Coal Plants Challenged as Gas Plants Surge

European carbon trading is gradually pushing down coal-fired capacity factors, and operating costs are rising. The U.S. may not have a carbon market, but increasing regulatory requirements are having the same effect on coal-fired generation capacity factors and operating costs. In the meantime, gas-fired assets are enjoying increased usage and lower unit costs.

Looking at the past several years of operational performance, utilization, and cost data across the North American and European thermal power generation markets, some trends are very clear.

Last year, we noted in our 2010 industry trends forecast that coal generation had clearly fallen from favor in the European electric market, as shown by several years of historical data since the advent of carbon trading—under the EU Emissions Trading System (ETS)—which began in 2005. In the same European markets, gas-fired combined-cycle plants saw increased levels of utilization and corresponding cost reductions on a nonfuel operations and maintenance (O&M) basis, as costs were spread over more production. Our perspective at HSB Solomon Associates LLC (Solomon) was that the North American market could learn from the carbon trading experiences in Europe and be better prepared when similar changes hit our markets.

One year ago, it seemed likely that some sort of carbon trading or carbon tax might move ahead in the U.S. markets. Now, with the fall 2010 elections behind us, a cap and trade or a carbon tax seems unlikely to move forward in the near term; however, that does not mean we are returning to the status quo as we knew it even five years ago. Lessons learned from the European carbon market experience and historical data research provide valuable information to North American plant operators.

Even without cap and trade or carbon taxes, energy supply decisions continue to be driven by the realization that carbon will be more tightly controlled—if not legislatively, then by U.S. Environmental Protection Agency (EPA) regulations. As a result, industry is adapting. In Europe, before the ETS went into effect, European generators began changing strategic direction to prepare for ETS implementation. In both the U.S. and Canadian markets, coal generation owners have begun announcing asset retirements. In a recent Internet search, it was easy to find at least 10 generation companies across North America that have already announced decisions to shut down older coal-generating units. Coal-unit retirement dates across North America ranged from 2015 through 2022. From a strategic planning perspective, the emissions control conversion costs for smaller, older coal units are proving to be uneconomical.

The economic downturn that began in 2008 clearly disrupted some market trends; however, as the situation stabilized through 2009, some prior trends continued along their expected paths while others strengthened dramatically.

Other market pressures continue to evolve. Natural gas prices remain relatively low across the U.S. and Canada, due mainly to advanced drilling techniques and large shale gas development, while nuclear projects that seemed to be enjoying a renaissance have also been delayed or cancelled.

Asset Utilization Reversed

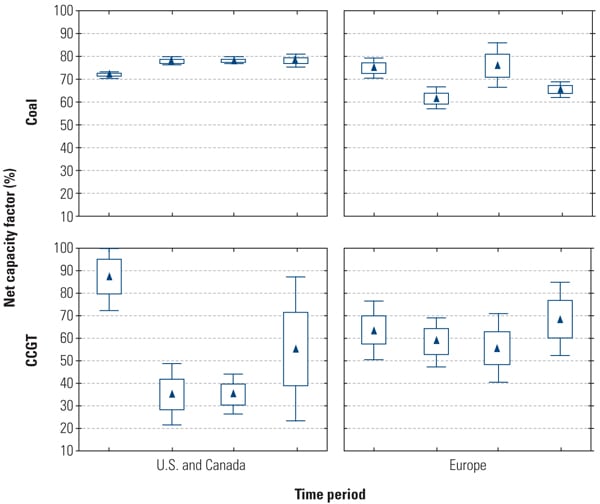

In Europe, several factors converged on coal generation beginning in 2005 with the carbon ETS. These changes accelerated through the market as renewable capacity grew in Europe and as fuel prices became more volatile. Even with the 2008–2009 economic downturn, combined-cycle gas turbine (CCGT) assets significantly ramped up utilization from 48% net capacity factor (NCF) in 2006–2007 to 65% NCF in 2008–2009, while coal units were out of service or running at lower loads due to economic dispatch (Figure 1).

|

| 1. Gas use is rising, coal use is not. This chart shows two-year net capacity factor by region and by power generation technology (coal-fired and combined-cycle gas turbine [CCGT]). The four “time periods” are 2002–2003, 2004–2005, 2006–2007, and 2008–2009. The mean is shown as an icon, plus and minus one standard deviation is represented by the box, and 95% of the data are covered by the end points on the lines. Source: Solomon Associates |

The “spark green spread” overtook the “spark brown spread.” In fact, at times, the spark green spread was negative, a price signal to European coal operators to leave their units out of service. For this analysis, the spark green spread represents the net revenue for gas turbine generation, which is the difference between the market price of electricity and the natural gas fuel cost, adjusted for the generation conversion efficiency and additionally adjusted for the costs of carbon emissions allowances. The spark brown spread is the net revenue for coal generation, which is the difference between the market price of electricity and the coal fuel cost, adjusted for the generation conversion efficiency and additionally adjusted for the costs of carbon emissions allowances.

NCFs in European coal plants have oscillated over previous time periods, and the 2008–2009 values were no different. However, there appears to be an underlying trend in increased utilization. The range of NCF variation is increasing over time. If this trend continues for the next two-year time period, coal NCFs should be in the 78% range.

For U.S. and Canadian markets, coal units hit peak utilization in 2006–2007 at 79% NCF and sustained that level through the 2008–2009 economic slowdown. Combined-cycle plants in the U.S. and Canada showed an upturn in utilization from a low of 35% in 2004–2005 to a mean of 55% NCF in 2008–2009, but this included a wide range of NCF variation, depending on which market the CCGT was located in.

Because most economists expect an extended economic recovery, we anticipate that utilization of European CCGTs and coal units will grow over the next two years at a moderate pace. The only notable impact in Europe may come from a return of volatile fuel prices like those seen in 2007 and the first half 2008.

No significant change is expected due to emissions restrictions during this period, because the current five-year ETS period expires at the end of 2012. Carbon allowance allocations in the next ETS phase (2013–2020) will determine whether carbon allowances introduce significant signals to European electric markets post-2012.

For U.S. and Canadian markets, where several older coal units have been identified for retirement, we expect the coal units remaining in service to be pushed even harder for production. At the same time, these remaining coal units will be dealing with new or upgraded emissions control equipment, adding to plant complexity, cost, and potential availability challenges as utilization constraints.

Availability and Reliability Performance

Most power generating assets seem to perform better when they are operated consistently, and European CCGTs were no exception. After four years of running at nearly 14% equivalent unavailability factor (EUF), the 2008–2009 data show that European CCGTs settled in at 8% EUF, a significant improvement. European coal units saw lower availability during 2008–2009 (22.5% EUF), which was as poor as the two-year period of 2004–2005, when the ETS commenced. Significantly, the years that the EUF for European coal plants was in the high-20s were also 2005 and 2008.

If any coal plant operators have not yet found their world changing, just look again at the European coal experience: European markets have experienced significant turmoil, and generators are still struggling to find ways to best deploy their coal assets in a carbon-constrained environment. Solomon’s experience is that only the best performers are capable of adapting to changing conditions in a year or two. Many take far longer.

U.S. and Canadian coal operators have fared somewhat better than their counterparts in Europe, although the market signals (specifically, a carbon price signal in the form of cap and trade or a carbon tax) in North America have been much less of a factor than in Europe. While North American coal plant operators enjoyed a two-year EUF of 12.2% back in 2002–2003, the EUF numbers have slowly crept through the 13% to 14% range and now are up to a two-year average of 17%.

Consider the changes that have occurred in the North American coal units in the past six years. Have you switched or been blending fuels? Have you added scrubbers or selective catalytic reduction systems? It appears that even those changes have led to nearly a 5% increase in EUF. It is apparent that the range of EUF performance for North American coal units is spreading slightly, meaning that some have already shown adaptability in the face of change, while others may still be struggling.

Even with increased utilization during 2008–2009, CCGT operators in the U.S. and Canada have also experienced a wider range of availability performance. The new, higher EUF two-year average is 17%. Generally, North American CCGTs don’t have higher capacity factors than those found in Europe, so we expect to see availability performance remain within a wide range.

Operating and Maintenance Costs

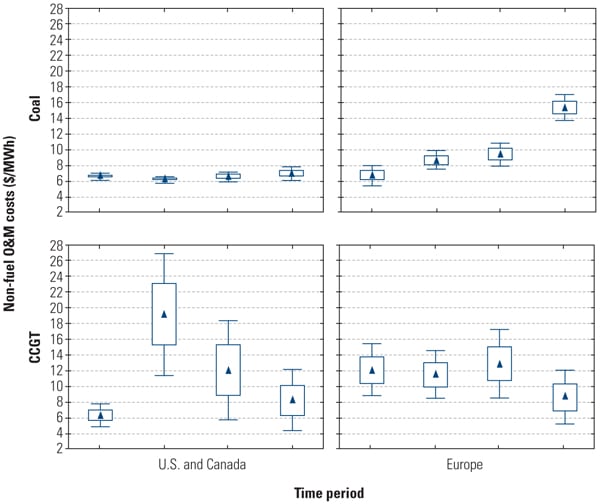

The cost of European coal-fired generation jumped dramatically in the past few years as operators responded to the new operating scenarios and as coal units encountered new maintenance challenges. Nonfuel O&M costs for European coal plants have risen quite dramatically, moving from approximately $9.50/MWh to $15.40/MWh between the 2006–2007 period and the 2008–2009 period. That’s a 62% increase—all after the ETS was put in place (Figure 2). These changes came with significant changes in market price signals both in carbon ETS markets and in fuel price volatility.

|

| 2. Coal costs increasing. This chart shows inflation-adjusted non-fuel O&M spending for the same time periods, regions, and technologies shown in Figure 1. Note that European coal-fired generation cost increases correspond to decreasing capacity factors. Source: Solomon Associates |

Coal generation in the U.S. and Canada has seen nearly constant inflation-adjusted costs over the past eight years. Data for the 2008–2009 time period show the highest values in the trend period, which can be explained partly due to increasingly complex emissions control installations or upgrades.

As more smaller, older coal plants are retired, the remaining coal-fired plants will be required to increase electricity production. At the same time, those same plants will continue to be retrofitted with emissions control equipment and be subjected to increased regulatory control. As plant complexity increases, we anticipate an increase in electricity production cost. We expect these factors will cause the range in plant availability and cost performance to widen in the future. Some plants will adapt quickly, while others may take two, three, or four years or longer to adjust to their new operating and regulatory environment.

There were no surprises with European CCGT cost trends; as utilization went up, costs per MWh went down. Even though CCGT plants in North America have seen a wide range of utilization, many CCGT plants are working under long-term service agreements, so major maintenance costs are somewhat steady, keeping overall O&M costs in a similar, consistent range.

Many Lessons Learned

The data appear to say that the period of baseload coal generation leading the world in capacity factor and low cost of production is coming to an end, and not only for European coal plants. Combined-cycle operators in North America soon expect to see utilization factors like those experienced recently in Europe, as a result of low natural gas prices and rising costs of coal-fired generation.

In our experience, most plant owners and operators believe they have the fuel-shifting situation “under control,” but they either fail to adapt quickly when their business is hit by big changes (such as carbon controls), or they let the smaller changes (the effect of closing smaller coal plants) slip through without taking notice.

Maintaining good data is cheap. Failing to adapt quickly is really expensive. Keep your eyes on a balanced set of performance numbers, dig in, and learn from other markets and assets.

Many lessons have already been learned. It is important to realize that historical data can be used to drive our business forward, to make us better planners, and to make us better prepared as change inevitably comes. For instance, do you know the availability impact expected when adding new environmental equipment to your plant? How has the move from baseload operation to perhaps load-following or weekend cycling changed your O&M practices? Have you set new operating and performance targets for your assets and plant teams based on this new operating environment?

Research by Solomon has quantified statistical relationships between changes in maintenance spending and the corresponding time lag in reliability degradation. Research showed that equivalent forced outage rate variations became increasingly volatile as both “underspending” and “overspending” differences became more severe. The difference was that typically in overspending situations, reliability problems already existed, whereas in underspending situations, there was a time lag before reliability problems surfaced. This research indicated a lag of approximately two to three years from initial underspending before reliability would change for the worse.

During the 2008–2009 economic slowdown, some of our client companies were quick to adapt, using this maintenance spending lag information to constrain spending and defer projects. They understood that reliability would “hold” for two to three years; now, spending recovery plans are under way. Remember the “pay me now or pay me later” adage: It is impossible to starve your assets and expect pacesetter reliability performance over the long run. Understanding this truism is key for properly managing your core business assets.

The same adage can be used in reverse. Understanding maintenance spending deferrals and their corresponding impact on reliability performance can be useful toward the end of asset life. Generating companies are increasingly looking for data on winding down major maintenance spending on coal assets that are nearing the end of their service life, while managing reliability performance and expectations from those assets in their waning years.

Change is just around the corner. If you have not yet experienced significant change, it is looking for you. Keep your eyes open, because if you are not ready and do not adapt quickly, your company’s performance will suffer—not just this year, but potentially for a few years to come.

— Anthony J. Carrino ([email protected]) is senior consultant and Richard B. Jones, PhD ([email protected]) is director of statistics and risk modeling, power generation for HSB Solomon Associates LLC.