Photovoltaics Overshadow Concentrated Solar Power

Though much newer, solar photovoltaic technology has gained a much larger market share than concentrated solar power, even though the latter promises thermal storage and the potential to be almost fully dispatchable.

As solar technologies, both solar photovoltaic (PV) and concentrated solar power (CSP) are often discussed collectively, along with solar thermal and solar fuels. But the difference between the two power generating technologies that have evolved independently for decades is significant: CSP harnesses irradiative solar energy, which is easily transformed into heat through absorption by gases, liquids, or solid materials and is then converted to mechanical energy and finally electrical energy, while PV uses solar radiation, which is essentially a flux of elementary particles that promote photoreactions and generate a flow of electrons.

Technology-agnostic solar industry observers note that both technologies are today approaching “grid parity” as solar utilities around the world develop them with “relative” success. But solar PV has vastly overtaken CSP’s market share, and will prevail for a long time. At the end of 2012, the world’s PV installations totaled 32 GW—compared to a cumulative 2.9 GW of CSP capacity, the bulk concentrated in Spain (68%) and the U.S. (28%).

Of the 1,176 MW of utility-scale solar capacity in the U.S. at the beginning of 2012, about 43% came from concentrated thermal technology while 57% came from PV—but PV accounts for 72% of solar projects under construction. And while 2012 was a banner year for the world’s CSP sector, marking the most installations—more than 1 GW—over a 12-month period in the technology’s 135-year history, experts forecast that growth spurt will be short-lived, overshadowed primarily by plunging prices of PV panels and a variety of hurdles that are stalling the still relatively small sector.

At least 7.3 GW of new CSP capacity is in various stages of preconstruction development in the U.S., the Middle East and North Africa, and in China, India, and Australia. Saudi Arabia, notably, will lead a longer-term charge with its ambitions to generate 75 to 110 TWh by 2032, which could require the installation of 25 GW of capacity in Saudi Arabia alone. Yet, PV’s growth is slated to soar to a staggering 41 GW by 2014—an expansion that will be undertaken by “all major world regions,” according to market research firm IHS.

A Cost Disparity

The paramount reason for this market share disparity is cost. According to the International Energy Agency, CSP received a minuscule 7% share of public research and development (R&D) funding from the Organisation for Economic Cooperation and Development countries for renewables in 2010, compared to 36% for solar PV and 28% for wind. This is why, some experts say, innovation in the CSP field has been limited and patent rates declined significantly between 1977 and 2000.

Moreover, CSP is a capital-intensive technology whose initial investment is dominated by solar field equipment and labor. Accounting for 84% of electricity generation costs of CSP, initial investment requirements range from $2,500 to $10,200/kW, depending on capacity factor and storage size. In contrast, solar PV’s initial investment costs range from $3,500 to $6,000/kW. The remaining 16% for CSP typically consists of fixed operation and maintenance costs, which average $70/kW per year, while variable maintenance is limited to about $3/MWh.

Cost concerns are also possibly the most plausible reason why investment in CSP is substantially lower than for PV: In 2011, the sector garnered just $18 billion worldwide, while PV got $125 billion.

A Vulnerable Sector

As with most dawning technologies, the economic crisis hit CSP particularly hard as governments reconfigured subsidies and imposed austerity measures, forcing developers to rethink projects or convert to PV. For Spain, the only European Union member to have developed a CSP production sector, and a country that spurred the world’s concentrated solar technology revival in the second half of the 2000s, CSP’s future has all but been eclipsed by both a moratorium on financial aid imposed by the Spanish government earlier this year and the government’s intention to retroactively redefine plant remuneration terms.

At the end of 2012, though Spain commissioned 17 new plants to bring its total CSP capacity up to 1.95 GW—and all within the last five years—the future of at least six new plants hangs in the balance as Spanish CSP developers have been forced to turn to other countries to develop their technology (Figure 1) and bring down production costs on their own. Protermosolar, the country’s CSP industry association, bemoans the government’s measures that it says came before the nation’s CSP sector could become as competitive as other generation sectors.

|

| 1. In a new light. Spain led the world with 1.95 GW of installed concentrated solar power (CSP) capacity at the end of 2012 and generated 5,138 GWh from 42 plants: 37 parabolic trough, three tower, and two Fresnel plants. Spanish companies are also putting up a number of the CSP plants worldwide, like Abengoa SA’s $2 billion Solana parabolic trough plant, which came online near Gila Bend, Ariz., this October. That 280-MW plant built with a $1.45 billion U.S. federal loan guarantee uses a thermal storage system to produce power for six hours at full power. Courtesy: Abengoa SA |

Restructuring efforts also established the Korea Electric Power Exchange (KPX) to serve as the system operator and coordinate the wholesale electric power market. KPX continues to regulate the cost-based bidding-pool market and determines prices for energy sold between generators and the KEPCO grid. KEPCO is the main retailer and, apart from large industrial consumers, is the sole purchaser of electricity from the pool. Since 2004, however, regional districts have been allowed to bypass KEPCO and the power pool by buying power directly from independent generators.

Today, KEPCO and independent generators (which produce about 8% of the country’s power) are overseen by the Ministry of Trade, Industry, and Energy (MOTIE), an entity that took on a trade policy role and replaced the Ministry of Knowledge Economy (MKE) in March 2013. MOTIE works in consultation with the Ministry of Strategy and Finance, the country’s six generation companies, and KEPCO. The country’s nuclear power sector is regulated by the Nuclear Safety and Security Commission (NSSC).

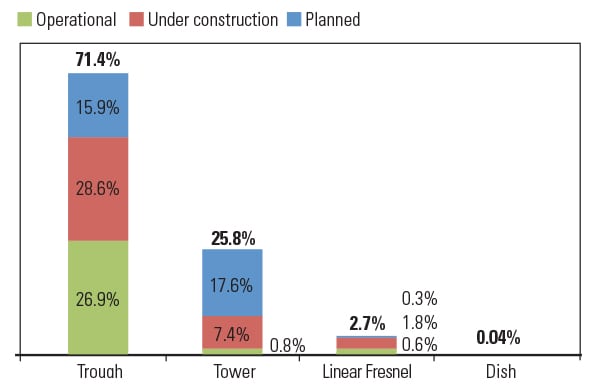

The Evolution of CSPSince the world’s very first concentrating solar thermal systems were developed in 1878 by French inventors Augstin Mouchot and Abel Pifre, the fundamental quest for solar thermal energy developers of a great variety of designs and applications has been to increase working temperatures. Today, four different technology approaches focus the sun’s energy onto mirrors to create steam to drive a turbine that generates power: ■ Trough systems, which use large, U-shaped (parabolic) reflectors that heat oil-filled pipes running along their center, or focal point, as high as 750F. The parabolic trough is today the most mature of CSP technologies and forms the bulk of current commercial plants (Figure 2). ■ Power tower systems, also called central receivers, which use many large flat heliostats to track the sun and focus its rays onto a tower-mounted receiver. The receiver heats a fluid, such as molten salt, to temperatures of up to 1,050F to make steam or store energy for days before being converted into electricity. ■ Dish/engine systems, which use mirrored dishes nearly 10 times larger than a backyard satellite to focus sunlight onto a receiver that is integrated into a high-efficiency “external” combustion engine outfitted with thin tubes containing hydrogen or helium gas. ■ Linear-Fresnel reflectors, which approximate the parabolic shape of trough systems but use long rows of flat, or slightly curved, mirrors to reflect the sun’s rays onto a downward-facing linear, fixed receiver. Mouchot’s and Pifre’s inventions were based on dishes, though the parabolic trough was invented soon after, in 1884, by American engineer John Ericsson. In 1897, another American engineer, Frank Shuman, demonstrated a solar engine that worked by reflecting solar energy onto collector boxes filled with ether—which has a lower boiling point than water—and later, an improved system using mirrors to reflect solar energy onto boxes filled with water. He also developed a 560-W low-pressure steam turbine and, in 1912, set up the world’s first solar power thermal power station in Meadi, Egypt, using parabolic troughs to power a 60- to 70-horsepower engine that pumped 6,000 gallons of water per minute from the Nile River to nearby cotton fields. In contrast, PV’s evolution has been much more recent. The first photovoltaic technology capable of providing sufficient power to electrical equipment—a primitive version with an efficiency of only 4% that cost $300/W to produce—was invented in 1954 by the Bell Telephone Laboratories. Solar PV got its boost with the space age, after the U.S. launched its first satellites into space. Finally, in 1970, a solar cell was developed that tamped down the price of energy from $100/W to $20/W—a breakthrough that made it realistic to use solar applications for residential use.

|

More Stringent Requirements

Added to cost concerns are a number of obstacles. According to the U.S. National Renewable Energy Laboratory (NREL), generation-weighted averages for total land area requirements range from 3.2 acres/GWh per year for CSP towers to 5.3 acres/GWh per year for Stirling dish CSP systems; large (>20 MW) PV systems require between 2.8 and 3.4 acres/GWh. But not only must CSP plants be installed at larger scales to be cost-effective, they also need higher levels of irradiance—which means siting is limited in the U.S. to the Sunbelt—and access to water. That also means they can take years to permit and connect to the grid.

In fact, CSP needs a tremendous amount of water for cooling processes—up to 3,780 liters/MWh for Fresnel installations and 2,835 liters/MWh for solar towers, compared to just 19 liters/MWh for PV—and this in turn has environmental implications in arid and semi-arid areas. However, at least four large plants with dry cooling technology—which promises to reduce water consumption by more than 90% (but increase generation costs by 5%)—have come online this year alone: three Integrated Solar Combined Cycle (ISCC) plants in Hassi R’mel, Algeria; Kuramayat in Egypt; and Ain Beni Mathar in Morocco; plus the 100-MW Shams 1 in the United Arab Emirates—a POWER Top Plant (see story on p. 34).

Significantly, PV has a number of standalone smaller applications, attributable to its low maintenance requirements and low costs. One reason for PV’s extensive market growth has been its suitability for residential power supply, points out pro-solar community resource group, the Principal Solar Institute. “In fact, photovoltaics have found a place meeting a broad spectrum of energy needs. While large-scale photovoltaic projects are competing with traditional utilities to meet consumer demand at one end of the spectrum, smaller residential projects are working to replace them at the other end,” it says.

The Promise of Thermal Storage

Perhaps CSP’s saving grace could be its most formidable advantage over PV, which is its ability to store thermal energy for up to 16 hours. Innovations are expected in all four CSP technologies (see sidebar) and throughout the system value chain as research and development is focused on improving dispatchability. According to Romeu Gaspar, founder of energy consulting firm X&Y Partners, “Dispatchability will be increasingly important when and where renewable energies achieve high penetration rates, so two things can happen: CSP becomes a commercially viable solution before a commercial PV storage system is developed, carving its own market segment; or the PV industry quickly solves the storage issue and becomes the solar technology of choice.”

Other experts point out that CSP is also better suited to hybridization with complementary solar and fossil fuel primary energy sources. And it can be applied to a number of niche industrial processes to desalinate water, improve water electrolysis for hydrogen production, generate heat for combined heat and power applications, and support enhanced oil recovery operations.

That means CSP isn’t going to disappear from the market altogether, the Principal Solar Institute says. The future of CSP will depend on its stronghold at the utility scale, “where no amount of PV cost-reduction is expected to overcome its inherent technology advantages.” ■

— Sonal Patel is a POWER associate editor (@sonalcpatel, @POWERmagazine).