Global Prospects for Gas-Fired Power Generation

The 2008–2009 global financial crisis affected the power generation industry in many ways, but mostly in terms of lower availability of financing, as well as deteriorating returns on investment. Such issues still persist to some extent, exacerbated by the Eurozone sovereign debt crisis, eroding market confidence, and liquidity of the banking sector.

The medium- and long-term prospects for gas are sound. Global production of natural gas increased by 82% in the past decade, mainly to meet the growing power generation needs. The availability of gas has grown massively as a result of new pipeline schemes, such as Nabucco (from Asia to Europe), expansion of global liquefied natural gas (LNG) production led by Qatar, and the boom in shale gas production spearheaded by the United States but gradually spreading to other regions.

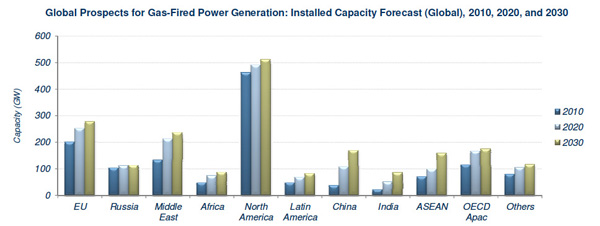

Gas-fired power generation—increasingly preferred by many countries for its relatively clean-burning characteristics and its flexible operating capabilities—is expected to grow across all regions of the world (Figure 1). This is in contrast to coal-fired power, where the bulk of the growth will be driven by the Asian behemoths of China and India while capacities in many developed countries decline gradually. It is, however, China and India that will have the highest gas-fired growth rates, albeit from a fairly low current base. Capacity is also expected to more than double in the ASEAN region. North America and Europe will maintain their lead as the regions with the largest installed gas-fired capacity through 2030.

1. Gas-fired generation capacity is expected to grow strongly worldwide in the next two decades. Courtesy: Frost & Sullivan

Global installed gas-fired generation capacity is forecast to rise from 1,311 GW in 2010 to 2,008 GW in 2030, with electricity generation rising from 4,444 TWh to 7,187 TWh over the same period.

Natural gas prices, having declined steeply following the global economic downturn and as a result of increased gas supplies from LNG and unconventional gas, are lower despite some global variations. They are expected to remain unchanged over the next few years, with the oil price link expected to weaken further in North America and Europe.

Market Drivers

Four factors appear to be driving the rate of new gas-fired generation.

Decommissioning of Aging Power Stations. The European Union and North America are the largest markets for power station decommissioning in the world. This is because a majority of their power plants—in particular the coal-fired units—are in the second half of their life cycle. In Europe, as a result of the Large Combustion Plants Directive (LCPD), numerous plants that have not upgraded their air pollution control equipment are scheduled to close by 2015. Aging capacity and legislative initiatives have, therefore, created a substantial replacement market. Considering the unpopularity of coal in these developed regions, the majority of old plants will be replaced by gas-based plants.

Availability and Price of Natural Gas. The availability of gas has grown massively because of new pipeline schemes, such as Nabucco, expansion of global LNG production, and the boom in shale gas. The latter is transforming the United States into a gas exporter, but the exploitation of shale reserves in other regions may also bring benefits in Europe, China, and Latin America. Growing availability of gas, combined with the economic downturn, have brought about a prolonged period of relatively low gas prices, boosting gas-based generation.

Established Technology. Gas-fired generation is arguably the most established generation technology, which, in times of economic uncertainly, makes it a very safe bet. While coal-fired technology has also been long established, environmental requirements mean that future plants need to be increasingly based on some new technologies that still have little track record or are still somewhat unproven or even uncertain, such as ultrasupercritical technology, integrated gasification combined cycle, and carbon capture and storage (CCS).

The persisting credit crisis and economic downturn in the developed regions of the world, however, have a negative impact on the development of clean coal technologies. While these are expected to take off in the medium to long term, research and development, as well as the establishment of pilot plants have slowed down because of funding problems as governments and private investors alike rein in spending. Gas-fired generation, as a well-established, fairly clean generating option is, therefore, likely to benefit from delays and possible doubts over the development of CCS.

Renewables Require Backup Capacity. Gas-fired plants also benefit from the rapid growth in renewable energy in many parts of the world. As intermittent sources such as wind and solar photovoltaics grow, so does the need for backup power. Gas-fired plants are widely regarded as the best option for providing this backup. Coal plants and nuclear power plants are also gradually becoming more flexible; however, they cannot offer the same degree of operational flexibility and fast startup times that gas turbines offer.

In the European Union—the global leader in green energy—gas plants are increasingly needed in countries such as Germany, where the buildup of renewable energy capacity—first in wind and now increasingly in solar power—has been extremely rapid. In the next decade, the focus of global renewable energy development will shift to the emerging regions of the world. Many of these markets look to green energy as a way of reducing atmospheric air pollution and lowering their dependence on fossil fuels. Growth in these emerging markets will also then drive the need for gas-based backup capacity.

Market Restraints

Three key issues appear to be restraining the adoption of gas-fired generation: economic crisis, volatile gas prices, and gas supply concerns.

Economic Crisis Affecting Project Funding. The global credit crisis, which started in the United States in 2008, persists. The Eurozone sovereign debt crisis of 2011/2012 has further eroded market confidence and liquidity of the banking sector. Utilities and independent power producers are more cautious and are closely reviewing investment decisions. Medium-sized and smaller utilities have significantly scaled back investment plans. Electricity consumption in many countries of the developed world has still not recovered to pre-crisis levels. Moreover, the projected growth in renewable energy may reduce operating hours of gas plants. Such developments potentially erode future profitability and, therefore, viability of some plants.

Volatility of Natural Gas Prices. Gas prices are more volatile than those of coal and uranium, therefore increasing risk and acting as a deterrent for some investors. Gas prices have been relatively low in the recent past as a result of the United States shale gas boom and the rapid expansion of LNG capacity in the Middle East and Southeast Asia in particular, but events such as the Fukushima nuclear disaster or political developments such as growing tensions between Iran and the western world can lead to sudden increases in wholesale gas prices.

Natural Gas Supply Security Concerns. Considering the growing availability of natural gas as a result of new pipeline connections, the expansion of global LNG infrastructure, and expected growth of unconventional gases, such as shale gas and coal bed methane, concerns over supply security do not feature highly in most investors’ minds. However, in countries where natural gas already generates a high share of electricity and where aging coal capacities are increasingly replaced by gas, this may become a major restraint in the future.

With the majority of natural gas being produced in potentially unstable regions such as Russia, the Middle East, and Africa, there are significant political and security risks involved in having a high reliance on natural gas imports from a limited number of sources. The United Kingdom, for instance, has the vast majority of its LNG imports coming only from one country—Qatar. Concerns over supply security have also emerged in Japan, which is aggressively expanding its renewable capacity in a bid to reduce its gas import dependency. Parts of Southeast Asia, traditionally relying on gas for their power generation needs, are now turning away from an excessive reliance on gas, preferring instead to build more coal-fired power stations.

Technology Trends

The key areas of technology development for gas turbines are greater efficiency, lower emissions, lower maintenance costs, greater reliability, and improved operating flexibility. Efficiency is the area that is most directly affected by potential improvements in the other areas, with there typically being a trade-off between flexibility and efficiency.

Advanced gas turbines have recorded combined cycle efficiencies—at baseload—of more than 60%. GE, Siemens, Alstom, and Mitsubishi have all achieved this in their commercial test plants. This represents a massive rise on top efficiencies of 50% to 52% in the early 1990s.

The latest generation of gas turbines (H-class, J-class) were initially conceived with greater efficiency as the key goal, but greater operating flexibility is increasingly emerging as the key battleground between the original equipment manufacturers. Flexibility refers to fast-start capabilities and higher part-load efficiencies, which are increasingly important attributes in liberalized power systems with a growing share of intermittent sources of supply, such as renewables.

Gas Production and Consumption Trends

Global production of natural gas increased by 82% during the 2000–2010 period, mainly to meet growing power generation needs, with the share of space heating and other applications declining gradually.

North America is both the largest producer and consumer of natural gas. Within this region, the United States—as a result of its expanding production of shale gas—has been the world’s largest producing country since 2009, overtaking Russia. This will enable the country to become independent of LNG imports and drive a greater expansion of gas-fired power generation in the region.

Europe is dependent on imports of gas, primarily from Russia, but also from North Africa and increasingly from the Middle East through LNG. Future imports will also come from other territories, such as the Caspian region. China and India are increasingly dependent on imports of LNG to meet their burgeoning gas needs.

LNG Export and Import Trends

The vast majority of the world’s LNG importation facilities are located in Europe, North America, and East Asia (mainly Japan and South Korea). The gas supplying these terminals is liquefied mainly in the Middle East, Africa, and Southeast Asia (mainly Indonesia and Malaysia).

The strongest future expansion in LNG regasification terminals is expected for China, which has numerous projects under construction and in the planning stages. More facilities are also expected for Japan, as the country needs to replace lost nuclear output. The United States, meanwhile, is converting some of its import terminals to export use to find overseas markets for its growing production of unconventional gas.

Qatar is the world’s largest producer of LNG, representing more than 25% of global LNG exports in 2010. Australia, however, is expected to challenge Qatar’s position with numerous export schemes under way to tap into the country’s expanding reserves.

Competitive Analysis

GE is the undisputed leader of the global gas turbines market, having started commercial gas turbine manufacturing in 1949 and offering machines for a wide variety of applications, including the oil and gas industry. The company has been more successful during the economic downturn, supported by its own financing arm providing project finance, which has been a boon for developers during the financial crisis.

Siemens is the second-place company and is gradually increasing its global reach with more extensive manufacturing and licensing agreements outside Europe. Alstom and Mitsubishi Heavy Industries (MHI) vie for the third position, but MHI’s stronger position in the emerging markets of Asia has led to the Japanese firm pulling ahead of its European rival recently.

Fuel Mix Trends

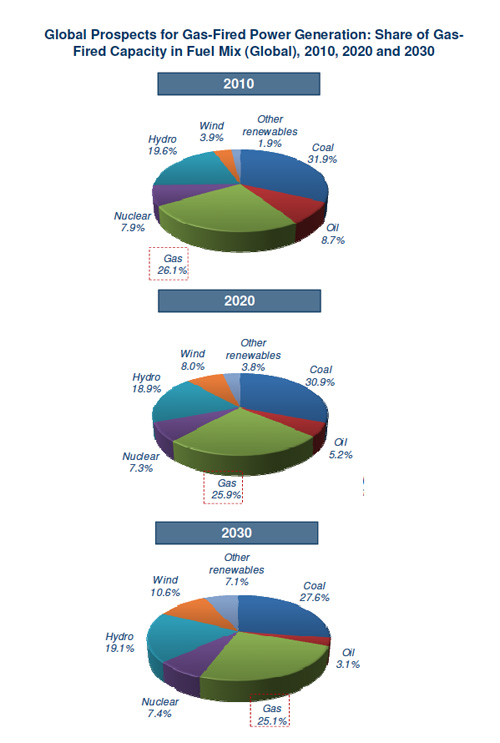

Due to rapid growth in renewable energy—supported by subsidies and preferential access to the grid in many markets—the share of gas in the global fuel mix will decline over time, albeit only marginally (Figure 2). Despite attempts to gradually decarbonize power supply, fossil-fired electricity will still account for 55.8% of installed capacity by 2030. This compares to a share of 66.6% in 2010.

2. Gas will maintain its current place in the fuel mix through 2030 as increasing renewables replace oil and coal. Courtesy: Frost & Sullivan

The relative proportions of the thermal fuels are changing over time. The share of gas in the conventional thermal power capacity mix will gradually expand, rising from 39.1% in 2010 to 41.7% in 2020, and 44.9% in 2030.

Conclusions

The prospects for gas-fired power generation are excellent. Driven by the decommissioning of aging coal plants in the developed world and the growing availability of natural gas from new pipeline schemes, expanding LNG development and a boom in the production of unconventional gas, installed capacities of gas-based plants are forecast to rise strongly across all regions of the world.

This is in stark contrast to coal-fired power, where the bulk of the growth will be driven by China and India, and where a combination of the threat of tougher regulation, carbon markets, CCS uncertainty, and high engineering, procurement, and construction costs deter investors from building new plants.

The leading regions for gas-fired power plant orders during the current decade will be the Middle East and China, with the market being sustained by burgeoning demand for new plants in emerging economies, as well as replacement demand arising from decommissioning of old coal-fired power plants, particularly in Europe and North America.

It is probable that in the short term, gas-based plants will also have delays associated with the availability of finance, exacerbated by the Eurozone sovereign debt crisis, which erodes market confidence, and liquidity of the banking sector. Moreover, electricity consumption in many countries of the developed world has still not recovered to pre-crisis levels. However, considering the problems associated with coal and nuclear—where developments have slowed down in the aftermath of the Fukushima accident—gas will benefit, additionally buoyed by its relatively clean-burning characteristics and flexible operating capabilities.

—Harald Thaler is industry director for power generation at Frost & Sullivan.