Everybody is now jumping on the pro-nuclear bandwagon. With U.S. electricity demand ramping up due to the rapid build-out of energy-intensive data centers across the country, there is finally broad political and business support for dispatchable 24/7 nuclear power to help meet projected load growth and ensure overall grid reliability. The Trump White House, the Republican-led Congress, and Big Tech are all on board with the idea that nuclear generation capacity must be increased to keep pace with the country’s growing electricity consumption.

COMMENTARY

However, that’s where the nuclear consensus breaks down. Thus far, the main focus has been on restarting mothballed reactors and pursuing the development of new—and largely unproven—smaller, modular reactor (SMR) designs. There has been little to no interest in building more of the well-established large-scale reactors that are the workhorse of the domestic industry.

The widespread perception in the electric utility industry is that conventional large reactors are too capital-intensive, too time-consuming to build, and too financially risky to undertake. This is problematic since these companies are the operators and owners of the current nuclear fleet and the traditional sponsors of new capacity.

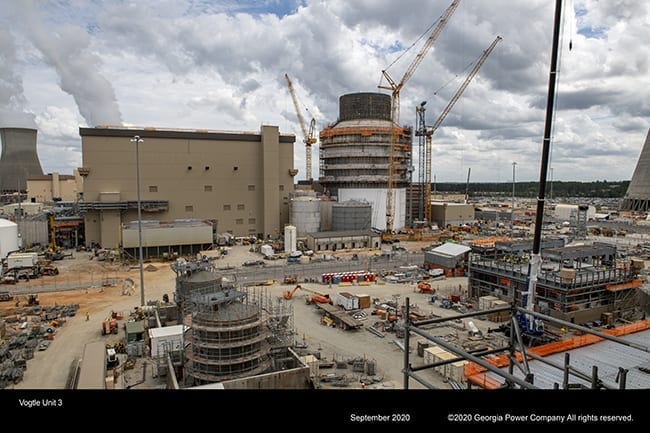

Over the past 50 years, investor-owned U.S. electric utilities have had a poor track record of adding new nuclear capacity on a timely and cost-effective basis. The last two large-scale U.S. reactors connected to the grid over 2023–2024 at the Vogtle Plant in Georgia, which were the first to use the next-generation Westinghouse AP1000 model, came in at a record-setting $16,000 per kilowatt each.

Even though several non-recurring factors combined to raise the total cost of these two first-of-a-kind units, no utility company seems able to get past the Vogtle sticker shock. As of this writing, there are no committed orders or signed contracts for building another AP1000 reactor in this country.

To break the current logjam caused by risk-averse utility sponsors no longer willing or able to confront the financial risk of building new reactors, a new nuclear financing model is needed—one predicated on an asset-based project financing approach and anchored by a new class of investors during the construction phase who are better capable of managing the upfront financial and development challenges of a greenfield nuclear project.

Large infrastructure private equity firms such as Brookfield Asset Management, BlackRock’s Global Infrastructure Partners and Macquarie Asset Management have experience in the overlapping domains of energy, infrastructure, project delivery, and risk management. While not active thus far in large-scale nuclear power, such greenfield experience is fungible and transferable given the networks of operating teams, technical experts, and development companies that these fund managers can draw upon.

All the incumbent infrastructure investment firms also have critical mass in terms of capital resources and the ability to write the large upfront equity check required for large-scale nuclear construction. There is currently some $1 trillion of infrastructure-related private equity capital that could be used to fund new U.S. nuclear projects, including a significant amount of supplementary capital available from third parties such as technology companies. The top seven Big Tech companies combined, the “Magnificent Seven,” alone currently have nearly $0.5 trillion of cash on hand.

Utilizing an asset-specific project finance model that maximizes lower-cost debt in the capital structure would allow these new private equity sponsors to sell a completed nuclear plant to a utility operator at an attractive all-in price including financing costs while still achieving their targeted fund returns.

Attracting private equity capital to the nuclear power space will require a favorable investment backdrop which, in turn, will depend on greater regulatory certainty, especially during the all-important construction phase, something that now appears underway.

The four executive orders signed by President Trump in May 2025 to “usher in a nuclear energy renaissance” and “re-establish the United States as a global leader in nuclear energy” importantly included significant reforms at the Nuclear Regulatory Commission, which has been the chief source of construction delays and completion risk for the industry over the past 50 years.

That said, the administration’s ambitious goal of quadrupling U.S. nuclear generation capacity to roughly 400 gigawatts by 2050 will only be achieved if large-scale reactors play a prominent role. While nuclear SMRs are currently in vogue, these units will never be able to move the capacity needle even if they are ultimately shown to work at commercial scale.

It is important that the U.S. nuclear industry get back on the horse and build another AP1000 reactor to finally realize the synergies and economies of scale that come with standardization, repetition and accumulated institutional knowledge. For this to happen, it will require a new financing approach and a new set of project sponsors better equipped to manage the outsize risks of large-scale nuclear construction than your local electric utility.

—Paul H. Tice is a senior fellow at the National Center for Energy Analytics and author of the new report, “A Strategy for Financing the Nuclear Future.”