While the overall economy is down, the effort to add renewable energy resources in the U.S. continues to push project development forward. For renewables, the lowlight of 2008 was certainly the credit crisis, which resulted in a stunning loss of capital. Until last year, the primary driver for financing was the available tax equity, most of which is now out of the picture. The need for tax equity and sponsor equity has never been greater. However, earlier this year, as part of the American Recovery and Reinvestment Act of 2009 (ARRA), renewable tax incentives and loan guarantees were passed that focused on renewable energy and transmission projects. These are expected to free up debt equity for large-scale projects. Thousands of applications are expected to pour in for grants that will be paid on wind farms that start construction before the end of 2010 and begin operations before the end of 2012. The stimulus-authorized U.S. Department of Energy (DOE) loan guarantee program provides up to 80% of the project cost. This is expected to support guarantees of $80 billion to $110 billion.

The growth potential for renewable energy is tremendous and is being driven by overwhelming government policy support. In January, as part of ARRA, the renewable energy production tax credit (PTC) was extended an additional three years. Uncertainty over these tax credits was creating some reluctance to move forward with proposed project activity. With more predictability, the likelihood of increased renewable energy projects increases. In addition, renewable energy developers now have the option of taking a 30% investment tax credit in lieu of the PTC.

Other factors will drive continued development as well. At present, 28 states have passed or plan to implement renewable portfolio standards. These actions mandate that up to 20% of total electricity be supplied by renewable energy sources over a defined period of time. In addition, as part of proposed CO2 cap-and-trade legislation, a national renewable electricity standard is being suggested. With carbon legislation looming on the horizon, the cost of renewable energy is likely to become more competitive with traditional forms of generation.

None of these factors alone is expected to launch widescale project activity. However, a combination of one or more of these key drivers is likely to create the spark for significant construction activity.

Wind Is Blowing Other Renewables Away

Wind energy is by far the leading renewable energy source moving forward today. For the U.S. wind industry, 2008 was a record year. In fact, more than 8,500 MW were installed, bringing wind’s total capacity to more than 25,000 MW in the U.S. This represents a 50% increase over 2007. It has been estimated that wind capacity could grow 19% annually over the next several years. In fact, during the past year the U.S. surpassed Germany as the nation with the largest amount of installed wind capacity.

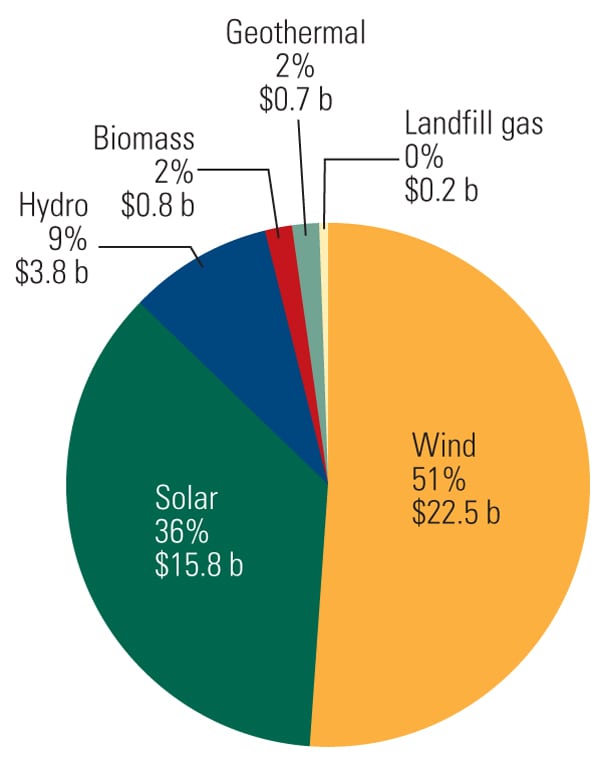

Although 2009 is considered to be a sleeper year for wind projects because of the economy, a respectable amount of wind capacity remains under construction as we write this in late October. Currently, Industrial Info is tracking 5,212 MW of U.S. wind projects under construction, representing more than $8.8 billion of investment. Beyond 2009, an additional 100,000 MW have been proposed for construction kickoff between 2010 and 2015. Of this, 24,000 MW of project activity have been earmarked for a 2010 construction start. Of course, some projects will not move forward to fruition. Many of these projects are facing financial barriers, and transmission constraints in some parts of the country will be the death knell for others.

Incentives Expected to Lower Solar Costs

Solar energy represents a huge potential domestic energy resource for the U.S., particularly in the Southwest, where the deserts have some of the best solar resource levels in the world. In the past, the majority of solar generation was installed for remote distributed energy use. For this application, photovoltaic (PV) panels have been the best-suited technology. As utilities put more effort into solar generation projects, solar thermal technologies, especially concentrating solar power (CSP), are gaining more attention. Currently, there are a variety of CSP technologies that use reflective materials such as mirrors to concentrate the sun’s rays to utilize heat energy for conversion to electricity. (See our solar special report in this issue for a summary of technology options.)

Utility-scale CSP power plants provide the lowest cost and most efficient methods for harvesting solar energy. The U.S. has about 450 MW of proven CSP technology, which has been operating successfully in California for the past 15 years.

Although solar energy is abundant and free, the cost to harness (harvest) it with solar collectors can be significant. As a result, electricity generated from solar energy is currently more expensive than power produced from conventional fossil-fuel power plants. However, studies indicate that even at moderate levels of deployment, large-scale solar power could potentially compete directly with conventional fossil-fuel generation.

CSP construction costs are generally between $3 million and $6 million per MW, and power generation is about 8 to 15 cents per kilowatt-hour (kWh), the lowest of any solar technology. Current goals are to achieve between 4.5 and 7 cents per kWh by 2025. Cost improvements are expected to come from improved designs, economies of scale, volume production, and operation and maintenance cost reductions. Molten-salt thermal energy storage integration can allow for generation from solar energy during bad weather or at night to improve economics.

The cost reductions realized by wind power are a good model for CSP. The initial cost of wind power was high, but it decreased as installed capacity increased. The same trend is expected to develop for CSP.

According to the Western Governors’ Association’s Solar Task Force, the long-term federal investment tax credit and state-based incentives could promote as much as 8,000 MW of solar electric generating capacity by 2015 in the western U.S. Deployment on this scale would also bring down solar costs to a point that it would be competitive with power produced from fossil fuels, according to the report. The task force envisioned half of the deployment coming from central CSP and the other half from distributed PV generation.

According to the DOE, at least 7,000 MW of centralized CSP generation will be built by 2020, and possibly much more.

Currently, more than 50 projects totaling 10 GW of CSP are in the development pipeline in six states, with the majority located in California, Nevada, and Arizona.

All Fuels Considered

Apart from wind and solar energy, other types of renewable energy are also in progress. In fact, at this point more than 47,000 MW are either under construction or in the development stages. This includes more than 35,000 MW of hydroelectric capacity, more than 3,000 MW of biomass-fired energy, and 2,800 MW of geothermal energy. Other types of renewables that are being tracked include landfill gas–to-energy, tidal energy, waste-to-energy, and biodiesel-powered energy resources.

Although the exact fuel mix to supply America’s future energy demand is still being determined, one thing seems clear: With continued government support and solid private investment, renewable energy is poised to play a major role in supplying the future’s electricity.

—Britt Burt (bburt@industrialinfo.com) is vice president, power industry for Industrial Info Resources. IIR (www.industrialinfo.com) is a leading provider of global market intelligence specializing in the industrial process, heavy manufacturing, and energy-related markets.