Global Gas Glut

Marcellus Shale gas has increased recoverable natural gas reserves in the U.S. by about a third over estimates prepared a few years ago. Europe is also exploring shale gas as an alternative to problematic Russian gas supplies and low proven natural gas reserves. POWER contributors in the U.S. and UK examine the comparative economic value, public acceptance, and political implications of these massive shale gas reserves.

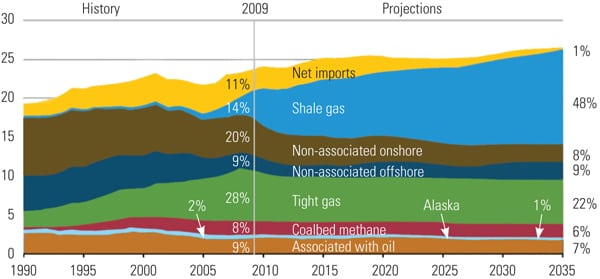

The U.S. natural gas reserves chart looks like a roller coaster. In 1967, the U.S. Department of Energy’s Energy Information Administration (EIA) predicted that proven U.S. natural gas reserves were 293 trillion cubic feet (Tcf), the peak reported at the time. Since that year predictions have slid downward, hitting a low of 164 Tcf in 1994. That very low number sparked a scramble to construct new liquefied natural gas (LNG) import terminals about a decade ago. Then, a few short years ago, advanced drilling techniques made the vast reserves of shale gas more than a mile beneath Earth’s surface accessible. Today, the EIA’s prediction of U.S. proven natural gas reserves is 2,552 Tcf, enough gas to keep the U.S. economy fueled for a century, at the current rate of consumption, and LNG export terminals are under development. The ability to tap even deeper shale gas reserves promises even more startling reserve estimates in the next few years (Figure 1).

|

| 1. Shale gas glut. The U.S. Energy Information Administration predicts that shale gas will become the predominant source of natural gas in the coming years. Units are trillion cubic feet per year of dry gas. Source: EIA, Annual Energy Outlook 2011 |

The rise in predicted shale gas reserves in Europe is similar, but with different consequences. The European Union (EU) is blessed with large quantities of shale gas reserves, although they are not equally distributed across the 27 EU countries (EU27). However, with few exceptions, EU countries are poor in conventional natural gas. Consequently, most of them are beholden to Russian gas pipelines for a large portion of their natural gas needs and will be dependent on imported gas for the foreseeable future. Several countries in the EU have also taken the political position that drilling for unconventional natural gas is environmentally unacceptable and have prohibited such drilling.

Copious amounts of natural gas, from conventional or unconventional sources, will provide significant economic benefits to those countries that can cheaply tap the resource. Not only does the use of natural gas produce half the carbon dioxide emissions of coal combustion, but the cost of production (once the full implementation of expected environmental retrofits to coal-fired plants are considered) also will probably produce reasonably priced electricity for many years, because the plentiful supply of gas should keep prices relatively low in the U.S.

The prospects for the EU are less promising, given that the majority of its gas is imported and the level of enthusiasm for exploiting unconventional gas resources is lower than in the U.S. The EU also faces other legal and political barriers to bringing unconventional gas to market that do not exist in the U.S., such as state ownership of the gas beneath Earth’s crust.

In this special report we discuss the momentous impact of shale gas on the economies of the U.S. and the EU. In our opinion, the immense flow of unconventional gas promises to be a game changer for the global power generation industry. We predict it will undermine the economics of renewable and nuclear projects, providing a path for quicker reductions of carbon and other emissions than expensive retrofits of solid fuel power plants and the means to keep electricity prices in check for years to come. In the U.S., the last “dash for gas,” which ended almost a decade ago, left many combined cycle plants either mothballed or used sparingly when the price of natural gas spiked. Today, long-term, low-cost natural gas will make these plants very valuable for many years into the future.

No question, the gas glut means it’s no longer business as usual for power generators. The effect is one that Joseph Schumpeter called “creative destruction,” a situation in which industries must revolutionize their economic structure from within, necessarily destroying the old one in the process. Those countries that embrace unconventional gas as the natural evolution of the power generation industry and release their grasp on old technologies will benefit greatly. Those that are slow to respond will be severely disadvantaged in the global marketplace.

U.S. Gas Supplies Gush

Looking for some cheap windmills? T. Boone Pickens is selling.

In 2008, Pickens, a longtime guru of gas, hatched a scheme to push windmills for electric power production in order to divert natural gas to power diesel-powered trucks. The plan, which won the enthusiastic support of the Sierra Club, promised a move toward “energy independence” by reducing the use of oil products in transportation.

In May 2008, Pickens ordered 667 windmills with a total capacity of 1,000 MW from GE, a $2 billion order, to equip a wind project in the Texas Panhandle. The project was the centerpiece of the “Pickens Plan.”

But the Pickens Plan, and the man’s status as a darling of wind power folks, quickly crashed on the shoals of an ocean of new natural gas. Within a year, Pickens was trying to unload his wind turbines, which had become twirling white elephants.

Though Pickens has sold out on wind, he’s sticking with gas, earning condemnation from environmentalists who were lauding him in 2008. Now they charge that Pickens might—shockingly—be looking to make a profit from gas. The 82-year-old Pickens, who made his first billion drilling for gas at Mesa Petroleum, told the politics newspaper Roll Call in an interview last May that “you can’t do wind because natural gas is too cheap.”

Gas Is the Game Changer

Pickens is not alone in his renewed enthusiasm for low-cost gas now flowing from shale formations. Many other energy analysts are pondering the implications of the stunning emergence of gas from tight shale. In Pennsylvania, the heart of one of the largest shale formations, the Marcellus Shale, new gas supplies have already lowered energy prices to the state’s consumers, according to a study by Penn State. “From the household perspective, reductions in energy expenditures act like a tax cut for the Pennsylvania economy, increasing discretionary income,” the study said (Figure 2).

|

| 2. Many shale gas opportunities. The Marcellus Shale deposit is principally under New York and Pennsylvania, but that’s not the only region where unconventional natural gas reserves reside. Source: EIA |

This enthusiasm for what was once known as “unconventional” gas has many environmentalists gnashing their teeth, seeing a new dash to gas as a rapid retreat from their favored, but less practical and more expensive, renewables. They have mounted a rearguard action, challenging the environmental impacts of shale drilling and the economics, but neither approach seems likely to slow down the advent of new, low-cost, and abundant supplies of gas.

Gas developers first started employing the new directional drilling technology and hydraulic fracturing, long a staple of conventional oil and gas exploration, only in 2004. When the new approach began to unleash unheard of amounts of gas about three years ago, many adopted a popular sports cliché. “This could be a game changer,” they said.

Today, it seems clear to many, the game has changed. John Rowe, the savvy outgoing CEO of giant electric utility Exelon Corp., told a meeting at the American Enterprise Institute in Washington earlier this year that while coal will remain king of the generating mountain for some time to come, “Natural gas is queen. It is domestically abundant and inexpensive and is the bridge to the future. Because of natural gas, there is no need for expensive mandates and subsidies. Natural gas allows us to compete with China and India.”

During the first decade of this new century, the conventional wisdom was that natural gas had seen its glory days as a major electricity generating fuel, and those days were in the 1980s and 1990s. The decades-long “gas bubble” from the days of federal price controls vanished. Gas prices tended to rise and fall unpredictably. There was serious talk, and serious money, going into importing foreign natural gas into the U.S.

“Shale gas” was a phrase that really hadn’t appeared in the vocabulary of anyone other than geologists. Geologists had long known that massive shale formations across the U.S. contained copious amounts of natural gas, but they didn’t know how to release it. When companies such as Chesapeake Energy put the new and old technologies together, the results were surprising, even astonishing.

Today, shale gas is a staple of newspaper headlines, the subject of short documentary films and long magazine articles, and on economic and regulatory agendas across the U.S. and Europe. In the words of the advertising industry, shale has sizzle. It’s the big new thing. Is it real?

As mentioned earlier, the EIA reports that the U.S. possesses some 2,552 Tcf of potential natural gas reserves. According to the EIA’s Annual Energy Outlook 2011, “Natural gas from shale resources, considered uneconomical just a few years ago, accounts for 827 Tcf of this resource estimate, more than double the estimate published last year.”

As the past decade ended, shale gas was swiftly accounting for a larger share of natural gas production. In a memo to a New York Times reporter in June, Michael Schall, who monitors natural gas for the EIA, wrote, “Prior to 2005 shale gas constituted only 4% of natural gas production and had grown to become 23% of production for 2010. EIA’s continued monitoring of the situation indicates that growth in shale gas production continues and that shale gas has exceeded 30% of total marketed natural gas production through May of this year.”

Independently, the Potential Gas Committee, an industry group run by the Colorado School of Mines, recently estimated U.S. gas reserves of 1,898 Tcf, “the highest resource evaluation in the Committee’s 46-year history, exceeding the previous record-high assessment by 61 Tcf. Most of the increase arose from reevaluation of shale-gas plays in the Gulf Coast, Mid-Continent and Rocky Mountain areas.” As you will read later, this estimate of gas reserves from all sources is about three times that of the EU27, a significant, long-term economic advantage for the U.S.

Have Gas Prices Stabilized?

Gas appears to have overcome its chief obstacle in generating markets: price volatility. In an interview, Chris Ellsworth, who follows natural gas for the Federal Energy Regulatory Commission’s (FERC’s) office of enforcement, said, “Natural gas now has a national market price. Price differences by region reflect only transportation costs, not the underlying gas.” In the past, gas prices varied regionally, complicating the economics of gas a generating fuel. It also fluctuated seasonally, spiking in the winter in response to home heating needs.

According to FERC’s staff analysis, in some areas—particularly the Southeast—gas has become the baseload generating fuel of choice; gas-fired plants are now being dispatched ahead of coal units. Ellsworth noted, “In 2010, we saw natural gas supply and demand meet new records, while natural gas prices remained moderate throughout most of the year.”

According to FERC’s State of the Markets 2010, “Though 2010 natural gas prices were up about 12 percent on average over 2009, they remained well below the levels of previous years. Natural gas demand increased in 2010 and was only partially offset by increased natural gas supply.

“Natural gas storage levels were high for much of the year and reached record levels in November. Outside of early winter 2010 and a few days in June, spot prices at the Henry Hub remained between $3/MMBtu and $5/MMBtu. By the end of the year, prices remained low despite a cold start to the winter.”

One widely used metric for commodity prices is the Goldman Sachs Commodity Index (GSCI). Over the two years between 2008 and 2010, the GSCI doubled. But U.S. natural gas prices were flat. According to FERC, this was because the U.S. gas market is almost entirely self-sufficient, insulated from forces that drive other commodity prices, such as the price of crude oil. Also, noted FERC, “Strong domestic production growth, combined with added pipeline and storage infrastructure, have increased domestic supply and reduced geographic and season price differences.”

Liquid Side Benefits

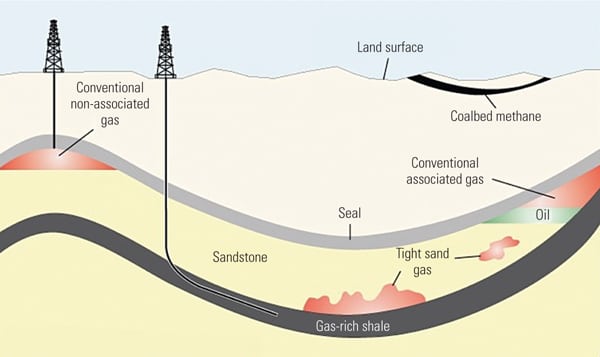

One little-understood aspect of the arrival of shale gas, which drives its economics, is that the gas is often found in conjunction with crude oil or natural gas liquids (NGLs). NGLs are hydrocarbon components of gas that, according to a standard industry definition, “are liquid at surface in field facilities or in gas-processing plants.” They include propane, butane, pentane, hexane, and heptane. Technically, this does not include ethane, which must be refrigerated to become a liquid, but which has great value as a petrochemical feedstock and is generally included in economic discussions of NGLs (Figure 3).

|

| 3. More than just gas. Unconventional drilling techniques allow drilling horizontally at depths of over a mile beneath the surface to follow shale deposits. The wells often deliver liquid petroleum products as well as natural gas, an unexpected economic bonus. Source: EIA and U.S. Geological Survey |

The Bakken formation in North Dakota’s Williston Basin produces copious amounts of crude oil; the same is true of the Eagle Ford formation in Texas. Thanks to the drilling boom in the Bakken, North Dakota has avoided the recession that has plagued the rest of the U.S. over the past four years. According to the EIA, oil production from shale formations has risen from negligible five years ago to 300,000 barrels per day in 2010. The giant Marcellus shale formation under much of New York, Pennsylvania, and West Virginia contains large reserves of NGLs along with the gas. The Eagle Ford and Barnett shales in Texas produce significant NGL volumes along with oil and gas.

Because the oil and the NGLs are worth much more on the market than natural gas, the gas is essentially free. FERC’s Ellsworth made this point in his presentation to the commission earlier this year. Oil and NGLs, he told FERC, have such value of their own that “the breakeven cost for natural gas has fallen to zero.” Both Shell and Dow Chemical in recent months have announced plans to spend hundreds of millions of dollars to build ethylene processing plants to exploit the non-methane shale resources.

Many Policy Implications

The implications for the power generating business of a large, predictable, and economic supply of natural gas are revolutionary. Much of the long and often fruitless discussion over the past 15 years over the roles of coal, uranium, wind, water, and sun is rendered largely irrelevant by copious domestic gas. The endless haggling over how to reduce carbon dioxide emissions in electric generation begins to look feckless.

A recent study by a team from the Massachusetts Institute of Technology (MIT), the fourth in a series by the MIT Energy Initiative examining energy issues, highlights the role that abundant new supplies of gas can play in transforming U.S. energy systems. Says MIT’s Anthony Meggs, a coauthor of the study, “Shale gas is transformative for the economy of the United States, and potentially on a global scale” because it has so dramatically increased the amount of gas that can be produced economically in the U.S.

Abundant, low-cost natural gas has a number of policy implications that may reprioritize capital investment and redirect legislative priorities in the coming years, such as those that follow.

Requires Fewer New Transmission Lines. The need to spend enormous sums to build new long-distance transmission lines to move power from generating sites favorable for wind and sun to load centers may diminish with readily available low-cost gas. (If gas substitutes for new renewables, many gas-fired units built during the 1980s and 1990s, now sitting idle or not operating at peak efficiencies, could march up the dispatch order.) Decades of planning about moving large quantities of gas from Alaska across Canada to the U.S. could wither because of cost versus lower-48 gas.

Locating generation closer to load could also improve reliability and offer greater grid protection against cyber attacks or solar storms.

Eliminates the Need for Carbon Reduction Legislation. One of the most obvious impacts of gas is on emissions of carbon dioxide (CO2) from power generating plants. Using sidelined and under-used gas-fired plants to supplant coal generation makes a quick, low-cost dent in emissions of not only CO2 but also conventional pollutants such as sulfur dioxide, oxides of nitrogen, particulates, and mercury. The MIT report finds that “Increased utilization of existing natural gas combined cycle power plants provides a relatively low-cost, short-term opportunity to reduce U.S. CO2 emissions by up to 20% in the electric power sector, or 8% overall, with minimal additional capital investment in generation and no new technology requirements.”

Because methane has the lowest carbon content of any of the fossil fuels, says the MIT report, “In a carbon-constrained economy, the relative importance of natural gas is likely to increase even further, as it is one of the most cost-effective means by which to maintain energy supplies while reducing CO2 emissions. This is particularly true in the electric power sector, where, in the U.S., natural gas sets the cost benchmark against which other clean power sources must compete to remove the marginal ton of CO2.”

Collapses the Demand for Renewable Technologies. The arrival of shale gas profoundly challenges the rationales for widespread development of renewable energy. Writing in the online journal Salon recently, prominent liberal commentator Michael Lind said, “The arguments for converting the U.S. economy to wind, solar and biomass energy have collapsed.”

The implications of abundant gas have clearly been felt inside the wind energy industry. Columnist Mark Del Franco, who writes for North American Wind Power magazine, recently was critical of Denise Bode, head of the American Wind Energy Association (AWEA), the industry’s Washington lobby, for her inability to win federal renewable energy generating quotas. Del Franco observed “that despite having the legislative and executive branches on its side, AWEA could not get a renewable electricity standard passed before the midterm elections last year.” While critical of Bode, Del Franco cut her some slack: “Bode does not deserve all the blame. She cannot control market factors, such as the drop in demand for power or falling natural gas prices.”

Ends the Nuclear Renaissance Before It Starts. The rise of natural gas also threatens the long-predicted nuclear power renaissance, already stalled by a lagging economy, tight credit markets, and, most recently, the catastrophe in Japan. Low and stable gas prices undercut the chief economic advantage of nuclear plants: low fuel costs. Gas plants also enjoy a major advantage over nukes: low capital costs. If gas is cheap and plentiful, nukes look increasingly less attractive to private investors.

Industry CEOs Favor Gas

A recent survey of more than 700 electric utility executives by Black & Veatch found that gas has overtaken nuclear, wind, and solar as the top “environmentally friendly” generating technology. Last year, Black & Veatch’s survey had gas in third place, behind nuclear and wind, as the technology the industry should push for meeting future environmental requirements.

Abundant shale gas could also bolster U.S. national security and boost U.S. foreign policy objectives. In his Salon article, Lind notes that the new estimates of gas resources in the U.S. undercut both the danger of “peak oil”—the point at which world oil supplies begin declining—and U.S. dependence on oil imports. “Whatever may be the case with Peak Oil in particular,” he writes, “the date of Peak Fossil Fuels has been pushed indefinitely into the future.”

The Baker Institute at Rice University recently released a report, “Shale Gas and U.S. National Security,” arguing that U.S. shale resources will undercut the influence of Russia, Iran, and Venezuela in the world. That’s because the U.S. could soon become an exporter of excess gas in the form of LNG. “The geopolitical repercussions of expanding U.S. shale gas production are going to be enormous,” said Amy Myers Jaffe, the Wallace S. Wilson fellow for energy studies and one of the study’s authors. “By increasing alternative supplies to Europe in the form of liquefied natural gas (LNG) displaced from the U.S. market, the petro-power of Russia, Venezuela and Iran is faltering on the back of plentiful American natural gas supply.” In May, Chenier Energy announced it will invest $6 billion to convert its LNG import terminal in southwestern Louisiana to an export terminal. It expects LNG to begin flowing to foreign markets in 2015.

Though Boone Pickens saw lower gas prices blow away his plan to use wind to free up natural gas supplies to power heavy trucks, the shale revolution may lead to that end anyway. Compressed natural gas (CNG) is a good fuel for internal combustion engines, requiring little conversion of existing engines and producing considerably lower tailpipe emissions. But, as is the case with electric vehicles, a lack of fueling stations hampers CNG as a transportation fuel. Shale gas producer Chesapeake Energy Corp. hopes to solve that problem. The company recently announced it will invest $150 million in a project to build 150 CNG truck fueling stations along major U.S. truck routes.

It is also possible to convert methane into gasoline substitutes that can be used in existing pumps. The MIT gas reported noted, “Natural gas use in the transportation sector is likely to increase, with the primary benefit being reduced oil dependence. Compressed natural gas (CNG) will play a role, particularly for high-mileage fleets, but the advantages of liquid fuel in transportation suggest that the chemical conversion of gas into some form of liquid fuel may be the best pathway to significant market penetration.”

Little Downside with Shale Gas

The pending shale gas paradigm shift has prompted a counterrevolution, particularly among some environmentalists who see it as a threat to their ultimate goal of “carbon free” energy. Local opposition in areas where drilling is taking place—particularly in the eastern U.S., in the area of the Marcellus formation—helps drive opposition to shale gas development generally (Figure 4). Michael Krancer, secretary of Pennsylvania’s Department of Environmental Protection, recently complained that the debate over shale gas development is being “radicalized.” He said at a hearing in June, “Some folks just don’t want to debate at all how it can be done safely. They just want to kill it… they’re pulling out all the stops to make sure it doesn’t happen.” Pennsylvania supports shale gas recovery for obvious economic reasons: 140,000 well-paying jobs today and as many as 211,000 by 2020.

|

| 4. Drilling for dollars. A typical shale gas drilling site in Pennsylvania. Courtesy: Statoil, photo by Helge Hansen |

New Jersey, which lacks shale gas reserves, has banned fracking. Next door, on July 8, the New York Department of Environmental Conservation released a draft report with what appear to be very reasonable permit conditions for gas drilling in the Marcellus in that state; rules are due out later this year.

The U.S. Environmental Protection Agency (EPA) is examining the environmental impacts of shale gas development, and the U.S. Department of Energy is also studying the technology, even though the Energy Policy Act of 2005 exempted fracking from EPA regulations under the Safe Drinking Water Act, shifting the regulatory authority to individual states.

Opponents of shale gas development cite water pollution concerns resulting from the use of chemicals in the water used to pressurize the underground shale strata. Allegations include contamination of groundwater, including migration of methane into the water supply (although methane has never been identified as a threat to health). The independent documentary film Gasland included footage of flames shooting out of faucets, although industry officials have denounced these pictures as bogus parlor tricks.

However, during testimony before the U.S. House Oversight Committee in late May, EPA Administrator Lisa Jackson responded to questions about the safety of fracking by saying, “I’m not aware of any proven case where the fracking process itself has affected water.” A study by Duke University researchers released in May also found “no confirmed cases of an underground source of drinking water contaminated as a result of a hydraulic fracturing operation.”

The MIT gas study examined the environmental complaints, concluding that they present no novel issues. Rather, the problems related to shale gas development appear to be conventional and familiar to the oil and gas industry. MIT’s Meggs said that the small number of cases of contamination stem from poor practices in cementing well casings. “The quality of that cementing is the area where the industry, frankly, has to do a better job,” he said. But the study found only 42 documented instances of contamination from conventional gas well drilling. “It is not trivial,” said Meggs, “but neither is it all-encompassing.” Where there are problems, he noted, it’s possible to fix the well casings.

Shale critics have also argued that natural gas does not provide the climate benefits that MIT and others have cited. Cornell University ecologist Robert Howarth in April published an article making a surprising claim that methane leakage during drilling meant that shale gas was more damaging to the environment than coal. Methane is a much more potent greenhouse gas than CO2. Howarth acknowledged, “A lot of the data we used are really low quality,” which undercut his analysis.

Howarth’s work wasn’t persuasive even to some environmentalists. A Worldwatch Institute blog examined his analysis when it appeared, concluding that it has serious technical weaknesses. In May, Michael Levi, energy and environmental analyst for the Council on Foreign Relations, used National Energy Technology Laboratory data to debunk Howarth. Levi concluded, “Bottom line: Those who were skeptical of the Howarth study were reacting correctly.”

The New York Times recently published a series of articles by reporter Ian Urbina that were highly critical of the economics and environmental impacts of shale gas development. The work was based on a large, but highly selective, body of evidence including internal government emails and critiques from investment analysts (some of whom appear to be shorting the stocks of shale players, giving them an economic incentive to slam shale gas developers). The newspaper articles have produced a substantial backlash, including a rebuttal by the EIA suggesting that the newspaper misrepresented the agency’s projections for the role of shale gas. In a posting on its website, the EIA said its views on shale “differ in significant respects from those outlined” in the Times articles.

The series in the Times also prompted a tongue-lashing of the paper by Arthur Brisbane, its internal critic, or “public editor.” Specifically citing a June 26 article, Brisbane said, “My view is that such a pointed article needed more convincing substantiation, more space for a reasoned explanation of the other side and more clarity about its focus.” He added that “the article went out on a limb, lacked an in-depth dissenting view in the text and should have made clear that shale gas had boomed.”

More Gas Buried Deep

Are we seeing a shale boom that is destined to bust? Geologists point out that underlying the Marcellus Formation is an even bigger gas resource, the Utica shale. Notes veteran energy analyst Vinod Dar: “The Utica lies between 3,000 and 7,000 thousand feet beneath the Marcellus but extends further northwest and much further southwest. It underlies parts of New York, Pennsylvania, Maryland, Virginia, West Virginia, Ohio, Tennessee, Kentucky, Lake Erie, Lake Ontario, Ontario and Quebec. Its depth ranges from about 2 miles deep in parts of Pennsylvania to under 2,000 feet below sea level in parts of Ohio, the Great Lakes and Ontario. It is reportedly even shallower in Quebec.

“It is this very large footprint that is persuading E&P companies, especially Canadian companies, to postulate that the Utica shale may be a very large resource play even if recovery with current technology is only in the 2 to 3% range. Each generation of technology increases recovery rates and the industry is confident that recovery rates will keep rising over the next few decades.”

Europe’s Gas Boom

If the world is set to enter a golden age of gas, as the International Energy Agency (IEA) suggested recently, then the EU will certainly share in the excitement.

To supplement Western Europe’s own production of conventional gas, imports are readily available by pipeline from Russia and North Africa and, as LNG, from the Middle East. A frenzy of pipeline planning promises to bring in more gas from Russia and the Caspian region to the east, while the prospect of shale gas in Poland, France, and elsewhere holds great promise. With ambitious EU targets for CO2 emissions reductions forcing the retirement of old coal-fired power plants, and public opinion in Germany, Switzerland, and Italy now firmly anti-nuclear, the favorable economics and short construction times of gas-fired power plants have not looked so good since the UK’s dash for gas in the 1990s.

Though natural gas is plentiful, there is an argument that the favored fuel is disadvantaged because so much is imported. The EU, which already depends on Russia for 24% of its gas supply, lacks a clear energy policy and, according to some analysts, is not acting fast enough to ensure diversity of supplies. State-owned Russian gas giant Gazprom is investing aggressively in new pipelines to supply central Europe, while alternate gas supply routes bypassing Russia will not be available for years to come.

Gazprom even has ambitions in power production. RWE, the largest power producer in Germany, has been weakened by that country’s nuclear withdrawal and is not alone among European generators in feeling the squeeze from high Russian contract gas prices. In mid-July, RWE signed a memorandum of understanding with Gazprom to cooperate in building power plants in Germany, the UK, and Benelux (short for Belgium, the Netherlands, and Luxembourg). “The power industry is one of the priorities of Gazprom in Europe. In light of recent decisions by the German government to reduce their nuclear power programs, we see good prospects for the construction of new modern gas-fired power plants in Germany,” said Gazprom CEO Alexey Miller.

Exploiting shale gas would allow Europe to bypass Russia’s dominance, but despite the hype, only a few dozen wells have been drilled so far, and the extraction technology is not yet proven under European conditions. Environmental concerns may prove a serious obstacle: In May, the French government bowed to public protest and banned hydraulic fracturing (fracking).

Gas: A Quarter of Europe’s Energy

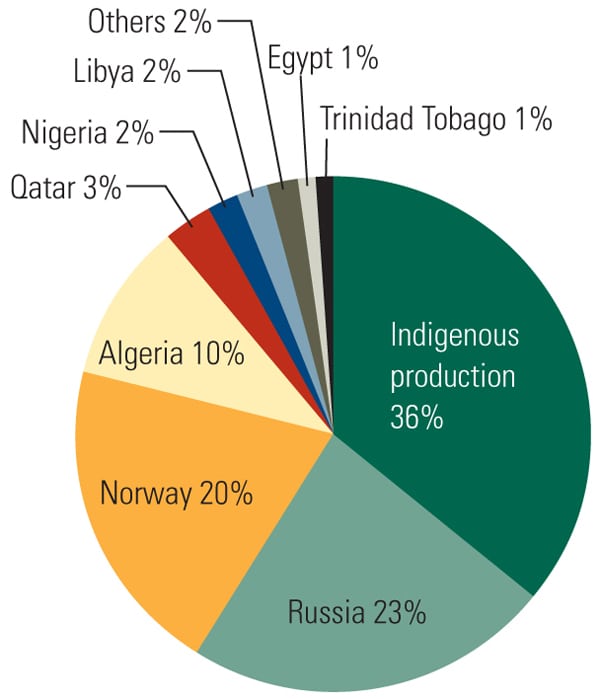

The EU nations consume around 17.3 Tcf (490 billion cubic meters) of gas a year (the U.S. uses 22.8 Tcf). This provides 24% of their primary energy, second only to oil (36% of primary energy), and 27% of all energy for power generation, according to Eurogas numbers for 2010. Natural gas production within the EU27 nations accounted for 36% of the gas used in 2009. Russia supplied an additional 23%, Norway 20% (see sidebar), and Algeria 10% (Figure 5).

|

| 5. Mostly imports. Natural gas production within the EU27 nations accounted for 36% of the gas used in 2009; the rest was imported. Russia supplied almost a quarter of the EU’s natural gas imports. Source: Eurogas |

As Table 1 shows, European countries vary widely in their reserves, production, and use of gas. Apart from Russia, only Ukraine, Norway, and the Netherlands have large conventional gas reserves, and the latter two nations are the only significant exporters now that Britain has become a net importer. In Western Europe, the two big economies of France and Germany are notable for their heavy dependence on imported gas.

|

| Table 1. European gas production, consumption, conventional reserves, and shale gas resources, excluding Russia. Source: U.S. EIA (market) and Oil and Gas Journal, Dec. 6, 2010 (proven reserves) |

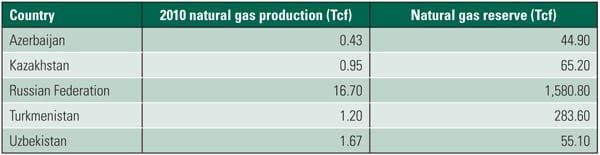

Russia is in a different league. Its reserves of some 1,600 Tcf are more than eight times those of the EU nations and Norway put together, but well under the latest EIA estimate of 2,552 Tcf of gas reserves in the U.S. At the moment, Russia also controls most exports from central Asia (Table 2), though new pipelines to the west could eventually bring the Caspian region more autonomy.

|

| Table 2. Russian and Eurasian gas production and reserves, 2010. U.S. natural gas reserves are estimated by the EIA as 2,552 Tcf. Source: BP Statistical Review of World Energy 2011 |

Russia exported 7.063 Tcf in 2010, of which 1.132 Tcf was imported from the Caspian region; the remainder was from domestic production. Of the 7.063 Tcf exported, 0.495 Tcf went out as LNG, mainly to Japan and Korea, and 2.436 Tcf went by pipeline to Belarus, Ukraine, and Turkey. The remaining 4.132 Tcf supplied the EU nations by pipeline, with Germany and Italy taking the most.

The European continent has three main pipeline routes: the Northern Corridor from Norway, the Eastern Corridor from Russia, and the Mediterranean Corridor from Africa. A Southern Corridor (South Stream) has been proposed to bring gas from the Caspian region.

Like power prices, gas prices vary widely across Europe. The UK has the lowest prices in Western Europe, currently around $10/MMBtu. German companies pay twice as much, and Danish users nearly three times as much. In most European countries, gas for industrial use currently costs around $14/MMBtu—two or three times as much as in the U.S. Russian industry, by comparison, pays less than $3/MMBtu.

The Nord Stream Controversy

The first of the big new pipelines, known as Nord Stream, will increase, not decrease, European dependence on Russian gas (Figure 6). Nord Stream runs from Vyborg in Russia, near the Finnish border, under the Baltic Sea to Greifswald in northeast Germany. At 759 miles (1,224 kilometers) it will be the world’s longest subsea pipeline and, when complete, its twin 48-inch-diameter pipes will be able to carry 1.942 Tcf of gas a year.

|

| 6. Building more pipelines. Several more pipelines that will bring more natural gas into Europe are either under construction or in planning stages. Shown are the projected routes of Nord Stream, Nabucco, and South Stream pipelines. Source: Nord Stream |

The laying and underwater work for the first line was completed on June 21, and start-up is scheduled for the last quarter of this year. The second line is now one-third complete and is scheduled to be operational by the last quarter of 2012 (Figure 7).

|

| 7. Finished pipeline. Welding of the last 12-meter-long pipe section in the first of Nord Stream’s two pipelines was completed on May 4, 2011. The twin 48-inch-diameter pipelines run from Vyborg, Russia, near the Finnish border, under the Baltic Sea to northeast Germany. Courtesy: Nord Stream |

Nord Stream is a joint project of Gazprom (51%), BASF SE/Wintershall (15.5%), E.ON Ruhrgas (15.5%), Gasunie (9%), and GDF Suez (9%). The chairman of Nord Stream AG is Gerhard Schröder, who promoted the project when he served as Germany’s chancellor, until 2005. The company says the subsea section will cost €7.4 billion; other sources quote €8.8 billion, plus €6 billion for the new onshore pipelines that will link Nord Stream with the existing Russian and German infrastructure.

This new pipeline will further tighten Russia’s economic stranglehold on the EU. Because the pipeline bypasses Ukraine and Belarus, Nord Stream will give Russia more political control over these countries without the risk of harming supplies to—and income from—Western Europe.

At the moment, Russian gas flows to Western Europe via pipelines through Ukraine and Belarus. Disputes with these two countries over gas costs and unpaid bills have several times prompted Russia to cut supplies, and occasionally Western Europe has suffered as a result. In June 2010, Russia restricted gas to Belarus. Much more serious for the EU were the rows with Ukrainian state gas company Naftohaz in January 2006 and January 2009, both of which disrupted supplies to much of the continent during the heating season.

Although Nord Stream is promoted as a pan-European project, critics say it will benefit mainly Russia and Germany. Slovak journalist Peter Ševce points out that countries such as Slovakia will experience a decrease in energy security because gas diverted through Nord Stream will no longer flow through their own transit pipelines. Poland and the Baltic states also objected vigorously to the project. U.S.-based energy analyst Mikhail Korchemkin, a long-time critic of Nord Stream, argues that many of Russia’s new pipeline projects are uneconomic and unnecessary.

More Pipelines to Come?

Russia’s next proposed pipeline is South Stream, which would cross the Black Sea to Bulgaria and from there split into two branches to supply central and southern Europe. The current partners are Gazprom, Italy’s Eni, Wintershall, and EDF. The distance of 584 miles (940 km) would be spanned by four parallel pipes with a combined capacity of 2.224 Tcf per year. The project could come on stream in 2015.

Marcel Kramer, CEO of South Stream AG, has argued that South Stream will mainly divert gas that currently flows through Ukraine, so it will do little to increase EU dependence on Russia. The implication is that South Stream is driven by economics.

The scheme’s many critics, on the other hand, see South Stream as simply a way to subvert Nabucco, the European Commission’s favored southern pipeline. They claim that Gazprom cannot say where the gas would come from and that the project would be uneconomic. For Gazprom to build, co-own, and operate the pipeline sections in EU territory would also require extensive exemptions from EU competition law.

Nabucco, in contrast, really would reduce dependence on Russia by allowing the Caspian region, Egypt, and the Middle East to export directly to Turkey and the EU. Nabucco would run for 2,512 miles from eastern Turkey to Austria, with a capacity of 1.094 Tcf per year. The current partners are OMV (Austria), MOL (Hungary), Transgaz (Romania), Bulgargaz (Bulgaria), BOTAS (Turkey), and RWE (Germany). It is scheduled for start-up in 2017.

Only Azerbaijan has so far signed a contract to supply gas to Nabucco; other potential suppliers are Iran, Iraq, Turkmenistan, and Egypt. Critics say that the project will be uneconomic without Iran’s participation, and that increasing availability of LNG threatens the viability of all long-distance pipelines.

Nabucco would likely be the first pipeline in the Southern Gas Corridor, a European Commission proposal to bring 2.118 to 4.238 Tcf of non-Russian gas to the EU. Other large pipelines proposed for the Southern Corridor are White Stream (from Georgia to Ukraine, Bulgaria, and central Europe), ITGI (Interconnector Turkey-Greece-Italy), and the Trans-Adriatic Pipeline (Greece, Albania, and Italy).

Shale Gas Hits the News

Given the cost and political complexity of trans-European pipelines, it’s no surprise that the discovery of unconventional gas reserves closer to home has generated excitement.

As Table 1 shows, according to EIA figures, Europe’s proven shale gas resources (639 Tcf) are comparable to those of the U.S. (827 Tcf) and, surprisingly, are more than three times the size of proven European conventional reserves. The EIA’s estimate of all proven natural gas resources (including shale gas) in the U.S. is 2,552 Tcf. The amount of proven conventional gas reserves in the U.S. (1,725 Tcf) is almost an order of magnitude larger than the EU’s reserves outside Russia (186 Tcf).

Most regions of the EU have some shale gas. Poland and France have very large resources, while Germany fares relatively badly. Sweden, Denmark, and Turkey, which have little or no conventional gas, do have respectable shale gas reserves.

A report published in May by the European Centre for Energy and Resource Security (EUCERS) at King’s College London estimates total recoverable reserves of unconventional gas in Europe at 1,165 to 1,342 Tcf: 530 Tcf of shale gas (slightly less than the EIA estimate shown in Table 1), 424 Tcf of tight gas (gas invery tight underground formations), and 283 Tcf of coal bed methane gas. This compares with total EU conventional gas reserves of 85.5 Tcf, the report says (although the EIA figures are double that), and unconventional gas could meet Europe’s gas demand for another 60 years.

The relatively high price of European gas—currently around $9/MMBtu for long-term contracts—will help to make shale gas extraction economic, the EUCERS study authors believe. In particular, shale gas could undercut expensive gas from new Russian sources such as the Yamal Peninsula in Siberia and the Shtokman field in the Barents Sea. Even the threat of low-cost shale gas could force Gazprom to increase its commercial flexibility.

A report by Florence Gény of the UK’s Oxford Institute for Energy Studies (OIES) is more cautious, putting the break-even cost of European shale gas at $8 to $16/MMBtu. Drilling costs will be two or three times as much as in the U.S., Gény says, in part because the gas-bearing shales are deeper.

Although Europe should be able to benefit from a decade of U.S. experience with the technology of shale gas extraction, some other European peculiarities will hinder the transfer of know-how, the study points out. In many European countries, for instance, reliable geological information is hard to come by. There are also big differences in market structures and legal frameworks. In Europe, for instance, gas is much more likely to belong to the state than to the landowner. Europe’s high population density will also be an issue, the OIES study says, though other shale gas commentators disagree.

A “land grab” since 2007 has seen applications and licenses for unconventional gas covering well over 40,000 square miles (100,000 square kilometers), mostly in Poland, France, and Germany. By the end of 2010 around 50 companies were involved, from the oil majors (ExxonMobil, Shell, Total, ConocoPhillips, and Chevron) down to small independents. So far, they have drilled only a handful of wells, and significant production is unlikely until at least 2020.

In France, public protests about the environmental consequences of shale gas extraction have led the government to ban fracking, despite having already issued licenses for that country’s seemingly rich shale gas resources (Figure 8). The citizens of France are becoming increasingly environmentally conscious, and there is even a strong movement to abolish the nuclear reactors that provide most of France’s electricity.

|

| 8. Bad press. Public protests have forced the French government to ban shale gas fracking, at least for now. Courtesy: Nicolas Sawicki |

Coal bed methane (CBM) is a largely undeveloped resource in Europe, but it seems likely to expand on the back of the shale gas revolution. Australian CBM specialist Dart Energy, for instance, entered the European market in February with the acquisition of Scottish company Composite Energy. Dart has 15 CBM licenses in the UK and has just signed a CBM sales contract in Scotland to begin in 2013. Dart also recently partnered with Belgian company NV Mijnen, which owns all the coal fields in the Flanders region of Belgium.

— Kennedy Maize is a POWER contributing editor and executive editor of MANAGING POWER. Charles Butcher ([email protected]) is a UK freelance writer specializing in the energy and chemical industries. Dr. Robert Peltier, PE is POWER’s editor-in-chief.