Renewable Growth Soars, Buoyed by Distributed Generation

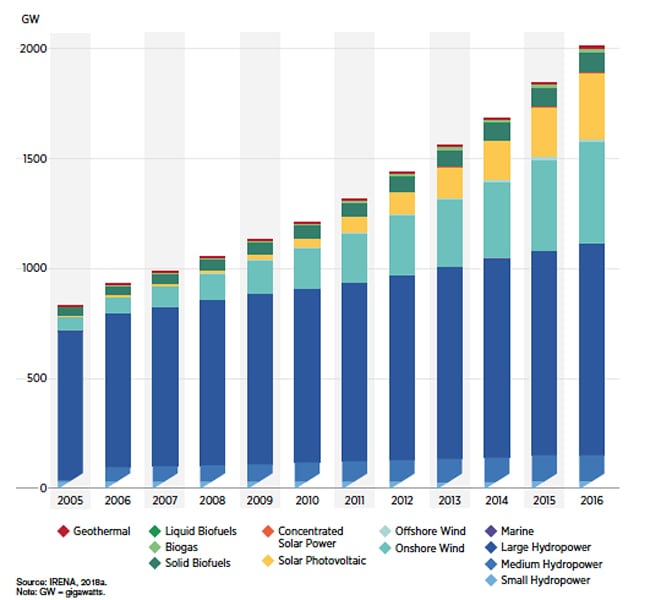

Nameplate renewable capacity surged to more than 2,000 GW worldwide at the end of 2016, constituting more than 28% of total generating capacity (Figure 6). Most (56%) was hydropower, followed by wind (23%), and then solar, mostly from photovoltaic (PV) at about 15%. According to the International Renewable Energy Agency (IRENA) the expansion was fueled by dedicated policies and technological advancements that have, in turn, driven costs downward. While the agency projects soaring growth of all renewables for power, one sub-sector making notable headway is distributed generation (DG), which allow the production of energy near the point of use.

In a report released this April titled Renewable Energy Policies in a Time of Transition, IRENA suggests that the modular nature of DG systems allows for rapid deployment, and typically, it is the most “cost-effective energy option for rural off-grid locations.” Because DG enables local self-consumption, it can deliver savings both to the end consumer and the system as a whole.

But growth of the new sub-sector is still pegged to regulatory and pricing policies, including administratively set feed-in tariffs (FITs) or feed-in policies (FIPs), as well as net metering and net billing schemes, which allow DG system owners to reduce or eliminate the variable charge portion of their electricity bills, the agency noted. As with larger scale renewable installations, DG FIPs/FITs are typically designed to encourage distributed PV. Net metering provides compensation to DG owners in energetic terms (credit in kWh), and the credit can be applied to offset consumption of electricity within current or future billing cycles. In net billing, compensation is monetary, and an owner can consume power from the DG system in real-time and send excess generation to a utility’s grid (though unlike net metering, banking kWh in a billing cycle to offset future consumption is not allowed). The world has increasingly adopted both policies. The number of countries adopting net metering and net billing grew from 9 in 2005 to 55 to 2017.

According to the report, distributed PV has achieved the most significant growth. Investments soared to $67.4 billion in 2015, up 12% from 2014. Developing countries largely led this surge, armed with effective financing, innovative business models, and as distributed PV costs generally declined. IRENA also noted, however, that the subsector has opponents that are pushing for reformulation of net metering schemes. Some utilities, for example, argue that net metering fees paid to prosumers for excess power unfairly transfer costs to the utilities.

“Well-designed net metering schemes that encourage self-consumption can drive prosumers to a more system-friendly behaviour. Regulation should consider appropriate design elements, such as the length and timing of the netting period and the actual value of net excess generation,” the report says.