Ukraine Looks Beyond Russian Gas

For years, tensions have been brewing between Russia, which provides about a quarter of the natural gas consumed in the European Union (EU), and neighboring Ukraine, a country through which 80% of those exports travel via pipeline. Ukraine, which depends on Russia for all its gas supplies, has protested what it considers Gazprom’s inflated gas price hikes and unfair fines; meanwhile, it too has raised tariffs for gas shipped across its territory. Russia has accused Ukraine of not paying its gas-incurred debt and of illegally siphoning off supplies destined for Europe. This March, in an effort to diminish its reliance on Russian gas, Ukraine found a new supplier.

Erupting disputes have twice left parts of Europe in the cold, with countries such as Bulgaria, Germany, Greece, Hungary, Romania, and Slovakia enduring a total natural gas shutoff from pipelines running from Russia through Ukraine. In 2006, Russia turned off all gas exports to Ukraine for three days; in 2008, it cut shipments by 50%; and in 2009, a renewed debt spat led to a total disruption of supply, which lasted more than 13 days.

A resolution was temporarily reached, as former Ukraine Prime Minister Yulia Tymoshenko and former Russian Prime Minister (and now President) Vladimir Putin negotiated a new contract covering the next decade—until the Ukrainian 2010 presidential election.

Stemming from the political storm that ensued in Kiev after that 2009 agreement, Tymoshenko was charged with abusing power for ordering Ukraine utility Naftogaz to sign the gas deal with Russia in 2009, which was allegedly detrimental to Ukraine’s interests, and subsequently was sentenced in October 2011 to seven years in jail. Current Ukraine president and former Tymoshenko ally Viktor Yushchenko testified against her in a trial that was bemoaned by the EU and the U.S. as “politically motivated.” Tymoshenko’s release from prison for medical treatment was being discussed in early April this year, a move analysts saw as a weak effort by the Ukraine to mend relations with the EU.

Meanwhile, a new spat arose between Ukraine and Russia in 2010: Ukraine disputed how much gas it would import from Russia, citing diminished demand as a result of the economic recession, and Gazprom insisted Ukraine fulfill its contractual obligations and buy quantities of gas agreed upon in 2009.

In the latest development, Ukraine announced plans this March to sign a contract with Germany’s RWE energy firm to import Russian gas through Slovakia using reverse-flow technology. Rejecting allegations that the plans are a ploy to force Gazprom to discount supplies, Ukraine Prime Minister Nikolay Azarov told German newspaper Die Welt that even though Ukraine buys much more gas than Germany does, it has to pay a much higher price, as negotiated in the 2009 contract. Buying Russian gas from a German company would be cheaper than buying it directly from Russia, he said.

The amount Ukraine proposes to buy from RWE is an estimated 3 million cubic meters of gas per day—miniscule compared to the 100 million cubic meters per day it consumes from Russia, analysts note, but it is the first, critical attempt by Ukraine to reduce its dependence on imports from Gazprom, they say.

Over the rest of Europe, countries hard-hit by interruptions in gas supply have also been seeking ways to wean themselves from reliance on the Ukraine trade route. The future of European gas markets is generally dependent on three new gas pipeline projects. Two, the Nord Stream and South Stream pipelines, are majority owned by Gazprom, and the third, the Nabucco project, is supported by Europe and Turkey.

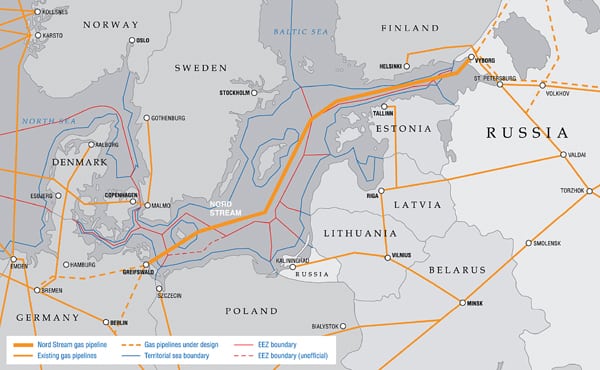

Despite some European hostility to the project owing to increased European energy dependency on Russia, the first of the two Nord Stream 1,224-kilometer (km) offshore pipelines directly connecting Russian gas reserves and energy markets in the EU began transporting gas in mid-November last year (Figure 3). The second line, which runs parallel to the first, is expected to come on stream in the last quarter of 2012. Each line has a transport capacity of roughly 27.5 billion cubic meters (bcm) of gas a year.

|

| 3. First in line. The first line of the two Nord Stream 1,224-kilometer gas pipelines running in parallel through the Baltic Sea from Vyborg, Russia, to Lubmin, near Greifswald, Germany, began transporting gas in mid-November last year. The route crosses exclusive economic zones of Russia, Finland, Sweden, Denmark, and Germany. The second line will come on stream later this year. Interest in the €15 billion project surged following the Russian-Ukraine gas crisis of 2009, which shut off gas delivery to Europe for almost two weeks. Courtesy: Gazprom |

Completion of the Gazprom and ENI South Stream pipeline—which proposes to carry 63 bcm of gas per year through the Black Sea to Bulgaria, and farther, to Greece, Italy, and Austria—is expected by 2015, though there are many doubts about its feasibility.

Some analysts view the €10 billion project as a direct competitor of the EU-backed Nabucco line. The Nabucco line has been planned to run from the eastern border of Turkey to Baumgarten in Austria via Bulgaria, Romania, and Hungary. Preliminary analyses had cited Iran and Turkmenistan as sources of gas supplies for the conduit, but it was later decided the pipeline would carry gas from the Caspian region, notably from the Shah Deniz field in Azerbaijan, to Europe by 2017. This pipeline was intended to diversify Europe’s current natural gas suppliers and delivery routes and create a southern corridor free from Russian interests.

The 3,900-km Nabucco pipeline—whose shareholders include Austria’s OMV, Hungary’s MOL, Romania’s Transgaz, the Bulgarian Energy Holding, Turkey’s Botas, and Germany’s RWE—would reach a capacity of 31 bcm a year, meeting just 5% of Europe’s gas needs. In mid-March, however, developers proposed a route half the length of the original project, running from the Turkish-Bulgarian border to Austria.

—Sonal Patel is POWER’s senior writer.