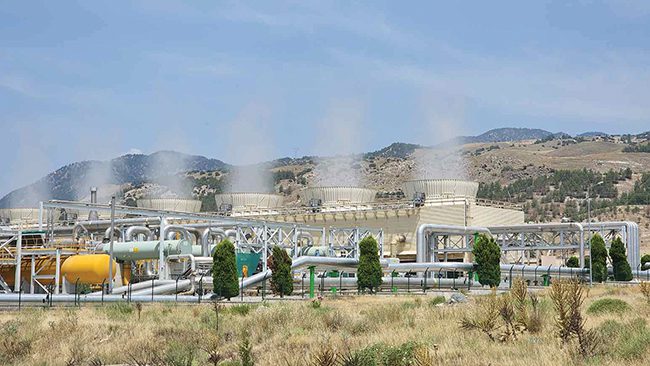

For more than a century, geothermal energy has quietly provided consistent, low-carbon power to parts of the U.S. Immune to weather disruptions and environmentally clean, it offers a stability few other energy sources can match. Yet for decades, geothermal remained a niche player, not due to lack of potential, but because the technology to access it at scale was out of reach.

That’s changing. Advances in horizontal drilling, adapted from the oil and gas (O&G) sector, are opening up deep geothermal resources once considered inaccessible. As a result, geothermal is emerging as a viable source of zero-carbon baseload power capable of delivering round-the-clock energy to a grid increasingly reliant on intermittent renewables. In a decarbonizing economy, geothermal is no longer an afterthought. It’s becoming essential infrastructure.

COMMENTARY

Advances in hydraulic fracturing and directional drilling, pioneered by the fossil fuel industry, are now driving the shift from conventional geothermal, which depends on rare natural reservoirs of hot rock and fluid, to next-generation systems. Artificial reservoirs can be engineered more than 10,000 feet deep, tapping into widespread hot rock exceeding 200C (392F). While geothermal is inherently complex, it really just boils down to consistently delivering large volumes of hot geothermal brine to the inlet of the power plant.

Globally, geothermal has been slow to scale, with just 382 MW added in 2024. But momentum is building. The U.S. now leads the world with 3.7 GW of installed capacity, accounting for 23% of global output, and more than 2 GW of next-gen projects currently in development. Supported by the Department of Energy’s (DOE’s) 2023 Liftoff program, next-gen geothermal has moved firmly into the demonstration phase, with early pilots showing strong potential for cost-effective, zero-carbon baseload power. The DOE has set ambitious goals: 5 GW of capacity by 2030, 90 GW by 2050, and a 90% reduction in the cost of next-gen geothermal by 2035 through its Enhanced Geothermal Shot initiative.

This article is part of POWER’s annual special edition published in partnership with the RE+ trade show. This year’s event is scheduled for Sept. 8-11, 2025, in Las Vegas, Nevada. Click here to read the entire special issue, and if you’re attending RE+, be sure to connect with the POWER team at our booth on Venetian Level 1—V3046.

How Horizontal Drilling Changes the Economics

Geothermal has historically faced steep costs. Drilling deep, high-temperature wells is expensive, time-consuming, and technically challenging. But horizontal drilling is now reshaping the cost curve in much the same way it did for shale gas and tight oil.

Fervo Energy recently drilled a 15,000-foot geothermal well in just 16 days, with a max average rate of penetration (ROP) of 95 feet/hour (29m/hr), 79% faster than the DOE’s baseline for ultradeep geothermal. Previously, the company’s Project Red pilot reached a record flow rate of 107 kg/s, achieving performance once expected to be at least a decade away.

These advances are driving down the levelized cost of electricity (LCOE) for geothermal. Fervo’s latest wells come in under $5 million each, compared to $13 million just a few years ago. At scale, that brings LCOE into the $70/MWh range, which is competitive with nuclear, gas with carbon capture and storage (CCS), and many long-duration storage solutions.

Just as important, horizontal drilling improves the repeatability of geothermal wells. Each new well generates valuable subsurface data on rock conditions, equipment wear, flow behavior, and reservoir response. That data can be applied to optimize the next set of wells, creating a learning loop that drives further cost reductions and faster development cycles.

Commercial pilots from companies such as Fervo, Eavor, GreenFire, and Sage Geosystems are already proving the model. Fervo, for example, has announced plans to deliver 400 MW of contracted power by 2028, scaling rapidly from a current pilot capacity of 14 MW.

Scaling Up: From Demonstration to Deployment

Pilot projects are proving that horizontal drilling works for geothermal. The next step is scale. To move from tens of megawatts to gigawatts of capacity by 2030, the industry must drill hundreds, if not thousands, of horizontal wells. This will require a massive uptick in drilling activity, workforce training, and supply chain coordination.

At current estimates, it takes roughly 20 production and injection wells to support a 30-MW geothermal facility. At $5 million to $13 million per well, that’s a significant capital outlay. Yet with horizontal drilling reducing time and improving efficiency, the cost per megawatt is falling rapidly.

Infrastructure investors are starting to pay attention, and so are utilities under pressure to secure firm, zero-carbon baseload power to balance growing renewable portfolios. Several major U.S. utilities, including Southern California Edison, have already signed long-term power purchase agreements (PPAs) with geothermal developers, signaling confidence in the scalability and reliability of horizontal geothermal. Tech companies like Meta and Google are also investing, willing to pay a premium to meet surging data center demand and advance their decarbonization goals.

Beyond Electricity: Expanding the Use Case

While baseload electricity remains the core value proposition for geothermal, its applications are expanding. High-temperature geothermal brine can be used directly for industrial heating, desalination, and district energy systems. It can also support critical mineral extraction, particularly lithium, offering new revenue streams for project developers. These capabilities make geothermal uniquely versatile among clean energy technologies.

As interest grows, new offtake models are emerging. Flexible PPAs, hybrid grid contracts, and multi-use agreements that include power, heat, and mineral rights are helping to de-risk investment and accelerate commercialization.

While horizontal drilling has made next-gen geothermal possible, two key technical areas still need additional innovation:

Exploration and Resource Characterization: Geothermal developers need better tools to identify viable hot rock zones and optimal well placements. Unlike oil and gas, where seismic and subsurface imaging are well established, geothermal exploration lacks standardized, scalable tools. Improved simulation software, real-time monitoring, and machine learning models can help reduce drilling risk and lower project costs.

Thermal Management and Reservoir Stability: The biggest unknown in engineered geothermal systems is thermal decline—how fast a rock formation cools once production begins. If heat is extracted too aggressively from one zone, it can reduce the longevity and output of the system. Advanced well completions that ensure even flow and heat distribution will be essential to maintain long-term performance.

Most technologies addressing these gaps are still at Technology Readiness Level (TRL) 3–7 and will require partnerships, field testing, and continued DOE support to advance.

The Opportunity Ahead

The demand for clean firm power is growing. According to multiple grid models, the U.S. will need between 700 GW and 900 GW of clean firm capacity by 2050 to fully decarbonize the grid. No single technology, whether nuclear, long-duration storage, or hydrogen, can meet that need alone.

The value of geothermal value lies not only in its consistency but also in its versatility. Beyond power, it can supply direct industrial heat, support mineral recovery from brines, and provide flexible grid services, all from a domestically sourced, zero-carbon resource. What horizontal drilling offers is a pathway to make geothermal ubiquitous, not exceptional. It turns one of the oldest renewable energy sources into one of the most scalable solutions for the future.

—Prutha Atre is director at Silicon Foundry, a Kearney Company.