Power in Africa: Prospects for an Economic Foothold

To sustain unprecedented economic growth, lift hundreds of millions out of poverty, and attract investment, African countries are taking bold steps to expand electricity infrastructure. Are the continent’s efforts pragmatic or merely ambitious, driven by political will?

If there is one region in the world that has been overlooked for its potential to revitalize power industries around the world—which, of late, have suffered a downturn owing to generation oversupply, changing environmental priorities, and shifting public perception—it’s Africa. The continent harbors a growing population—yet, more than 591 million Africans have no access to electricity. Its energy potential remains vastly unexploited, and in some countries, infrastructure lags woefully behind other global regions. However, African economies are proving resilient to global economic shocks and gaining momentum. According to the African Development Bank (AfDB), real output for all countries on the continent is estimated to have increased 3.6% in 2017 (Figure 1) and could accelerate to 4.1% in 2018 and 2019, fueled by “faster growth and buoyant capital markets,” and a general interest from institutional investors and commercial banks, which are constantly seeking profitable returns.

Today, many African countries are on the brink of structural transformation in a bid to create more jobs and reduce poverty. Across Africa’s five sub-regions, East Africa is slated for the fastest growth, as public investment, manufacturing, and construction activity kicks up. In North Africa, where economic progress slowed after political shuffling in part due to the 2011 Arab revolution, short-term growth is underpinned by an uptick in oil prices and financial reforms. Southern Africa’s growth is also expected to soar on the back of better performance of commodity exports in South Africa, Angola, and Zambia, as well as an expansion in agriculture, mining, and services. In West Africa, increased oil production and agricultural output will help consolidate gains made in 2017, accelerating growth. The AfDB projects economic underperformance only in Central Africa, even with the recovery of oil prices.

But this growth will be dependent on several factors, and nothing may be more crucial to the continent’s economic advancement than a much-needed surge in access to electricity. By 2016, Africa had installed only 168 GW of power capacity, and progress on the transmission and power distribution front has been “painfully slow, making the generated electricity unusable for productive purposes,” said the AfDB. And, its electricity deficit remains enormous. “Per capita consumption of energy in Sub-Saharan Africa (excluding South Africa) is 180 kWh, against 13,000 kWh per capita in the United States and 6,500 kWh in Europe,” the multilateral development finance institution noted in its African Economic Outlook 2018, which was released this January. That access to power is also disparate across the continent: In North Africa, it was 98% in 2014 but 26% in East Africa, and it varies greatly within countries, where urban consumers are better served than rural consumers.

Several experts told POWER that the power supply scarcity has several implications for economic growth, the most serious of which is that power is particularly expensive. The average effective cost of power, reflecting both high-cost utility power and reliance on emergency backup generation during frequent power outages, to manufacturing enterprises on the continent is close to $0.20/kWh—four times more than in some other regions of the world. On average, power outages occur a quarter of the year, and this has been crippling for productivity. About 60% of firms operating in Africa consider infrastructure (power shortages and costs, and transport bottlenecks) “the most binding constraint they face in their daily operation,” noted the AfDB.

Rise of the Independent Power Producer

As is the case for other developing regions around the world, the continent suffers a “Catch-22”: It desperately needs infrastructure to speed up development and attract investment but building that infrastructure itself requires a massive infusion of investment. According to the World Bank, the cost of addressing the needs of sub-Saharan Africa’s power sector stands at about $40.8 billion a year—equivalent to 6.35% of Africa’s gross domestic product.

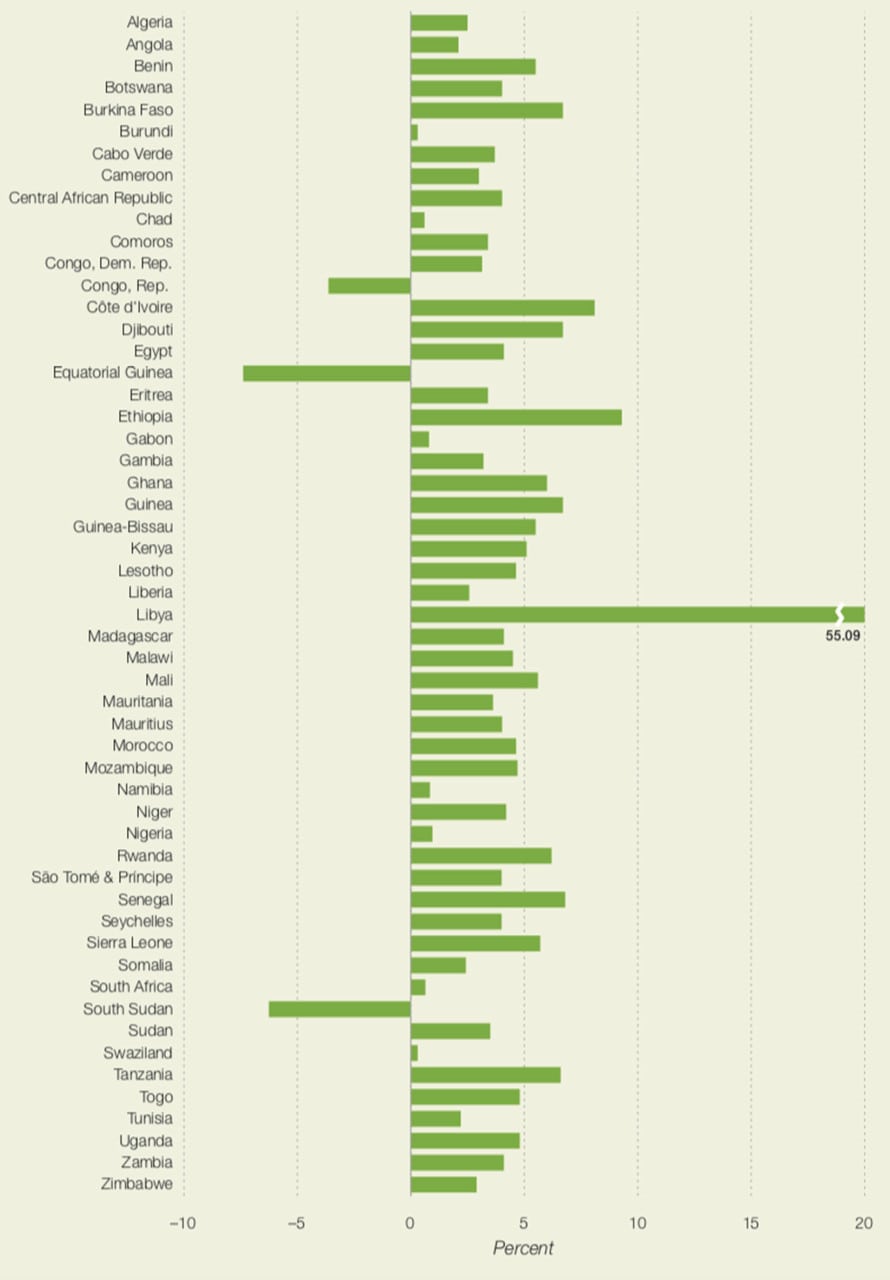

Public utilities have historically offered major sources of new investment, with funding gaps partly filled by official development assistance and development finance institutions. But as a 2016 World Bank report notes, many state-owned utilities have suffered “years of underspending on maintenance and expansion,” which is tied to “the inability of many customers to pay for electricity services and underpricing” (Figure 2). The high costs and low revenues at African utilities have resulted in “serious shortcomings in operational efficiency, high costs of small-scale operation, and over-reliance on expensive oil-based electricity generation,” it says.

|

| 2. A deficit crisis. A 2016 analysis of state-owned utilities in 39 countries in sub-Saharan Africa by the World Bank showed only those in the Seychelles and Uganda were fully recovering their operational and capital costs. Utilities covered operational costs in only 19 countries, and only four countries also covered half or more of capital costs, based on new replacement values of current assets. The study concludes that utilities in the region operate at a major deficit (an average of $0.12/kWh), hampering their ability to effectively provide universal energy access. Source: The World Bank: “Making Power Affordable for Africa and Viable for its Utilities,” 2016 |

Faced with growing power demand, and the need to tackle high electricity losses and capacity shortages, by 2016, at least 24 sub-Saharan countries had enacted electricity sector reforms. All of the countries corporatized electric utilities. Two-thirds also set up regulatory bodies, and more than a third paved the way for independent power producers (IPPs, Figure 3). According to Romain Py, who heads up transactions for African Infrastructure Investment Managers (AIIM)—Africa’s largest private equity investment manager focused exclusively on infrastructure—over the last few years, more IPPs have reached financial close for larger projects, among them Azura-Edo, Cenpower, Amandi, and Albatros Energy. That trend will likely continue in other locations, notably in West Africa, where countries like Benin, Burkina Faso, Mali, and Sierra Leone have embraced the IPP model, he told the African Utility Week media in April.

|

| 3. A pioneering project. In July 2016, Avon Peaking Power, which is jointly owned by ENGIE, Legend Power Solutions, Mitsui & Co., and The Peaker Trust, began commercial operation of a 670-MW open cycle gas turbine power plant north of Durban in South Africa. The project supplies power to state-owned utility Eskom under a 15-year power purchase agreement. That project and its sister plant, the 335-MW Dedisa plant in Port Elizabeth, paved the way for the independent power producer model in power-strapped South Africa. Courtesy: ENGIE |

According to the AfDB, however, a glaring risk thwarting IPP success is that in some countries, even when laws are enacted, they may not be implemented. That may affect credibility of guarantees offered by off-takers to IPPs, with whom IPPs negotiate and sign power purchase agreements, and increase project costs and off-take tariffs. Another factor that hampers private investment is that some African countries don’t have well-defined infrastructure programs and bankable project pipelines, and the lack of planning often means that the private sector cannot assess costs and risks or set down long-time plans. Infrastructure projects, which require heavy, long-term investment, are also vulnerable to poor governance and political risks, such as elections and other political considerations, as well as corruption (see sidebar “Political Risk and Corruption”).

Political Risk and CorruptionWhile the African Development Bank (AfDB) forecasts remarkable economic growth for nearly all regions on the continent, it also urges “cautious optimism,” pointing to several risks. The dangers include a possible downturn in the global appetite for oil as the shale oil and gas revolution reshapes markets; a tightening of global financial conditions; protectionist sentiments in countries like Tanzania; and policy uncertainty, which could affect investor confidence. As significant are political risks, which have assailed nearly every country on the continent historically and continue to lurk, particularly in countries that have recently held or plan to hold elections. Since the 1980s—as several countries adjusted to their post-colonial status—political rather than economic and social considerations determined where infrastructure projects were executed. As the AfDB noted in a 2018 report, “In many African countries, airports, paved roads, and power plants are built to yield political benefits in the regions of powerful politicians, and end up as ‘white elephants.’ ” The organization said that political bias in project selection may also exist, leading to a large number of unfinished projects as new governments fail to complete them given their lack of economic returns (or benefits to constituents). Corruption, which entails abuse of public power for private gain, is also a conspicuous problem. Typically, it involves giving priority to projects that generate higher private material and political gains over projects with higher social returns. In 2013, as measured by the Corruption Perception Index produced by Transparency International, eight of the world’s 20 most-corrupt countries were in sub-Saharan Africa. In a January 2018 working paper, the Massachusetts Institute of Technology’s Center for Energy and Environmental Policy Research noted that most sub-Saharan African countries have implemented electricity reforms to curb corruption and improve efficiency, introducing independent regulation and private sector participation, along with unbundling of vertically integrated functions of the power industry. However, reforms designed to create genuine competitive markets have been difficult. The researchers conducted econometric analysis of the performance of reforms in 47 African countries between 2002 and 2013. They found the reform experience “lagged behind the anticipated outcomes and has led to extensive political backlash against reforms.” Higher electricity prices have been a source of political resistance, “reinforced by the awareness that elections can be won or lost because of electricity prices.” The authors concluded that corruption weighed heavily on three indicators: technical efficiency, access rates, and economic performance. The study also showed that creation of independent regulators and private sector participation can both enhance utility performance and have wider economic benefits. |

The Development Boost

Despite these risks, Africa’s power sector appears to have the financial backing of major institutions. The AfDB, for example, is exploring new financing mechanisms to de-risk the cost of large-scale infrastructure projects through Africa50, a new infrastructure investment platform, and The New Deal on Energy for Africa, a partnership effort with the lofty goal of providing 100% access in urban areas by 2025. The AfDB notes that the effort will require 160 GW of new capacity, 130 million new on-grid connections, and 75 million new off-grid connections—and a total average annual investment of $30 billion.

Power Africa, an initiative approved by the U.S. Congress in February 2016, meanwhile, seeks to increase the continent’s installed generation capacity by 20 GW by 2020. In August 2017, it said it had helped facilitate the financial close of 80 private-sector power transactions worth $14.5 billion that could generate up to 7.2 GW. Over the last decade, China has also emerged as a key investor, accounting for more than 30% of new capacity additions in sub-Saharan Africa, and, according to the International Energy Agency (IEA), Chinese contractors are set to build more than 17 GW of new capacity through 2020, nearly half of which is hydropower-focused (Figure 4).

|

| 4. Parched for power. Chinese engineering and construction giant SinoHydro in March 2018 commissioned the two-unit Kariba South Expansion project on the Zambezi River, adding 300 MW to Zimbabwe’s grid. Before the project came online, the country suffered a 600-MW shortfall, which it sourced—at a steep cost—from Eskom in South Africa, Caho-bassa of Mozambique, and SNEL in the Democratic Republic of Congo. Hatch served as the owner’s engineer for the project. Courtesy: Hatch |

Pooling Power

While large swathes of Africa remain electricity poor, some countries are heavily investing in their power sectors with ambitions to become net power exporters. Ethiopia, for example, will nearly quadruple its electric power capacity when it completes the 6,450-MW Grand Ethiopian Renaissance Dam (GERD), a $6.4 billion project that is under construction on the Blue Nile River. Paired with the 1,870-MW Gilgel Gibe III Dam, which it completed in 2015, the country plans to export surplus power to its neighbors, including Egypt, Djibouti, and Sudan, and boost revenues by up to $1 billion a year. Similar plans have been proposed for the Grand Inga—a hydropower project in the Democratic Republic of Congo (DRC) that could eventually produce 50 GW.

While development of large-scale projects like these has historically been hampered by a lack of transmission and investment, five regional power pools created since 1995 could make them possible (Figure 5). The pools include the Central Africa Power Pool (CAPP); the Comité Maghrébin de l’Electricité (COMELEC) for northern countries; the Eastern Africa Power Pool (EAPP); the Southern Africa Power Pool (SAPP); and the West Africa Power Pool (WAPP). According to Callixte Kambanda, manager of Energy Policy, Regulation, and Statistics at the AfDB, the pools offer significant opportunities to allow countries to meet growing demand and utilize comparative resource advantages. SAPP, for example, the oldest and most advanced power pool on the continent, offers short-term energy markets that work to tamp down prices and encourage investment. The system is already highly integrated, and some smaller countries in the region reap significant benefits from the integration, he said.

|

| 5. Regional power pools. Regional energy integration has become increasingly significant to attract investment, for energy security, and to reduce costs through economies of scale. The pools include the Central Africa Power Pool (CAPP); the Comité Maghrébin de l’Electricité (COMELEC) for northern countries; the Eastern Africa Power Pool (EAPP); the Southern Africa Power Pool (SAPP); and the West Africa Power Pool (WAPP). Source: “Atlas of Africa: Energy Resources, 2017,” African Development Bank/The Infrastructure Consortium for Africa |

Distributed Generation and Fast Power

On the flip side, owing to transmission and distribution constraints, a number of project developers have set up interesting business models for smaller, off-grid power generation applications to ensure that Africa’s underserved population will still have electricity. The Rocky Mountain Institute, for example, helped Rwanda and D.Light set up a blueprint to enable the purchase of solar lighting units through pay-as-you-go options. Standard Microgrid has developed a community-managed off-grid micro-utility business model, using proprietary technology to monitor the systems remotely and manage demand (Figure 6). A number of major players, too, are active in the decentralized power market in Africa, including ABB. A microgrid project ABB installed at Robben Island—the isolated land mass off the coast of South Africa’s Western Cape, where Nelson Mandela spent 18 years in prison—consists of a 500-kW PowerStore battery, a 667-kW solar photovoltaic plant, and a 500-kVA diesel generator.

|

| 6. A utility in a box. In April 2016, Standard Microgrid delivered a containerized “utility-in-a-box” solution to Mugurameno Village, Lusaka Province, Zambia. The project provides energy services to 32 homes and businesses as well as energy for high-quality lighting to the Mugurameno Basic School, which educates 500 students. Project developers are now looking to install the solution at 150 sites by 2021. Courtesy: Standard Microgrid |

Large equipment manufacturers like Siemens Energy are also banking on a large-scale distributed generation expansion in Africa. This November, the company rolled out a mobile 44-MW aeroderivative gas turbine, projecting that the continent is poised to see its greatest increase of power generation in the next two decades, and that, based on emissions, efficiency, and environmental concerns, by 2040 Africa’s use of natural gas will increase by more than 800% to fuel a quarter of all the continent’s generation. The African market displays a “more imminent need—to quickly improve the African power infrastructure by providing highly flexible solutions and fast order-to-execution projects in the form of small and medium-sized power plants,” the company said. “The combination of these diverse requirements calls for market and customer-specific solutions in order to truly answer Africa’s call for electricity.” Distributed generation with light industrial and aero-derivative gas turbines, in particular, makes sense for the continent’s needs because it allows for fuel flexibility, fast-response times, and low maintenance downtimes. “At the same time, they can help to optimize network operation by providing voltage support, or reactive power and inertia to a local grid,” it added.

“Fast power” solutions are much-needed for emergency supplies in parts of Africa that have been cut off from the national grid, or stricken with drought or other fuel shortages, as a number of African delegates told POWER at a business briefing hosted by the U.S. Trade and Development Agency in November. Along with representatives from Siemens’ SGT-A45 Mobile Unit, suppliers present at the briefing included EthosEnergy, Fluor, Modec International, PW Power Systems, and Tiger Industrial Rentals. Also notably present were gas turbine heavyweights Caterpillar’s Solar Turbines, which offers mobile power units ranging from 5 MW to 15 MW, and GE, which has a specialized global fast power division dedicated to urgent and mobile power.

An Evolving Generation Mix

Though Africa has the world’s lowest per capita energy consumption—it consumed only about 3.3% of global primary energy in 2015—the continent harbors 18% of the world’s uranium, 7.5% of the world’s proved gas reserves, 7.6% of its proved oil reserves, and 3.6% of global coal reserves. In 2014, 80.5% of its installed power generation capacity was comprised of thermal fuels—mostly oil, coal, and natural gas—and the bulk of the remainder (18.7%) was hydro.

Fuel shares around the continent have begun to shift, however. Projections forecast that the role of coal—which is one of the cheapest sources of electricity production—will decline, even in South Africa, as gas for power and industry, and liquid-petroleum projects for transport and power, develop. While the continent has only one nuclear plant—the 1,940-MW Koeberg in South Africa’s Cape Town—several other countries, including Kenya, Egypt, and Namibia, are interested in introducing nuclear.

The continent’s newest coal plants—Eskom’s Kusile and Medupi projects, which are each 4.8-GW multi-unit facilities—point in a new direction for environmental controls. The first of six 800-MW units at Kusile, which came online in September 2017, is Africa’s first plant to implement wet flue gas desulfurization technology (it uses a GE Power system). The six-unit Medupi Plant, which should be completed by 2021, features six air-cooled condensers, returning demineralized water for reuse in the turbine steam cycle. When it begins operation, it will be the largest dry-cooled coal-fired power plant in the world, according to engineering firm SNC Lavalin.

The largest gain could come from renewable energy, however, of which the continent theoretically has an inexhaustible resource, including from solar, wind, geothermal, biomass, hydro, and tidal. Africa has already installed several noteworthy projects, including the world’s largest concentrating solar power plant in Morocco in March 2017 (Figure 7) and the world’s largest single-turbine geothermal plant at Olkaria in Kenya. A number of its financial backers, including governments, multilateral agencies, and investors, have shown an increased focus on renewables. The IEA in late 2017 suggested that installed capacity of renewables in sub-Saharan countries could almost double from around 35 GW to 60 GW, but only if it can resolve financial and political issues.

|

| 7. A beam over Africa. The 510-MW Ouarzazate Solar Power Station (also called the Noor Power Station) in Morocco’s Drâa-Tafilalet region comprises two parabolic trough facilities (the 160-MW Noor I, which came online in 2016, and the 200-MW Noor II, which was commissioned in January 2018). The final phase to be completed in October 2018 will bring online the 150-MW Noor III concentrated solar power plant, which uses central towers and salt receiver technology. According to MMYPEM, which is commissioning the Noor III salts for a consortium of Spanish firms TSK, ACCIONA, and SENER, the project will be the world’s second utility-scale tower with molten salt storage. Courtesy: MMYPEM |

Even though there are “enough examples to show it works,” as Mustapha Bakkoury, chairman of the board of Morocco’s Solar Energy Agency reportedly said during an Africa CEO Forum panel in April, a major obstacle is “believing that it is feasible.” ■

—Sonal Patel is a POWER associate editor (@sonalcpatel, @POWERmagazine)