Exelon to Split Business, Spin Off Generation Segment

Responding to rapid changes in the power industry, Exelon Corp. plans to cleave its business into two publicly traded companies: one comprising its six regulated electric and gas utilities, and the other, which it plans to spin off, comprising its 31-GW competitive generation fleet and customer-facing businesses.

The separation—which the company’s Board of Directors approved on Feb. 21 and Exelon wants to complete in the first quarter of 2022—will give each company the “financial and strategic independence to focus on its specific customer needs, while executing its core business strategy,” the company said on Feb. 24.

If the separation receives the required final approval from Exelon’s Board of Directors, shareholders, and regulators, Exelon anticipates it will establish “the nation’s largest fully regulated transmission and distribution utility company and the largest carbon-free power producer paired with the leading customer-facing platform for clean, sustainable energy solutions.”

More details about each company, including information about senior management teams, board appointments, and company names, will be released in the “coming months.” For now, Exelon President and CEO Christopher Crane and the company’s existing management team are expected to lead Exelon until the separation is complete through a public listing of “SpinCo,” its Generation spinoff.

Exelon Corp. also said it expects shareholders will retain their current shares of the company’s stock and receive a pro-rata dividend of shares of the new company’s stock in a tax-free transaction. “The actual number of shares to be distributed to Exelon shareholders will be determined prior to closing,” it said.

Exelon’s Move Echoes Those By Other Major Energy Companies

During an earnings call on Wednesday, Crane said the “very good strategic move” will better position each business within “its peer set,” allowing the separate companies to tailor “distinct business investment profiles and meeting unique customer needs.”

“Our industry is changing at a rapid pace and our customers expect us to continuously innovate to stay ahead of growing demand for clean energy, evolving business conditions, and changing technology,” he explained. “Now is the right time to take this step to best serve our customers, employees, community partners, and shareholders. These are two strong, distinct businesses that will benefit from the strategic flexibility to focus on their unique customer, market, and community priorities.”

The move echoes similar efforts in recent years by some of the nation’s largest generators to focus on regulated businesses and exit cutthroat competitive markets. In July 2020, Public Service Enterprise Group (PSEG), New Jersey’s giant utility, said it would explore alternatives for its competitive arm PSEG Power to reduce overall business risk and earnings volatility; improve its corporate credit profile; and enhance its environmental, social, and governance (ESG) position. That same month, Dominion Energy moved to sell the bulk of its gas transmission and storage assets for $9.7 billion to Berkshire Hathaway Energy, as well as to cancel the $8 billion Atlantic Coast Pipeline project it was developing with Duke Energy. Dominion said those actions would accelerate its transformation into a “pure-play” power company with zero-carbon generating assets that are anchored in regulated markets.

Other companies that have sought to guard against distress in unregulated markets include Duke Energy and American Electric Power. Another example of a high-profile business separation was the bankruptcy of FirstEnergy Corp.’s competitive arm FirstEnergy Solutions, which has now re-emerged as an independent firm, Energy Harbor Corp.

Exelon Utilities Narrow Focus on Grid Initiatives—Electrification, Distributed Generation

Under Exelon’s current plans, the remaining organization—for now, “RemainCo”—will parent Exelon’s six fully regulated transmission and distributed utilities: Commonwealth Edison Co, which serves northern Illinois, including Chicago; PECO Energy Co., which serves southeastern Pennsylvania, including Philadelphia; Baltimore Gas and Electric Co., which serves central Maryland, including Baltimore; Potomac Electric Power Co., which serves the District of Columbia and other portions of Maryland; Delmarva Power & Light Co., which serves portions of Delaware and Maryland; and Atlantic City Electric Co., which serves portions of southern New Jersey.

Combined, these utilities employ 16,400 workers and deliver gas and power to more than 10 million customers across five states and the District of Columbia. “Exelon Utilities has invested $22 billion over the last four years to modernize the grid and improve customer service, resulting in each utility achieving its best-ever customer satisfaction rating in 2020,” the company said.

“As a standalone transmission and distribution company, RemainCo will continue that performance track record with an additional $27 billion in investment over the next four years to continue modernizing the grid while managing costs and keeping rates affordable,” it said. Each Exelon utility has also launched initiatives to expand transportation electrification and support distributed generation, it said.

Crane on Wednesday also highlighted a business case. The regulatory business “shares the traits of a high-quality, best-in-class utility, strong above earnings growth rate of 6% to 8%,” he said. It offers a “Diversified rate base across seven constructive jurisdictions with almost 100% of our rate base growth covered by alternative rate recovery mechanisms. Best-in-class operations and an attractive [environmental, social, and governance] attributes provide platforms to enable a transition to a clean energy economy without owning the generation,” he said.

Fashioning a Generation Company That Will Thrive Amid Change

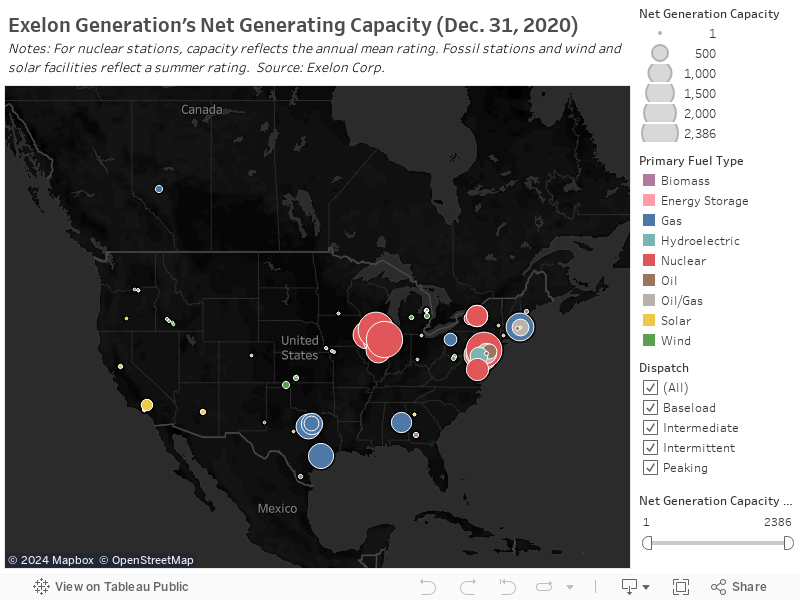

“SpinCo,” on the other hand, will absorb Exelon’s Generation business, which holds 31.2 GW and is already one of the largest competitive power producers in the U.S.

At the end of 2020, the bulk of its installed capacity, 18.8 GW, came from 23 reactors at 13 nuclear plants. Exelon also owns 9.3 GW of fossil plants, primarily natural gas and oil, as well as 3 GW of renewables. Additionally, it contracts another 4 GW of generation. According to Exelon, SpinCo will also hold “the leading share in the [commercial and industrial] market,” where it has “very high customer renew and retention rates.”

Exelon Generation’s Net Generating Capacity (Dec. 31, 2020). Notes: For nuclear stations, capacity reflects the annual mean rating. Fossil stations and wind and solar facilities reflect a summer rating. Source: Exelon Corp.

“It also has the lowest emissions intensity, nearly fivefold less intensive than the next generator, and more than 13 times to 15 times less carbon intensive than the other [independent power producers (IPPs)],” Joe Nigro, Exelon senior executive vice president and chief financial officer, noted on Wednesday. “These attributes are a clear advantage for SpinCo as the Biden administration committed to 100% zero-carbon electricity sector by 2035 to address the climate crisis.”

According to Exelon’s most recent 10-K filing, however, the business suffered a downturn over 2020, owing in part to lower realized energy prices, a reduction in load owing to the pandemic, and increased nuclear outage days. On Wednesday, Exelon reported a full-year 2020 GAAP (generally accepted accounting principles) net income of $589 million for Generation, down substantially from $1.13 billion reported for 2019.

Exelon Evaluating ‘Options’ in ERCOT

Last week, bearing the full brunt of operating in a volatile competitive market, its net income sustained another substantial hit—in the range of $560 million to $710 million—from the mid-February Texas power crisis.

During the unprecedented freeze event, its 1.1-GW Colorado Bend II and 1.1-GW Wolf Hollow II combined cycle gas turbine plants suffered “periodic outages as a result of historically severe cold weather conditions,” it said. “Generation used a combination of commercial paper and letters of credit to manage collateral needs and has posted approximately $1.4 billion of collateral with the [Electric Reliability Council of Texas (ERCOT)] as of Feb. 22, 2021,” it said.

Crane, in the earnings call on Wednesday, suggested Exelon is “evaluating its options” with respect to its ERCOT business. “This loss is unacceptable to us,” he said. As a first step, the company will work with other stakeholders on the future design of the Texas market, he said.

“The second thing is we have to look at the design and the root cause on our specific units, and the issues that we had—anywhere from metallurgical issues to pressure issues to instrument issues. We had taken some action after the Super Bowl event a couple of years ago. But you don’t get compensated to do what we’ve done in other jurisdictions with hardening the plants that have not only energies but capacity payments that allow you to make those investments,” he said.

“So you know, we have to look at it, we want to be a reliable provider. We want to participate in a market that’s designed to not only protect the consumers, the cost element, the reliability element, but allow us to make the investments and operate our plants safely and reliably,” Crane said

A Growth Strategy

In its 10-K filing, Exelon suggests SpinCo will depend on an “optimal structure and composition of its generation assets” for growth, and that it will explore “wholesale and retail opportunities within the power and gas sectors.” A key strategy is to “ensure appropriate valuation of its generation assets, in part through public policy efforts, identify and capitalize on opportunities that match supply to customers as a means to provide stable earnings, and identify emerging technologies where strategic investments provide the option for significant future growth or influence in market development.”

But how SpinCo will be structured appears to be still under discussion. Exelon executives noted on Wednesday that while conversations are ongoing with rating agencies, they expect SpinCo will remain “investment grade.”

“It will continue to have a disciplined financial policy focused on optimizing cash flows to support the balance sheet, invest in clean energy solutions and return value to shareholders,” Nigro said.

Meanwhile, the composition of Exelon’s generation assets is notably also in flux. In December 2020, the group agreed to sell a significant portion of its solar business to an affiliate of Brookfield Renewable Partners, including 360 MW in operation or under construction at more than 600 sites across the U.S. Completion of the $810 million transaction is slated to close in the first half of 2021. Exelon, which said proceeds from the sale would be used for general corporate purposes, also noted it plans to retain “certain solar assets,” primarily its 242-MW Antelope Valley solar installation in California.

Generation Retirements on the Horizon

More changes to Exelon Generation’s portfolio may be on the horizon. On Wednesday, it said that “to maintain the generation fleet’s legacy of safety, operational excellence and financial stewardship, the company will retire uneconomic assets that negatively affect its ability to provide a reliable source of clean power to tens of millions of American homes and businesses.”

But so far, of its fossil fleet, only two gas-fired units at the Mystic Generating Station (Units 8 and 9, a combined 1.7 MW) are slated for retirement in May 2024. Exelon moved to retire the units in August 2020 after the Federal Energy Regulatory Commission (FERC) denied Exelon’s complaint alleging ISO-New England failed to follow its tariff for transmission security.

The company has been much more vocal about its economically distressed nuclear fleet. Exelon outlined a long list of risks and concerns for its substantial nuclear fleet, even as Crane on Wednesday highlighted “another very good year” for its nuclear plants, which generated 150 TWh with an average capacity factor of 95.4%—“second only to last year’s performance in fleet history,” he said. (POWER highlighted Exelon nuclear group’s performance and achievements last year, including it completion of 12 refueling outages in fewer days than planned, despite formidable COVID-19 restrictions).

Exelon in August 2020 moved to permanently retire two Illinois plants, the 2.3-GW Byron nuclear plant (Figure 1) in September 2021 and its 1.8-GW Dresden plant in November 2021, after they failed to clear PJM’s 2021–2022 planning year auction. On Wednesday, it said its 2.3-GW Braidwood nuclear plant in Illinois is also “showing signs of economic distress, in a market that does not currently compensate them for their unique contribution to grid resiliency and their ability to produce large amounts of energy without carbon and air pollution.”

And while all of the 2.3-GW LaSalle nuclear plant’s capacity cleared PJM Interconnection’s 2021–2022 planning year auction, Exelon has also “become increasingly concerned about the economic viability of this plant as well in a landscape where energy market prices remain depressed and energy market rules remain fatally flawed,” it said.

Exelon in September 2019 permanently shuttered its Three Mile Island nuclear plant in Pennsylvania, having failed to obtain policy reforms to keep it open. Illinois, however, enacted the Future Energy Jobs Act in December 2016 (it went into effect in June 2017), which helped keep Exelon’s Clinton and Quad Cities plants running. Exelon also strongly backed New York’s Clean Energy Standard, a measure that became effective in April 2017, to preserve the at-risk Nine Mile Point, FitzPatrick, and Ginna reactors in upstate New York. And in 2018, New Jersey also enacted zero-emission credits (ZECs) to bolster profitability of the Hope Creek plant, which is owned by PSEG, and Salem, whose output Exelon owns jointly with PSEG.

A Landscape Rife with Uncertainties

A key concern for Exelon is if FERC’s December 2019 Minimum Offer Price Rule order in PJM will undermine the continuation of the Illinois and New Jersey programs, it said on Wednesday. Exelon has backed a Fixed Resource Requirement in those states through which Exelon’s nuclear plants would be removed from PJM’s capacity auction, it noted. Meanwhile, it is also backing a comprehensive energy package in Illinois.

“The Governor [J.B. Pritzker] has called for passing an energy bill this session that protects our nuclear fleet, grows renewable energy, and supports customers and job creation. We expect the legislative process to ramp up in the coming weeks and months,” said Crane.

Nigro on Wednesday suggested SpinCo is uniquely positioned because it mostly operate in states that have or are considering ambitious clean energy goals. “The company will continue to be a leading advocate for clean energy policies aimed at preserving and growing clean energy to combat the climate crisis,” he said.

Exelon is also supportive of the Nuclear Powers America Act of 2019, a bill introduced in April 2019 in Congress, which expands the current investment tax credit to existing nuclear power plants. Kathleen Barrón, executive vice president of Exelon’s Government and Regulatory Affairs and Public Policy, on Wednesday also noted the company is “working with folks in Washington” to bolster development of a national clean energy standard, as well as to shape federal carbon legislation.

Efforts related to a “carbon tax dividend approach” currently focus on ensuring “the proper design is included in the sense that we need something that is going to be cognizant of the customer impact, but also aggressive enough to address the challenge of the climate crisis,” she said. Barrón, however, acknowledged that federal efforts “take time to enact,” which is why Exelon’s focus remains at a state level.

Nigro said that despite “uncertainties” that could impact SpinCo’s future, “such as legislation in Illinois, the next PJM auction, and potential federal carbon legislation,” SpinCo will continue to focus on its “strong investment-grade rated balance sheet supported by stable free cash flows, which we see in the different scenarios we are currently considering.”

Exelon has “a strong record of cost management, with announced savings of more than $1.1 billion since 2015 and that cost discipline will not change,” he explained. “We will continue to seek fair compensation for the zero-carbon attributes, while maintaining the discipline to retire on economic assets and opportunistically monetize others.”

—Sonal Patel is a POWER senior associate editor (@sonalcpatel, @POWERmagazine).