating with distribution companies that sell to regulated customers.

Both systems contribute to sending price signals to investors. The marginal cost of the system signals the need for new investment, which over time should cause the marginal cost to converge with that of the most efficient unit that could possibly be built. Long-term PPAs serve to forecast future prices and reduce uncertainty for investors seeking to enter the market. Several factors can affect the signals the market sends to investors and their ability to respond. In the case of Mexico, vertical integration and market concentration are the most important.

The Perils of Market Concentration

Based on a comprehensive study of energy market reforms, the World Energy Council finds that generators can exercise market power with as little as 10% of market share. Market power is exercised by incumbent players cooperating to keep marginal costs high and by creating access barriers to new entrants. CFE owns a majority share of generating capacity, which includes the oldest and higher-cost plants, so it will continue to be the price-setter of the system, benefitting itself, as well as the existing IPPs that profit from generating at costs that are below the marginal price.

Given that the reforms did not contemplate breaking up CFE into multiple units that compete with each other, there are strong incentives for existing generators to cooperate against the entry of new units. In order make room for new generation, the planning agency would have to mandate the retirement of older plants. This was done in England and Wales in late 1990 to address the generation duopoly that was maintaining the status quo more than a decade after reforms were implemented.

It is possible, as in the case of Argentina, for older plants to be naturally displaced by competition from new entrants attracted by high prices. In order for this to happen, however, the path to entry must be clear of obstacles, in particular those related to permitting and the availability and pricing of transmission and distribution.

The transmission system in Mexico today suffers from bottlenecks and deficiencies that have already prevented the incorporation of competitive renewable generation. Insufficient transmission capacity affects the ability of the system operator to dispatch in the most economical fashion and could hamper the entry of new generators, as the law so far does not establish how transmission costs will be allocated among agents in the system, or who will be responsible for interconnection upgrades and additional transmission capacity. The regulatory commission (CRE) will be in charge of granting permits and setting transmission tariffs. It is not clear, however, whether new investment will be market-driven, with the CRE granting permits based on feasibility and security criteria, or whether the CRE will be in charge of deciding if investments are needed and have the authority to require that new installations be built.

The Chilean experience shows that even under conditions of competition and market-based pricing, concentrated ownership of transmission can significantly alter business terms for existing and new competitors. Under the law of 1982, generators were expected to negotiate transmission prices with the transmission company, but these negotiations were rarely successful and often required arbitration. In one case, the generating company, Colbún, opted to build its own dedicated line after several years of failed negotiations with the transmission company. Vertical integration in Chile also directly affected competition for nonregulated customers in the Santiago metropolitan area, where the transmission and distribution company, which also owned generating capacity, priced its services to put competing generators at a disadvantage.

One arrangement recommended by experts for Mexico, given its twin constraints of subsidized residential tariffs and a dominant service provider, is to reserve industrial demand (nearly 60% of electricity sales) for private generators, and leave CFE as the exclusive supplier of household electricity. Under this scheme, CFE would not compete with other generators for long-term PPAs with industrial users, allowing them to access the cheapest possible electricity and inducing competition among generators for their business. CFE in turn would have plenty of installed capacity to serve regulated customers and could retire its least efficient plants. As a distribution company, CFE could also enter into PPAs with private generators and over time close the gap between its generating costs and the prices charged to residential consumers, thus reducing the need for subsidies.

Regulation First

The experience with deregulation and privatization of electricity and other services in the region also indicates that, to prevent consolidation of incumbent market power, the regulatory framework and authorities must be fully in place before the new system begins operation. It took Chile nearly 20 years to overhaul its regulatory system to address the cost and uncertainty caused by vertical integration and other limitations to competition created by the initial legislation because existing players in the system became vested in maintaining it, and the regulatory agencies and courts were either unable or unwilling to intervene.

The privatization of telecommunications in Mexico in the 1990s provides important lessons on the subject. The privatization of telecommunications was far from successful (from the point of view of tariffs, openness to competition, and expansion of service) to a great extent because the state monopoly was transferred to the private owner as a vertically and horizontally integrated firm with a six-year period of exclusivity in long-distance service. These conditions allowed the newly privatized company, Telmex, to build a first-mover advantage in all segments of the service, including those that are not natural monopolies, like cellular telephony. Furthermore, privatization of telecommunications was carried out prior to the creation of a regulatory agency; five years went by between the privatization and the publication of regulations that would specifically address market power, which Telmex has successfully contested in court.

The Mexican government should avoid making the same mistakes with energy in its rush to implement reforms.

The secondary legislation passed so far in Mexico for electricity (Ley de la Industria Eléctrica) has reallocated the functions previously concentrated in the hands of CFE to other agencies and given them formal autonomy. CENACE (Centro Nacional de Control de la Energía) is perhaps the most important for the electricity sector, as it will be responsible for guaranteeing open access to transmission and distribution and operating the dispatch of the system.

According to the regulations currently being debated in Congress, the regulatory commission (CRE) will share in many regulatory responsibilities, for example, in accepting or rejecting bids from generators and overseeing that transmission and distribution companies fulfill connection requests. To date, CENACE has had a board appointed, which includes the minister of energy and officials of the Finance Ministry and SENER (Secretaría de Energía). The most important directives that will govern operation of the system, the Market Rules, are yet to be decided. These are not subject to congressional approval; they will be created by SENER in 2015 if the new system is to begin operating, as expected, at the end of the year.

Uncertain Outcome

Mexico has undertaken a reform of its electricity sector because prices are too low to cover costs, which deters investment in new capacity and burdens the government with an expense that is politically difficult to eliminate. At the same time, industry pays prices significantly above those in the U.S. (industrial rates are $121/MWh in Mexico and $68/MWh in the U.S.). Improving the competitiveness of industrial electricity tariffs without raising prices for residential customers poses significant challenges; it requires allowing cheaper generation to enter the market and displace more expensive units.

The legislation passed so far in Mexico contains the necessary elements—a wholesale market run by an independent operator, unrestricted access to transmission and distribution networks, and open participation of private investors in electricity generation—that would allow, but by no means guarantee, the desired outcome. Success will require that Mexico put in place deliberate and well-thought-out pricing and permitting regulations and endow its regulatory agencies with the authority and autonomy to implement them.

In the absence of adequate regulation, it is possible that reforms will fail to attract new investment, or will result in increased prices, as was the case with market reform in England and Wales.

—Sylvia Gaylord, PhD (sgaylord@mines.edu) is an assistant professor at the Colorado School of Mines and an energy consultant.

[This article first appeared online Dec. 8, 2014.]