IEA's World Energy Outlook 2013: Renewables and Natural Gas to Surge Through 2035

By 2035, renewables will hold a 30% share of the global power mix, but only 1% of the world’s fossil fuel–fired power plants will be equipped with carbon capture and storage (CCS), reports the International Energy Agency (IEA) in its newly released World Energy Outlook (WEO-2013).

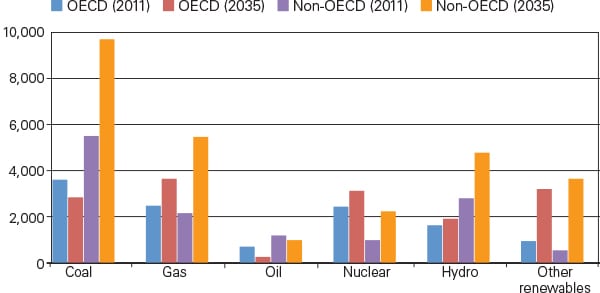

The annual report presents a central scenario in which global energy demand rises one-third by 2035, driven higher by the growing populations and expanding economies of India and Southeast Asian countries rather than by China. Meanwhile, more than half of the projected increase in global primary energy demand will come from the power sector (Figure 1), the agency projects.

|

| 1. The changing face of world power generation by source. The power generation mix (in TWh) in member countries of the Organisation for Economic Co-operation and Development (OECD) and non-members is expected to evolve variedly. Source: IEA |

Coal is expected to remain a cheaper option than natural gas for power generation in many regions, though that could change, depending on policy interventions to improve efficiency, curb air pollution, and mitigate climate change. Coal demand is set to increase 17% by 2035, with two-thirds of that increase occurring by 2020. While coal use will decline by half in Europe (despite current price dynamics) and plateau in China by 2035, India is poised to become the world’s largest coal importer by 2025. In the U.S., coal use is expected to decline by 14%.

Though several initiatives to mitigate climate change are under way—as with the U.S. Climate Action Plan, China’s plans to limit coal’s share in its domestic energy mix, Europe’s debate on 2030 energy and climate targets, and Japan’s discussion of a new energy plan that may or may not include nuclear power—global energy-related carbon dioxide emissions will still rise by 20% by 2035. That means, according to the IEA’s New Policies Scenario, which takes into account the impact of already announced climate change measures and other policies, the world will be on a “trajectory consistent with a long-term average temperature increase of 3.6C, far above the internationally agreed 2C target,” the report says.

Though the global average efficiency of fossil fuel conversion in power plants is forecast to improve by 15%, the IEA makes the significant, if dismal, admission that widespread deployment of CCS technology could stall. Only about 1% of global fossil fired–power plants (about 67 GW) will be equipped with CCS by 2035, mostly in the U.S., China, and the European Union (EU). CCS appears “well-suited” to resolving at least some of the tension between rapidly increasing power demand and the need to limit carbon emissions and local pollution, “yet many significant challenges have still to be overcome,” the agency says. These include the need to “integrate component technologies effectively into large-scale projects, identify viable storage sites and put the necessary financial incentives in place.”

By 2035, natural gas demand will outpace that of any other individual fuel and end up nearly 50% higher than in 2011. Demand for gas will come mostly from the Middle East—driven by new power generation—but also from Asian countries, including China, India, and Indonesia, and Latin America. Power generation continues to be the largest source of gas demand, accounting for around 40% of global demand over the period. New gas plants, meanwhile, are expected to make up around a quarter (or 1,000 GW) of net capacity additions in the world’s power sector through 2035.

Nuclear generation will also increase by two-thirds, reaching 4,300 TWh in 2035, led by China, South Korea, India, and Russia. But demand for nuclear power will be driven mostly by expansion in just a few countries. China accounts for around half the global increase, while South Korea will see the next-largest increase, followed by India and Russia. The prospects for nuclear power are less uncertain than after Fukushima in 2011, the IEA notes. What remains murky, however, is how the sector could be affected by further policy changes, implications of the ongoing safety upgrades for plant economics and public confidence, and notably, the impact of increased competition from shale gas.

Nearly half of the increase in global power generation will be from renewables—and generation from wind, solar, and hydro will make up an expected 30% share of the global power mix by 2035. That will put it ahead of natural gas and just behind coal as the leading fuel.

China will lead the world in renewables installations by 2035, its total renewable output totaling more than in the EU, the U.S., and Japan combined. Overall, the massive renewables increase will likely create challenges, the IEA foresees, raising questions about current market design and its ability to “ensure adequate investment and long-term reliability of supply.”

Electricity prices will also vary, the agency forecasts. By 2035, average Japanese, European—and even Chinese—industrial consumers will pay twice as much for power as their counterparts in the U.S., “which could have important ramifications for competitiveness,” the report says.

The report also notes that substantial investments in the power sector will be required over the projection period to satisfy rising power demand and to replace or refurbish aging infrastructure. By 2035, around 50% of today’s grid infrastructure will have reached 40 years of age, the agency notes. Cumulative global investment could amount to as much as $17 trillion through that period, averaging $740 billion per year. New plants will account for 58% of the total, while the rest will be needed in transmission and distribution networks.

—Sonal Patel, associate editor (@POWERmagazine, @sonalcpatel)